Carbon accounting is primarily a process for measuring, reporting, and allocating greenhouse gas emissions from human activities, thus enabling informed decision-making to mitigate climate change and foster responsible resource management. There is a noticeable upsurge in the academia regarding carbon accounting, which engenders complexity due to the heterogeneity of practices that fall under the purview of carbon accounting. Such plurality has given rise to a situation where diverse interpretations of carbon accounting coexist, often bereft of uniformity in definition and application. Consequently, organisations need a standardised, comprehensive, and sequentially delineated carbon accounting framework amenable to seamless integration into end-to-end manufacturing systems.

1. Introduction

The evolving interplay between corporate responsibility and environmental sustainability imperatives has propelled carbon accounting into sustainability discussions. As societies grapple with the profound effects of climate change, there is an elevated importance in comprehensively understanding and transparently measuring carbon emissions

[1]. Manufacturing systems are central to these discussions of climate change and carbon emissions, which play a crucial role in the global economy. Such systems warrant a meticulous examination, especially concerning their greenhouse gas (GHG) emissions

[2]. Manufacturing systems are complex conglomerations comprising products, machinery, personnel, information, control mechanisms, and support functions. All these elements are to be integrated to facilitate physical goods’ inception, production, distribution, and overall life cycle management. This intricate process caters to both market demands and societal needs

[3]. A paramount goal within these manufacturing systems is the ambition of net-zero emissions. This entails striving towards a state where the GHG emissions produced by these systems are considerably reduced, looming at a near-zero level

[4]. Diminishing emissions is pivotal for decelerating the progression of climate change and alleviating its consequent ramifications

[5]. Regulatory adherence plays a significant role in this context; in a multitude of nations, legal frameworks mandate organisations to transparently disclose their GHG emissions

[6].

Accounting is the systematic practice of recording and analysing financial data about businesses. This includes documenting financial transactions and producing financial statements that convey an organisation’s economic activities and health

[7]. Financial accounting focuses on creating detailed financial reports for stakeholders, ensuring clarity and transparency in financial communication

[8]. On another note, carbon accounting measures entities’ carbon dioxide equivalent emissions, including their supply chains, where there are inherent challenges in data collection, given it is outside the direct control of the organisation. This form of accounting covers a wide range of activities, such as measuring and reporting GHG emissions at various levels

[9]. Both financial and carbon accounting are tools for organisations to monitor and report on essential operational facets. Carbon accounting is an instrumental process, facilitating organisations to comply with these statutory requirements, thereby circumventing potential financial penalties

[10].

The definition of carbon accounting has evolved over the years

[11]. This happened due to several factors, including changing societal and environmental concerns, advances in the scientific understanding of climate change and GHG emissions, and developments in industry and policy

[11][12]. As society has become more aware of the impacts of climate change, there has been an increasing demand for accurate and transparent reporting of GHG emissions. This has led to the development of new tools, standards, and guidelines to help organisations report and manage their emissions

[13][14][15]. In addition, advances in the scientific understanding of climate change and GHG emissions have led to changes in how carbon accounting is conducted. For example, there is now greater recognition of the importance of measuring and reporting emissions from the entire supply chain, not just direct emissions from a single organisation

[16][17]. Overall, the evolving definition of carbon accounting reflects the changing environmental, social, and economic context in which organisations operate and the need for accurate and transparent reporting of GHG emissions.

2. Carbon Accounting in Manufacturing Systems and Supply Chains

Carbon accounting has gained increasing attention as a means for companies to measure, manage, and reduce their GHG emissions and overall carbon footprint. This is especially relevant to emissions-intensive sectors like manufacturing, where carbon accounting can support emission reductions across production processes and broader supply chains

[18][19][20][21][22].

Several studies have explored carbon accounting approaches tailored to the manufacturing sector. For the aerospace industry, a structured framework was proposed to facilitate consistent carbon measurement and reporting across complex extended supply chains

[18]. This framework emphasised the need for complete supply chain visibility and senior leadership support. In the automotive industry, the researchers in

[21] found that an environmental management accounting and eco-control approach helped Korean manufacturers align carbon management strategies with performance measurement. The study highlighted the need for quantitative carbon data to support decision-making. At a product level, researchers

[19] developed a framework to compile supplier-specific life cycle GHG emissions data for liquified natural gas, from extraction through to distribution. The granular, supplier-specific data were intended to differentiate the emissions profiles of various supply chains amid growing policy interest in embedded carbon emissions. For manufactured goods like wooden furniture, GHG accounting methods were used to identify emissions hotspots across timber supply chains in China

[23]. They found upstream production processes drove most emissions, urging sourcing and transport optimisation for footprint reductions. Multiple studies have also examined environmental or carbon management accounting as a tool to support emissions management internally. Across Chinese

[23], Malaysian

[24][25], Vietnamese

[26], and Libyan

[27] manufacturers, the research found environmental management accounting adoption levels were still developing. Key barriers were a lack of resources, knowledge, and regulatory incentives. The analyses underscored the need for management understanding and commitment to leverage these accounting systems towards sustainability

[28]. Though carbon accounting techniques are advancing, it is noted that the complexity can still overwhelm practitioners, limiting organisational adoption and supply chain impacts

[29]. They called for simplified tools and cross-disciplinary collaboration to increase connectedness.

[30] also outlined research opportunities to address data reliability challenges in Indian supply chains through emerging technologies like blockchain and the Internet of Things.

Manufacturing organisations have not kept up with the best practices for comprehensively tracking and disclosing emissions sources. The authors in

[31] discussed how current carbon accounting methods declare bioenergy to be carbon-neutral, failing to account for biogenic CO

2 emissions at the point of combustion. This means emissions from industrial bioenergy processes often go unreported or are zeroed out in emissions reporting frameworks. Other analyses have shown how agricultural emissions receive much more scrutiny and mandatory reporting requirements compared to biogenic emissions from industry. The authors in

[32] demonstrated that many countries with climate commitments do not include some industrial process emissions like waste/biomass incineration in their national reporting. This leads to under-reporting of substantial indirect emissions in developed countries. Specifically looking at differences by industry, the authors in

[33] found that while agricultural methane emissions are comprehensively tracked and targeted for reduction by most countries, CO

2 emissions from bioenergy are categorically excluded from reduction targets. They argue this imbalance hinders effective, holistic climate mitigation policy. In terms of territorial versus polluter-pays emissions accounting, the author in

[34] discussed how under purely territorial accounting of emissions from traded biomass, substantial indirect emissions can go unreported. He advocated for improved emissions reconciliation and shared producer/consumer responsibility for bioenergy emissions. All these challenges add up to the need for manufacturing organisations to keep up with the carbon accounting practices that are evolving in other industries and sectors.

Overall, the literature reveals ongoing developments in carbon accounting. Still, a persistent need for standardisation, simplified tools, regulatory incentives, and skills development is needed to drive broader adoption across manufacturing supply chains. More empirical research into accounting techniques and digitisation opportunities can support the transition towards carbon transparency and emissions reductions in global manufacturing systems.

2.1. The Current Understanding of the Definition of Carbon Accounting in Manufacturing Systems and Supply Chains

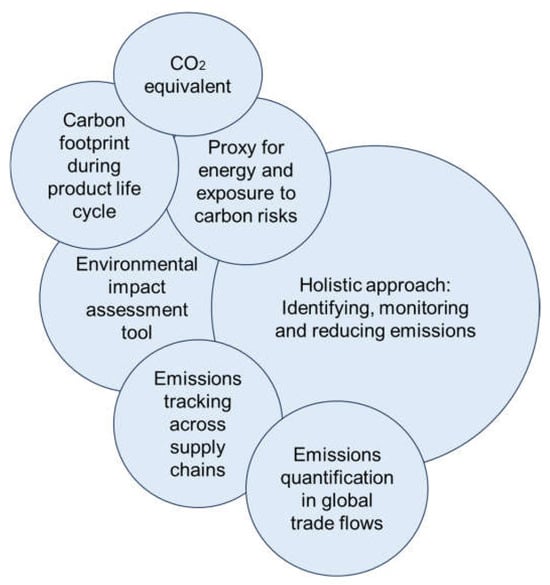

The concept of carbon accounting is fundamental in the context of manufacturing and supply chain management. Still, it is essential to note that there is no single universally accepted definition of this term within the literature. Nevertheless, some common themes have emerged, shedding light on the various aspects and purposes of carbon accounting. One perspective on carbon accounting is that it serves to quantify an organisation’s GHG emissions, typically expressed in terms of carbon dioxide equivalent. For instance, ref.

[18] describes carbon accounting as measuring the carbon dioxide equivalent emitted by any organisation. Similarly, ref.

[23] defines a product’s carbon footprint as the total carbon dioxide emissions and other GHGs during a product’s life cycle. In this view, carbon accounting is primarily seen as a tool for assessing the environmental impact of an entity. Expanding on this, ref.

[21] employs “

carbon emissions data as a proxy for energy use and, hence, exposure to rising carbon risks”. This suggests that carbon accounting not only measures emissions but also serves as an indicator of an organisation’s vulnerability to the challenges posed by carbon emissions. In this sense, carbon accounting can be viewed as a tool to quantify climate-related risks. Another broad definition of carbon accounting comes from

[29], which defines it as the “

measures of greenhouse gases produced by activities”. This definition encompasses a wide range of applications, from organisational emissions to product life cycles, emphasising the role of carbon accounting in assessing the environmental impact of various activities. Moreover, some researchers conceptualise carbon accounting as a more holistic approach that extends beyond measurement and instead focuses on identifying, monitoring, and ultimately reducing emissions. As ref.

[19] suggests, carbon accounting can “

improve GHG emission estimates and differentiate supply chains,” informing business and policy decisions about transitioning to a low-carbon future. Similarly, ref.

[21] argues that systematic carbon accounting and monitoring can help identify existing carbon exposure and serve as a starting point for developing strategies for carbon management. Here, carbon accounting plays a pivotal role in overall emissions management and sustainability efforts. Furthermore, carbon accounting is recognised for its significance in tracking emissions across complex supply chains. In

[35], carbon accounting is used to estimate the variable environmental impacts of agricultural commodity supply chains, while ref.

[36] applies it to quantify embodied emissions in global trade flows. In another example, ref.

[37] calculates the carbon footprint across a seafood product supply chain. These cases demonstrate the practical relevance of carbon accounting in understanding and mitigating emissions within intricate production networks.

In summary, as shown in Figure 1, the literature aligns around carbon accounting’s purpose as quantifying GHG emissions, especially across complete product life cycles and supply chains. It is predominately viewed as an emissions measurement tool, though some note its broader role in informing carbon management strategies. More standardised terminology could support the further development of carbon accounting approaches, tools, and applications across the manufacturing sector.

Figure 1. Various definitions of carbon accounting.

The Current Gaps Identified in Carbon Accounting in the Manufacturing Systems and Supply Chain Systems Literature

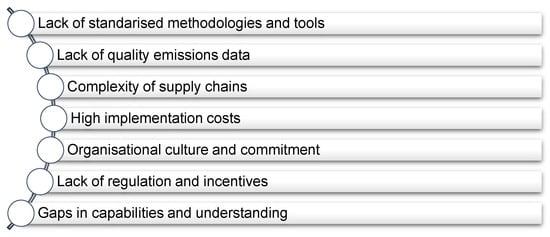

Numerous studies within the domain of carbon accounting in manufacturing supply chains have drawn attention to several critical gaps and challenges that need to be addressed for more effective and widespread adoption. One prominent theme that emerges from these studies is the need for standardisation and simplified tools in the field of carbon accounting. As pointed out by

[18], the proliferation of various carbon calculators, reporting standards, and certification schemes has created a confusing landscape, lacking a unified and practical framework that enterprises can readily employ for carbon accounting. This fragmentation can deter organisations from engaging in comprehensive carbon accounting efforts.

Another challenge pertains to the reliability and availability of data required for carbon accounting. Ref.

[30] identifies opportunities for leveraging emerging technologies such as blockchain and the Internet of Things to address data challenges in Indian supply chains. These technologies can enhance data transparency and accuracy, improving carbon accounting efforts’ quality.

Furthermore, studies have raised concerns about the narrow scope of carbon accounting efforts. For instance, ref.

[21] highlights that widely recognised guidelines like the GHG Protocol predominantly focus on direct or first-tier suppliers, potentially overlooking the broader carbon footprint associated with global trade flows. Ref.

[36] argues that addressing embodied emissions in global trade necessitates a more comprehensive approach to carbon management that spans across countries.

The Future Research Agenda for Carbon Accounting in Manufacturing Systems and Supply Chains

Carbon accounting in the context of manufacturing and supply chains presents a dynamic and evolving field, offering a promising avenue for future research and development. Several key themes emerge from the existing literature, which point towards the need for comprehensive and precise carbon accounting methods and tools to improve the accuracy of emissions estimation within complex global supply chains.

A recurring call in the literature, exemplified by studies such as

[19][20][21][38], emphasises the necessity for more robust carbon accounting practices. These calls stem from the recognition that reliable tools are essential to bolster confidence in climate-driven policy decisions and to bridge gaps in emissions data at the facility level of specific suppliers. By enhancing granularity and transparency in emissions data across various tiers of supply chains, stakeholders and policymakers can make informed decisions and foster more sustainable practices

[19][21].

Moreover, researchers advocate for the testing and refining of existing carbon accounting frameworks, tools, and implementation strategies through empirical research within the manufacturing sector. This area currently lacks substantial empirical evidence

[21][23][39]. For instance,

[21] suggests applying their carbon management framework to diverse industries to validate its effectiveness. At the same time, case studies and large-scale surveys are seen as valuable tools for gaining insights into successful carbon accounting practices

[21][39].

The Challenges of Carbon Accounting Implementation in Manufacturing Systems and Supply Chains

Addressing the challenges summarised in Figure 2 is essential for successfully implementing carbon accounting in manufacturing and supply chains. Standardisation, data quality improvement, supply chain transparency, cost-effective solutions, cultural change, regulatory support, and capacity building are all vital components in overcoming these hurdles and advancing the cause of sustainability in manufacturing and supply chains.

Figure 2. Challenges to carbon accounting in manufacturing and supply chains.

This entry is adapted from the peer-reviewed paper 10.3390/en17010010