+1 credit

+1 credit

| Version | Summary | Created by | Modification | Content Size | Created at | Operation |

|---|---|---|---|---|---|---|

| 1 | Rashmeet Kaur | -- | 2267 | 2024-01-02 12:11:58 | | | |

| 2 | Lindsay Dong | Meta information modification | 2267 | 2024-01-03 02:09:04 | | |

Video Upload Options

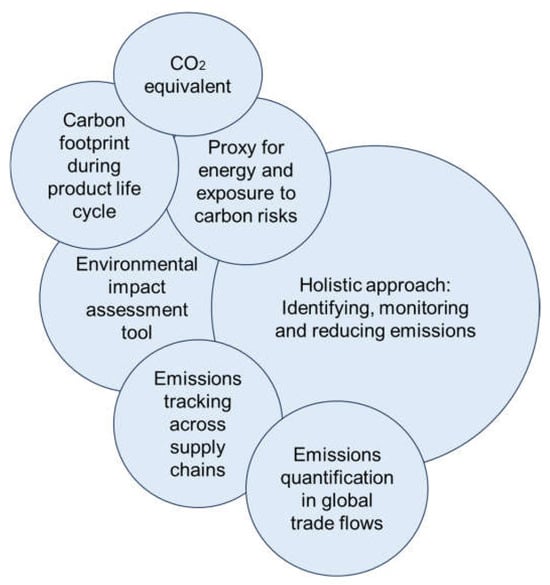

Carbon accounting is primarily a process for measuring, reporting, and allocating greenhouse gas emissions from human activities, thus enabling informed decision-making to mitigate climate change and foster responsible resource management. There is a noticeable upsurge in the academia regarding carbon accounting, which engenders complexity due to the heterogeneity of practices that fall under the purview of carbon accounting. Such plurality has given rise to a situation where diverse interpretations of carbon accounting coexist, often bereft of uniformity in definition and application. Consequently, organisations need a standardised, comprehensive, and sequentially delineated carbon accounting framework amenable to seamless integration into end-to-end manufacturing systems.

1. Introduction

2. Carbon Accounting in Manufacturing Systems and Supply Chains

2.1. The Current Understanding of the Definition of Carbon Accounting in Manufacturing Systems and Supply Chains

The Current Gaps Identified in Carbon Accounting in the Manufacturing Systems and Supply Chain Systems Literature

The Future Research Agenda for Carbon Accounting in Manufacturing Systems and Supply Chains

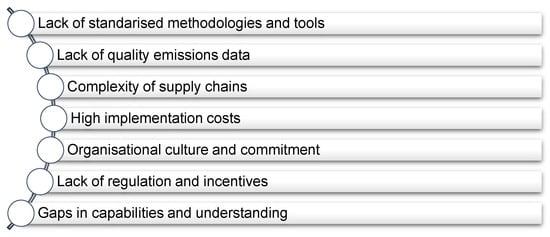

The Challenges of Carbon Accounting Implementation in Manufacturing Systems and Supply Chains

References

- Schaltegger, S.; Csutora, M. Carbon accounting for sustainability and management. Status quo and challenges. J. Clean. Prod. 2012, 36, 1–16.

- Marlowe, J.; Clarke, A.; Marlowe, J.; Clarke, A. Carbon Accounting: A Systematic Literature Review and Directions for Future Research. Green Financ. 2022, 1, 71–87.

- Cohen, Y.; Faccio, M.; Galizia, F.G.; Mora, C.; Pilati, F. Assembly system configuration through Industry 4.0 principles: The expected change in the actual paradigms. IFAC-PapersOnLine 2017, 50, 14958–14963.

- Bistline, J.E. Roadmaps to net-zero emissions systems: Emerging insights and modelling challenges. Joule 2021, 5, 2551–2563.

- Anderson, K.; Broderick, J.; Stoddard, I. A factor of two: How the mitigation plans of ‘climate progressive’ nations fall far short of Paris-compliant pathways. Clim. Policy 2020, 20, 1290–1304.

- Knox-Hayes, J.; Brown, M.A.; Sovacool, B.K.; Wang, Y. Understanding attitudes toward energy security: Results of a cross-national survey. Glob. Environ. Chang. 2013, 23, 609–622.

- Carnegie, G.D.; Parker, L.D.; Tsahuridu, E.E. It’s 2020: What is Accounting Today? Aust. Account. Rev. 2020, 31, 65–73.

- Maynard, J. Financial Accounting, Reporting, and Analysis; Oxford University Press: Oxford, UK, 2017; pp. 74–90.

- Carbon Might Be Your Company’s Biggest Financial Liability. Available online: https://hbr.org/2021/10/carbon-might-be-your-companys-biggest-financial-liability (accessed on 4 October 2023).

- Lodhia, S.; Hess, N. Sustainability accounting and reporting in the mining industry: Current literature and directions for future research. J. Clean. Prod. 2014, 84, 43–50.

- Stechemesser, K.; Guenther, E. Carbon accounting: A systematic literature review. J. Clean. Prod. 2012, 36, 17–38.

- Lovell, H.; MacKenzie, D. Accounting for carbon: The role of accounting professional organisations in governing climate change. Antipode 2011, 43, 704–730.

- Zhanga, C.; Zhang, C.; Zhou, M. Rethinking on the definition of carbon accounting. In Proceedings of the International Conference on Modern Economic Development and Environment Protection ICMED, Chengdu, China, 28–29 May 2016.

- DeFond, M.; Zhang, J. A review of archival auditing research. J. Account. Econ. 2014, 58, 275–326.

- Esfahbodi, A.; Zhang, Y.; Watson, G. Sustainable supply chain management in emerging economies: Trade-offs between environmental and cost performance. Int. J. Prod. Econ. 2016, 181, 350–366.

- Hertwich, E.G.; Wood, R. The growing importance of scope 3 greenhouse gas emissions from industry. Environ. Res. Lett. 2018, 13, 104013.

- Downie, J.; Stubbs, W. Evaluation of Australian companies’ scope 3 greenhouse gas emissions assessments. J. Clean. Prod. 2013, 56, 156–163.

- Kaur, R.; Patsavellas, J.; Haddad, Y.; Salonitis, K. Carbon accounting management in complex manufacturing supply chains: A structured framework approach. Procedia CIRP 2022, 107, 869–875.

- Roman-White, S.; Littlefield, J.; Fleury, K.G.; Allen, D.T.; Balcombe, P.; Konschnik, K.E.; Ewing, J.J.; Ross, G.B.; George, F. LNG Supply Chains: A Supplier-Specific Life-Cycle Assessment for Improved Emission Accounting. ACS Sustain. Chem. Eng. 2021, 9, 10857–10867.

- Liu, Z.; Zhang, W.M.; Xiao, Z.; Sun, J.; Li, D. Research on Extended Carbon Emissions Accounting Method and its application in Sustainable Manufacturing. Procedia Manuf. 2020, 43, 175–182.

- Lee, K.-H. Carbon accounting for supply chain management in the automobile industry. J. Clean. Prod. 2012, 36, 83–93.

- De Vries, G.J.; Ferrarini, B. What Accounts for the Growth of Carbon Dioxide Emissions in Advanced and Emerging Economies? The Role of Consumption, Technology and Global Supply Chain Participation. Ecol. Econ. 2017, 132, 213–223.

- Tang, S.; Xu, Y. An Empirical Study on Environmental Accounting Information Disclosure of Manufacturing Enterprises in China. In Proceedings of the 2nd International Conference on Contemporary Education, Social Sciences and Humanities, Beijing, China, 9–11 June 2017.

- Jamil, C.Z.M.; Mohamed, R.; Muhammad, F.; Ali, A. Environmental Management accounting practices in small medium manufacturing firms. Procedia—Soc. Behav. Sci. 2015, 172, 619–626.

- Mohamed, R.; Jamil, C.Z.M. The influence of environmental management accounting practices on environ-mental performance in small-medium manufacturing in Malaysia. Int. J. Environ. Sustain. Dev. 2020, 19, 378.

- Nguyen, T.H. Factors affecting the implementation of environmental management accounting: A case study of pulp and paper manufacturing enterprises in Vietnam. Cogent Bus. Manag. 2022, 9, 2141089.

- Elhossade, S.S.; Abdo, H.; Mas’ud, A. Impact of institutional and contingent factors on adopting environmental management accounting systems: The case of manufacturing companies in Libya. J. Financ. Report. Account. 2020, 19, 497–539.

- Mukwarami, S.; Nkwaira, C.; Van Der Poll, H.M. Environmental management accounting implementation challenges and supply chain management in emerging economies’ manufacturing sector. Sustainability 2023, 15, 1061.

- Burritt, R.; Schaltegger, S. Accounting towards sustainability in production and supply chains. Br. Account. Rev. 2014, 46, 327–343.

- Tiwari, K.; Khan, M.S.; Bharti, P.K. Sustainability Accounting and Reporting for supply chains in India-State-of-the-Art and Research challenges. IOP Conf. Ser. Mater. Sci. Eng. 2018, 404, 012022.

- Booth, M.S. Not carbon neutral: Assessing the net emissions impact of residues burned for bioenergy. Environ. Res. Let. 2018, 13, 035001.

- Cowie, A.L.; Berndes, G.; Bentsen, N.S.; Brandão, M. Applying a science-based systems perspective to dispel misconceptions about climate effects of forest bioenergy. GCB Bioenergy 2021, 13, 1210–1231.

- Balcombe, P.; Staffell, I.; Kerdan, I.G.; Speirs, J.F.; Brandon, N.P.; Hawkes, A.D. How can LNG-fuelled ships meet decarbonisation targets? An environmental and economic analysis. Energy 2021, 227, 120462.

- Friedlingstein, P.; O’sullivan, M.; Jones, M.W.; Andrew, R.M.; Hauck, J.; Olsen, A. Global carbon budget 2020. Earth Sys. Sci. Data Dis. 2020, 12, 3269–3340.

- Tanç, A.; Gökoğlan, K. The Impact of Environmental Accounting on Strategic Management Accounting: A Research on Manufacturing companies. Int. J. Econ. Financ. Issues 2015, 5, 566–573.

- Tian, X.; Sarkis, J. Towards greener trade and global supply chain environmental accounting. An embodied environmental resources blockchain design. Int. J. Prod. Res. 2023, 1–20.

- Aragão, G.M.; Saralegui-Díez, P.; Villasante, S.; López-López, L.; Aguilera, E.; Moranta, J. The carbon footprint of the hake supply chain in Spain: Accounting for fisheries, international transportation and domestic distribution. J. Clean. Prod. 2022, 360, 131979.

- Donaghy, T.Q.; Stockman, L. Comment on “LNG Supply Chains: A Supplier-Specific Life-Cycle Assessment for Improved Emission Accounting”. ACS Sustain. Chem. Eng. 2022, 10, 13549–13551.

- Hoai, T.T.; Minh, N.N.; Van, H.V.; Nguyen, N.P. Accounting going green: The move toward environmental sustainability in Vietnamese manufacturing firms. Corp. Soc. Responsib. Environ. Manag. 2023, 30, 1928–1941.