+1 credit

+1 credit

| Version | Summary | Created by | Modification | Content Size | Created at | Operation |

|---|---|---|---|---|---|---|

| 1 | Thaís Vieira Nunhes | + 2651 word(s) | 2651 | 2021-02-02 05:16:33 | | | |

| 2 | Bruce Ren | -303 word(s) | 2348 | 2021-02-10 03:56:27 | | |

Video Upload Options

This entry aims to identify and analyse the Scientific Technical Scenary on Corporate Sustainability (STS-CS) and propose a three-way Helix-based structure for its development and guidance on future scientific and technological investments. The study was developed using a combined method of bibliometric analysis and analysis of the content of scientific articles and technical publications (patents, white papers, publications of public bodies, etc.). The scientific articles were researched in the Scopus database and technical publications on the Orbit Intelligence, ProQuest and UN Global Compact platforms. The STS-CS was analysed in the light of scientific and technical literature and the experience of the authors of the study.

1. Background

Population and economic growth has resulted in increasing damage to the planet's sustainability. With the increasing need for consumption, the planet began to show signs that it could not support unbridled human development. From this point on, alternatives to sustainable development (DS) have begun to be discussed [1][2]. The idea of sustainable development was first presented in the World Commission's open letter on Environment and Development (p. 43), which defines SD as "development that meets present needs without compromising the ability of future generations to meet their own needs". Sustainability initially meant never picking more than the forest needs to generate a new harvest in the future [3]. The concept of SD has evolved and now has different meanings, but most have the same essence of the initial concept, that is, society should not use natural resources at a rate higher than its regeneration [4]. This is how the long-term need for human welfare began to be understood [5].

Initially, the study of sustainability was restricted to areas such as geography and sociology [6]. However, it did not take long for sustainability research to spread out and be applied in different areas, such as public and private government management [7]. In this sense, Currie et al. (2010) argue that increased interest in the study of business sustainability may have been the result of the various social, environmental and economic crises faced in the current world [6]. Companies ar e being charged for having negative impacts on the DS, as the "price" of the extraction, use and disposal of natural resources is quite significant, and its effects, such as increased air pollution, reduction of biodiversity and intensification of the impact of global warming, not only nature, but also the survival of society [8]. Today, the global community is consuming the production of more than 1,7 planets a year. Earth Overshoot Day is the date when humanity's demand for green resources and services each year exceeds what the Earth can regenerate. In 2020, Overshoot Day was in August 22 [9]. All consumption after that date was taken from resources that should be saved for future generations. Thus, following the scientific vanguard, pressures from various groups, including environmentalists, government and society, have become recurring for companies to make changes to mitigate the negative impacts of their activities on the sustainability of the planet [10]. In 2020, Overshoot Day was in August 22 [9]. All consumption after that date was taken from resources that should be saved for future generations. Thus, following the scientific vanguard, pressures from various groups, including environmentalists, government and society, have become recurring for companies to make changes to mitigate the negative impacts of their activities on the sustainability of the planet [8,10]. In 2020, Overshoot Day was in August 22 [9]. All consumption after that date was taken from resources that should be saved for future generations. Thus, following the scientific vanguard, pressures from various groups, including environmentalists, government and society, have become recurring for companies to make changes to mitigate the negative impacts of their activities on the sustainability of the planet [10].

2. Sustainable development of the company

As a result of these pressures, the concept of sustainable development was applied to the reality of companies, being known as corporate sustainability (SC) [11]. According to Lo and Sheu (2007), corporate sustainability is a business strategy in which value is added to the product through risk management in the economic, environmental (or ecological) and social dimensions [12]. Improving the performance of companies in all three dimensions can be based on the Triple Bottom Line (TBL) [13]. Corporate Social Responsibility (RSC) is often used as synonymous with RS, which can be seen as working with DS at company level. In this article, we use CS to describe the sustainability of the company covering all its meanings. CS gradually ceased to be a mere response to the pressure of interested parties to become a powerful market differentiator [14]. The sustainable company title has become increasingly coveted by organizations for a number of reasons: for example, the influence that sustainable management can have on the definition of value-added products and the valuation of company value on financial markets [14][15]. In addition, changing the company's view of itself by adopting "green" and innovative practices can result in new products and processes that are more economical, social and environmental efficient [16].

According to the United Nations Global Compact (UNGC 2018), the market has also increased its interest in more sustainable companies, as exemplified by the increase in 22% in the US Sustainable and Responsible Investment Market (ISR) since 2009. In addition, more than 8.000 companies participated in the Global Compact, the world's largest corporate sustainability initiative [17]. Another study published in 2013 by KPMG, the consultancy firm providing audit and advisory services, showed that approximately 233 of the 250 most valuable companies in the world are committed to sustainability [18]. Consistent with this trend, sustainability reports are becoming increasingly, on a global level, an essential part of CS [19][20]. Companies plan, execute and report their data on sustainability using sustainability reporting guidelines. Among them, the guidelines of the Global Reporting Initiative (GRI) standards are the most used for reporting sustainability around the world [21]. They are openly accessible to stakeholders and stimulate competitiveness as organizations are oriented to respond to the relevant benchmarks of their competitors [22].

Corporate sustainability indices such as the MSCI ESG (global environmental, social and governance index of Morgan Stanley Capital International), DJSI (global sustainability index Dow Jones) and ISE B3 (corporate sustainability index of Latin America B3) are other important tools for CS. These are CS assessment tools that, as well as CS reporting tools, provide users with guidance structures that support the implementation of CS. Corporate sustainability indices facilitate the understanding and evaluation of company performance over time by means of multidimensional and comprehensive indicators in the areas of environment, social and governance (ESG) [23]. The most widely used sustainability index is the Dow Jones Sustainability. It consists of a set of criteria assessed by the Sustainable Asset Management Group (SAM).

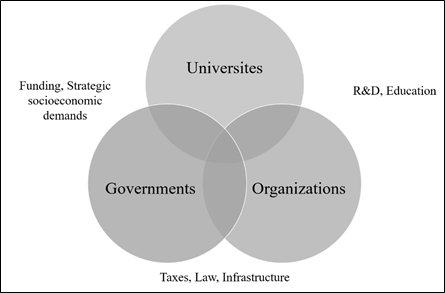

As can be seen, several fields of study are aligned with the aim of developing sustainable management. Topics related to the economic, social and environmental facets of SC can be studied and applied in integrated [24], separated [25], and along with other tools and disciplines [26]. For example, some to promote SC are ecological footprint, life cycle assessment (LCA), standards such as ISO 14.000 family on environmental management and ISO 26.000 on social responsibility, cleaner production techniques to eliminate or minimize waste and emissions at source, eco-design, natural capitalism and the Structure of natural capitalism. Planetary Borders, among others [27][28]. According to Ferreira et al. (2016), when an area reaches significant advances, it is important to map its historical evolution, identifying its structure, strengths, and weaknesses [29]. It is therefore up to investigate the main initiatives, practices and studies in the field of the SC that have allowed its development in the last twenty years and which can serve as a basis for universities, governments and organizations in implementing their strategies. In this context, government policies and legislation that foster the adoption of practices, research and innovations developed by researchers from the scientific academy in the area and the alignment of business models of companies with the pillars of sustainability have been responsible for the development of the SC around the world. The structure of Triple Helix (TH) presented in Figure 1 suggests the interconnection between these sectors to drive sustainable business development [30]. It is to investigate the main initiatives, practices and studies in the field of SC that have enabled it to develop over the last twenty years and which can serve as a basis for universities, governments and organisations in implementing their strategies. In this context, government policies and legislation that foster the adoption of practices, research and innovations developed by researchers from the scientific academy in the area and the alignment of business models of companies with the pillars of sustainability have been responsible for the development of the SC around the world. The structure of Triple Helix (TH) presented in Figure 1 suggests the interconnection between these sectors to drive sustainable business development [30]. It is to investigate the main initiatives, practices and studies in the field of SC that have enabled it to develop over the last twenty years and which can serve as a basis for universities, governments and organisations in implementing their strategies. In this context, government policies and legislation that foster the adoption of practices, research and innovations developed by researchers from the scientific academy in the area and the alignment of business models of companies with the pillars of sustainability have been responsible for the development of the SC around the world. The structure of Triple Helix (TH) presented in Figure 1 suggests the interconnection between these sectors to drive sustainable business development [30]. It is to investigate the main initiatives, practices and studies in the field of SC that have enabled it to develop over the last twenty years and which can serve as a basis for universities, governments and organisations in implementing their strategies. In this context, government policies and legislation that foster the adoption of practices, research and innovations developed by researchers from the scientific academy in the area and the alignment of business models of companies with the pillars of sustainability have been responsible for the development of the SC around the world. The structure of Triple Helix (TH) presented in Figure 1 suggests the interconnection between these sectors to drive sustainable business development [30]. and studies in computer science that have allowed its development in the last twenty years and that can serve as a basis for universities, governments and organizations in implementing their strategies. In this context, government policies and legislation that foster the adoption of practices, research and innovations developed by researchers from the scientific academy in the area and the alignment of business models of companies with the pillars of sustainability have been responsible for the development of the SC around the world. The structure of Triple Helix (TH) presented in Figure 1 suggests the interconnection between these sectors to drive sustainable business development [30]. and studies in computer science that have allowed its development in the last twenty years and that can serve as a basis for universities, governments and organizations in implementing their strategies. In this context, government policies and legislation that foster the adoption of practices, research and innovations developed by researchers from the scientific academy in the area and the alignment of business models of companies with the pillars of sustainability have been responsible for the development of the SC around the world. The structure of Triple Helix (TH) presented in Figure 1 suggests the interconnection between these sectors to drive sustainable business development [30]. Government policies and legislation that foster the adoption of science and technology practices, researches and innovations developed by researchers from the scientific academy of the area and the alignment of business models with the pillars of sustainability have been responsible for the development of science and technology worldwide. The structure of Triple Helix (TH) presented in Figure 1 suggests the interconnection between these sectors to drive sustainable business development [30]. Government policies and legislation that foster the adoption of science and technology practices, researches and innovations developed by researchers from the scientific academy of the area and the alignment of business models with the pillars of sustainability have been responsible for the development of science and technology worldwide. The structure of Triple Helix (TH) presented in Figure 1 suggests the interconnection between these sectors to drive sustainable business development [30].

Figure 1. Triple Helix model showing relationships between universities, governments and organizations. Source: Adapted from Kimatu (2016) and Ranga and Etzkowitz (2013).

Since the recognition of the importance of the theme at the end of the 1990, the number of academic, governmental and business initiatives in SC has increased continuously (see Figure 1 in Section 3.1). To illustrate this growth during the period covered by this study (1999-2018), one can highlight academic initiatives that have resulted in more than one.500 scientific articles published in the Scopus database up to 2019 on CS, indicating that this is a hot topic of major relevance to the scientific community; the commitment of organizations with more than one.500 patents in the development of sustainable technologies launched; and the efforts of governments and non-governmental organizations (NGOs) to use more than 500 documents (reports, cases and white papers) published on the ProQuest and Global Compact platforms.

In addition, according to a Scopus database search, only in the last five years, several SC reviews have been published. Among the most influential, Alshehhi et al. (2018) reviewed literature on the impact of SC on the financial performance of organizations, with the aim of discussing the main issues that hinder consensus on this relationship [31]. Batista and Francisco (2018) proposed to identify sustainable practices carried out by large corporations in a plan to implement organizational sustainability [32]. Kourula et al. (2017) focused on studies of computer science in the areas of business and international administration, discussing the potential of interdisciplinary work in this topic [33]. Desore and Narula (2017) described their CS research in the textile industry, analyze the good practices and barriers of this sector in the implementation of sustainability [34]. Naidoo and Gasparatos (2018) have developed corporate environmental sustainability strategies that can be inserted in the context of retail [35]. Although these revisions have contributed to the art state of CS, this review especially adds to the body of knowledge contributions from companies and governments, including analysis of sustainability reports and patent publications; materials prepared by governments, primarily the enactment of laws; and content universities and development funds, among other materials which, together with the experience of the authors, formed the basis for the proposed structure.

References

- Whiteman, G.; Walker, B.; Perego, P. Planetary Boundaries: Ecological Foundations for Corporate Sustainability. J. Manag. Stud. 2013, 50, 307–336.

- Keeble, B.R. The Brundtland Report: “Our Common Future.” Med. War 1988, 4, 17–25.

- Kuhlman, T.; Farrington, J. What is sustainability? Sustainability 2010, 2, 3436–3448.

- Aras, G.; Crowther, D. Governance and sustainability: An investigation into the relationship between corporate governance and corporate sustainability. Manag. Decis. 2008, 46, 433–448.

- Hahn, T.; Figge, F. Beyond the Bounded Instrumentality in Current Corporate Sustainability Research: Toward an Inclusive Notion of Profitability. J. Bus. Ethics 2011, 104, 325–345.

- Currie, G.; Knights, D.; Starkey, K. Introduction: A post-crisis critical reflection on business schools. Br. J. Manag. 2010, 21, s1–s5.

- Cullen, J.G. Educating Business Students About Sustainability: A Bibliometric Review of Current Trends and Research Needs. J. Bus. Ethics 2017, 145, 429–439.

- Baumgartner, R.J.; Ebner, D. Corporate sustainability strategies: Sustainability profiles and maturity levels. Sustain. Dev. 2010, 18, 76–89.

- Earth Overshoot Day. Available online: https://www.overshootday.org/ (accessed on 18 December 2020).

- Milne, M.J.; Gray, R. W(h)ither Ecology? The Triple Bottom Line, the Global Reporting Initiative, and Corporate Sustainability Reporting. J. Bus. Ethics 2013, 118, 13–29.

- Roca, L.C.; Searcy, C. An analysis of indicators disclosed in corporate sustainability reports. J. Clean. Prod. 2012, 20, 103–118.

- Lo, S.F.; Sheu, H.J. Is corporate sustainability a value-increasing strategy for business? Corp. Gov. An Int. Rev. 2007, 15, 345–358.

- Elkington, J. Accounting for the Triple Bottom Line". Meas. Bus. Excell. 1997, 2, 18–22.

- Lee, D.D.; Faff, R.W. Corporate sustainability performance and idiosyncratic risk: A global perspective. Financ. Rev. 2009, 44, 213–237.

- Artiach, T.; Lee, D.; Nelson, D.; Walker, J. The determinants of corporate sustainability performance. Account. Financ. 2010, 50, 31–51.

- Bos-brouwers, H.E.J. Corporate sustainability and innovation in SMEs: Evidence of themes and activities in practice. Bus. Strateg. Environ. 2009, 19, 417–435.

- UN Global Compact United Nations Global Compact Progress Report 2018; United Nations: New York, NY, USA 2018.

- Diouf, D.; Boiral, O. The quality of sustainability reports and impression management. Accounting, Audit. Account. J. 2017, 30, 643–667.

- Lozano, R.; Huisingh, D. Inter-linking issues and dimensions in sustainability reporting. J. Clean. Prod. 2011, 19, 99–107.

- Lee, K.H.; Farzipoor Saen, R.; Farzipoor, R. Measuring corporate sustainability management: A data envelopment analysis approach. Int. J. Prod. Econ. 2012, 140, 219–226.

- Talbot, D.; Boiral, O. GHG reporting and impression management: An assessment of sustainability reports from the energy sector. J. Bus. Ethics 2018, 147, 367–383.

- Nicolăescu, E.; Alpopi, C.; Zaharia, C. Measuring corporate sustainability performance. Sustainability 2015, 7, 851–865.

- Feil, A.A.; de Quevedo, D.M.; Schreiber, D. An analysis of the sustainability index of micro- and small-sized furniture industries. Clean Technol. Environ. Policy 2017, 19, 1883–1896.

- Schaltegger, S.; Lüdeke-Freund, F.; Hansen, E.G. Business cases for sustainability: The role of business model innovation for corporate sustainability. Int. J. Innov. Sustain. Dev. 2012, 6, 95–119.

- Goyal, P.; Rahman, Z.; Kazmi, A.A. Corporate sustainability performance and firm performance research: Literature review and future research agenda. Manag. Decis. 2013, 51, 361–379.

- Formentini, M.; Taticchi, P. Corporate sustainability approaches and governance mechanisms in sustainable supply chain management. J. Clean. Prod. 2016, 112, 1920–1933.

- Broman, G.I.; Robèrt, K.H. A framework for strategic sustainable development. J. Clean. Prod. 2017, 140, 17–31.

- Nawaz, W.; Koç, M. Development of a systematic framework for sustainability management of organizations. J. Clean. Prod. 2018, 171, 1255–1274.

- Ferreira, J.J.M.; Fernandes, C.I.; Ratten, V. A co-citation bibliometric analysis of strategic management research. Scientometrics 2016, 109, 1–32.

- Kimatu, J.N. Evolution of strategic interactions from the triple to quad helix innovation models for sustainable development in the era of globalization. J. Innov. Entrep. 2016, 5, 1–7.

- Alshehhi, A.; Nobanee, H.; Khare, N. The impact of sustainability practices on corporate financial performance: Literature trends and future research potential. Sustainability 2018, 10, 494.

- Batista, A.A.S.; de Francisco, A.C. Organizational sustainability practices: A study of the firms listed by the Corporate Sus-tainability Index. Sustainability 2018, 10, 226.

- Kourula, A.; Pisani, N.; Kolk, A. Corporate sustainability and inclusive development: Highlights from international business and management research. Curr. Opin. Environ. Sustain. 2017, 24, 14–18.

- Desore, A.; Narula, S.A. An overview on corporate response towards sustainability issues in textile industry. Environ. Dev. Sustain. 2018, 20, 1439–1459.

- Naidoo, M.; Gasparatos, A. Corporate environmental sustainability in the retail sector: Drivers, strategies and performance measurement. J. Clean. Prod. 2018, 203, 125–142.