+1 credit

+1 credit

| Version | Summary | Created by | Modification | Content Size | Created at | Operation |

|---|---|---|---|---|---|---|

| 1 | Dean Liu | -- | 2312 | 2022-10-24 01:41:02 |

Video Upload Options

The Herfindahl index (also known as Herfindahl–Hirschman Index, HHI, or sometimes HHI-score) is a measure of the size of firms in relation to the industry they are in and an indicator of the amount of competition among them. Named after economists Orris C. Herfindahl and Albert O. Hirschman, it is an economic concept widely applied in competition law, antitrust and also technology management. HHI is calculated by squaring the market share of each competing firm in the industry and then summing the resulting numbers,(sometimes limited to the 50 largest firms), where the market shares are expressed as fractions or points. The result is proportional to the average market share, weighted by market share. As such, it can range from 0 to 1.0, moving from a huge number of very small firms to a single monopolistic producer. Increases in the Herfindahl index generally indicate a decrease in competition and an increase of market power, whereas decreases indicate the opposite. Alternatively, if whole percentages are used, the index ranges from 0 to 10,000 "points". For example, an index of .25 is the same as 2,500 points. The major benefit of the Herfindahl index in relationship to such measures as the concentration ratio is that it gives more weight to larger firms. Other benefits of the Herfindahl index includes its simple calculation method and the small amount of easily obtainable data required for the calculation. The measure is essentially equivalent to the Simpson diversity index, which is a diversity index used in ecology; the inverse participation ratio (IPR) in physics; and the effective number of parties index in politics.

1. Example

For instance, we consider two cases in which the six largest firms produce 90% of the goods in a market. In either case, we will assume that the remaining 10% of output is divided among 10 equally sized producers.

- Case 1: All six of the largest firms produce 15% each.

- Case 2: The largest firm produces 80% and the next five largest firms produce 2% each.

The six-firm concentration ratio would equal 90% for both case 1 and case 2. But the first case would promote significant competition, where the second case approaches monopoly. The Herfindahl index for these two situations makes the lack of competition in the second case strikingly clear:

- Case 1: Herfindahl index = 6 * 0.152 + 10 * 0.012 = 0.136 (13.6%)

- Case 2: Herfindahl index = 0.802 + 5 * 0.022 + 10 * 0.012 = 0.643 (64.3%)

This behavior rests in the fact that the market shares are squared prior to being summed, giving additional weight to firms with larger size.

The index involves taking the market share of the respective market competitors, squaring it, and adding them together (e.g. in the market for X, company A has 30%, B, C, D, E and F have 10% each and G through to Z have 1% each). When calculating HHI the post merger level of the HHI score and the total increase of the HHI score are considered when reviewing the outcome. If the resulting figure is above a certain threshold then economists will consider the market to have a high concentration (e.g. market X's concentration is 0.142 or 14.2%). This threshold is considered to be 0.25 in the U.S.,[1] while the EU prefers to focus on the level of change, for instance that concern is raised if there is a 0.025 change when the index already shows a concentration of 0.1.[2] So to take the example, if in market X company B (with 10% market share) suddenly bought out the shares of company C (with 10% also) then this new market concentration would make the index jump to 0.162. Here it can be seen that it would not be relevant for merger law in the U.S. (being under 0.18) or in the EU (because there is not a change over 0.25).

2. Formula

- [math]\displaystyle{ H =\sum_{i=1}^N s_i^2 }[/math]

where si is the market share of firm i in the market, and N is the number of firms. Thus, in a market with two firms that each have 50 percent market share, the Herfindahl index equals 0.502+0.502 = 1/2.

The Herfindahl Index (H) ranges from 1/N to one, where N is the number of firms in the market. Equivalently, if percents are used as whole numbers, as in 75 instead of 0.75, the index can range up to 1002, or 10,000.

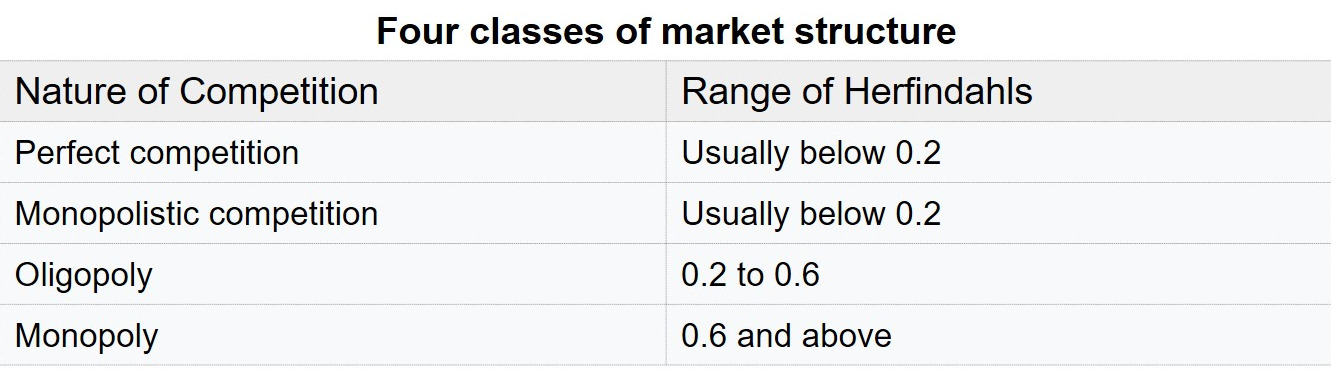

An H below 0.01 (or 100) indicates a highly competitive industry, Mergers and acquisitions with an increase of 100 points or less will usually not have any anti competitive effects and will require no further analysis.[3]

An H below 0.15 (or 1,500) indicates an unconcentrated industry. Mergers and acquisitions between 100 and 1500 points are unlikely to have anti-competitive effects and will most likely not need further analysis.[4]

An H between 0.15 and 0.25 (or 1,500 to 2,500) indicates moderate concentration. Mergers and acquisitions that result in moderate market concentration from HHI increases will raise anti-competitive concerns and will require further analysis.[5]

An H above 0.25 (above 2,500) indicates high concentration.[6] Mergers and acquisitions with HHI scores of 2500 or above will be considered anti competitive and an in-depth analysis produced, if the scores are well above 2500 they are considered to enhance market power they may only be allowed to progress when significant evidence is shown that the merger or acquisition will not increase market power.[7]

A small index indicates a competitive industry with no dominant players. If all firms have an equal share the reciprocal of the index shows the number of firms in the industry. When firms have unequal shares, the reciprocal of the index indicates the "equivalent" number of firms in the industry. Using case 2, we find that the market structure is equivalent to having 1.55521 firms of the same size.

There is also a normalized Herfindahl index. Whereas the Herfindahl index ranges from 1/N to one, the normalized Herfindahl index ranges from 0 to 1. It is computed as:

- [math]\displaystyle{ H^* = {\left ( H - 1/N \right ) \over 1-1/N } }[/math] for N > 1 and

- [math]\displaystyle{ H^* = 1 }[/math] for N = 1

where again, N is the number of firms in the market, and H is the usual Herfindahl Index, as above. Using the normed Herfindahl index, information about the total number of players (N) is lost, as shown in the following example: Assume a market with two players and equally distributed market share; H = 1/N = 1/2 = 0.5 and H* = 0. Now compare that to a situation with three players and again an equally distributed market share; H = 1/N = 1/3 = 0.333..., note that H* = 0 like the situation with two players. The market with three players is less concentrated, but this is not obvious looking at just H*. Thus, the normalized Herfindahl index can serve as a measure for the equality of distributions, but is less suitable for concentration.

3. Problems

The usefulness of this statistic to detect monopoly formation, however, is directly dependent on a proper definition of a particular market (which hinges primarily on the notion of substitutability). The index fails to take into consideration the complex nature of the market being tested.[8]

- For example, if the statistic were to look at a hypothetical financial services industry as a whole, and found that it contained 6 main firms with 15% market share apiece, then the industry would look non-monopolistic. However, suppose one of those firms handles 90% of the checking and savings accounts and physical branches (and overcharges for them because of its monopoly), and the others primarily do commercial banking and investments. In this scenario, people would be suffering due to a market dominance by one firm; the market is not properly defined because checking accounts are not substitutable with commercial and investment banking. The problems of defining a market work the other way as well. To take another example, one cinema may have 90% of the movie market, but if movie theaters compete against video stores, pubs and nightclubs then people are less likely to be suffering due to market dominance.

- Another typical problem in defining the market is choosing a geographic scope. For example, firms may have 20% market share each, but may occupy five areas of the country in which they are monopoly providers and thus do not compete against each other. A service provider or manufacturer in one city is not necessarily substitutable with a service provider or manufacturer in another city, depending on the importance of being local for the business—for example, telemarketing services are rather global in scope, while shoe repair services are local.

The United States federal anti-trust authorities such as the Department of Justice and the Federal Trade Commission use the Herfindahl index as a screening tool to determine whether a proposed merger or acquisition is likely to raise antitrust concerns. Increases of over 0.01(100) generally provoke scrutiny, although this varies from case to case. The Antitrust Division of the Department of Justice considers Herfindahl indices between 0.15 (1500) and 0.25 (2500) to be "moderately concentrated" and indices above 0.25 to be "highly concentrated".[9] However, these indices scores are not rigid guidelines that must be followed, while high levels of concentration is concerning, they indices scores provide ways to identify which mergers and acquisitions are potentially noncompetitive. There are other factors that need to be considered that will either help reinforce or counter the harmful effects of higher market concentration. The Herfindahl-Hirschman index is used as a starting point to gauge initial market power and then determine if additional information is needed to conduct further analysis on any potential anti-competitive concerns.[10]

4. Intuition

When all the firms in an industry have equal market shares, H = N(1/N)2 = 1/N. The Herfindahl is correlated with the number of firms in an industry because its lower bound when there are N firms is 1/N. In the more general case of unequal market share, 1/H is called "equivalent (or effective) number of firms in the industry", Neqi or Neff.[11] An industry with 3 firms cannot have a lower Herfindahl than an industry with 20 firms when firms have equal market shares. But as market shares of the 20-firm industry diverge from equality the Herfindahl can exceed that of the equal-market-share 3-firm industry (e.g., if one firm has 81% of the market and the remaining 19 have 1% each H=0.658). A higher Herfindahl signifies a less competitive industry.

4.1. Appearance in Market Structure

It can be shown that the Herfindahl index arises as a natural consequence of assuming that a given market's structure is described by Cournot competition.[12] Suppose that we have a Cournot model for competition between [math]\displaystyle{ n }[/math] firms with different linear marginal costs and a homogeneous product. Then the profit of the [math]\displaystyle{ i }[/math]th firm [math]\displaystyle{ \pi_{i} }[/math] is:[math]\displaystyle{ \pi_{i} = P(Q)q_{i} - c_{i}q_{i}, \quad Q = \sum_{i=1}^{n}q_{i} }[/math]where [math]\displaystyle{ q_{i} }[/math] is the quantity produced by each firm, [math]\displaystyle{ c_{i} }[/math] is the marginal cost of production for each firm, and [math]\displaystyle{ P(Q) }[/math] is the price of the product. Taking the derivative of the firm's profit function with respect to its output to maximize its profit gives us:[math]\displaystyle{ {\partial\pi_{i}\over{\partial q_{i}}} = 0 \implies P'(Q)q_{i} + P(Q) - c_{i} =0 \implies -{dP\over{dQ}}q_{i} = P-c_{i} }[/math]Dividing by [math]\displaystyle{ P }[/math] gives us each firm's profit margin:[math]\displaystyle{ {P-c_{i}\over{P}} = -{dP\over{dQ}}{q_{i}\over{P}} = -{dP/P\over{dQ/Q}} {q_{i}\over{Q}} = {s_{i}\over{\eta}} }[/math]where [math]\displaystyle{ s_{i} = q_{i}/Q }[/math] is the market share and [math]\displaystyle{ \eta = -d\log Q/d\log P }[/math] is the elasticity of demand. Multiplying each firm's profit margin by its market share gives us:[math]\displaystyle{ s_{1}\left( {P-c_{1}\over{P}} \right) + \cdots + s_{n}\left( {P-c_{n}\over{P}} \right) = {H\over{\eta}} }[/math]where [math]\displaystyle{ H }[/math] is the Herfindahl index. Therefore, the Herfindahl index is directly related to the weighted average of the profit margins of firms under Cournot competition with linear marginal costs.

4.2. Effective Assets in a Portfolio

The Herfindahl index is also a widely used metric for portfolio concentration.[13] In portfolio theory, the Herfindahl index is related to the effective number of positions [math]\displaystyle{ N_{\text{eff}} = 1/H }[/math][14] held in a portfolio, where [math]\displaystyle{ H = \|w\|^{2} }[/math] is computed as the sum of the squares of the proportion of market value invested in each security. A low H-index implies a very diversified portfolio: as an example, a portfolio with [math]\displaystyle{ H = 0.02 }[/math] is equivalent to a portfolio with [math]\displaystyle{ N_{\text{eff}} = 50 }[/math] equally weighted positions. The H-index has been shown to be one of the most efficient measures of portfolio diversification.[15]

It may also be used as a constraint to force a portfolio to hold a minimum number of effective assets:[math]\displaystyle{ \|w\|^{2} \leq N_{\text{eff}}^{-1} }[/math]For commonly used portfolio optimization techniques, such as mean-variance and CVaR, the optimal solution may be found using second-order cone programming.

5. Decomposition

Supposing that [math]\displaystyle{ N }[/math] firms share all the market, each one with a participation of [math]\displaystyle{ x_i }[/math] and market share [math]\displaystyle{ s_i=x_i/\sum_{j=1}^N x_j }[/math], then the index can be expressed as [math]\displaystyle{ H =\frac1N+N\sigma^2 }[/math], where [math]\displaystyle{ \sigma^2 }[/math] is the statistical variance of the firm shares, defined as [math]\displaystyle{ \sigma^2=\frac1{N-1} \sum_{i=1}^N\left(s_i-\mu\right)^2 }[/math] where [math]\displaystyle{ \mu=\frac1N }[/math] is the mean of participations. If all firms have equal (identical) shares (that is, if the market structure is completely symmetric, in which case [math]\displaystyle{ s_i=1/N }[/math]) then [math]\displaystyle{ \sigma^2 }[/math] is zero and [math]\displaystyle{ H }[/math] equals [math]\displaystyle{ 1/N }[/math]. If the number of firms in the market is held constant, then a higher variance due to a higher level of asymmetry between firms' shares (that is, a higher share dispersion) will result in a higher index value. See the Brown and Warren-Boulton (1988) and Warren-Boulton (1990) texts cited below.

References

- 2010 Merger Guidelines § 5.3

- However, it gets far more complicated than that. See para. 16-21 Guidelines on horizontal mergers

- "Horizontal Merger Guidelines (08/19/2010)" (in en). 2015-06-25. https://www.justice.gov/atr/horizontal-merger-guidelines-08192010.

- "Horizontal Merger Guidelines (08/19/2010)" (in en). 2015-06-25. https://www.justice.gov/atr/horizontal-merger-guidelines-08192010.

- "Horizontal Merger Guidelines (08/19/2010)" (in en). 2015-06-25. https://www.justice.gov/atr/horizontal-merger-guidelines-08192010.

- "Horizontal Merger Guidelines (08/19/2010)". https://www.justice.gov/atr/public/guidelines/hmg-2010.html.

- "Horizontal Merger Guidelines (08/19/2010)" (in en). 2015-06-25. https://www.justice.gov/atr/horizontal-merger-guidelines-08192010.

- Hayes, Adam. "Herfindahl-Hirschman Index (HHI) Definition" (in en). https://www.investopedia.com/terms/h/hhi.asp.

- "Herfindahl–Hirschman Index". USDOJ. https://www.justice.gov/atr/public/guidelines/hhi.html.

- "Horizontal Merger Guidelines (08/19/2010)" (in en). 2015-06-25. https://www.justice.gov/atr/horizontal-merger-guidelines-08192010.

- Saxena, Nidhi (2011-04-26). "Herfindal Hirschman Index". Essays For Student.com. https://www.essaysforstudent.com/term-paper/Herfindal-Hirschman-Index/94112.html. "If all firms have equal share the reciprocal of the index shows the number of firms in the industry. When the firms have unequal share the reciprocal of the index indicates the equivalent number of firms in the industry"

- Viscusi, W. Kip; Harrington, Jr., Joseph E.; Vernon, John M. (2005). Economics of Regulation and Antitrust (4th ed.). Cambridge, MA: The MIT Press. pp. 159–161. ISBN 9780262220750. https://mitpress.mit.edu/books/economics-regulation-and-antitrust-fourth-edition.

- Lovett, William (1988). Banking and Financial Institutions Law in a Nutshell. West Publishing Co..

- Bouchaud, Jean-Philippe; Potters, Aguilar (1997). Missing Information and Asset Allocation.

- Woerheide, Walt; Persson, Don (1993). "An Index of Portfolio Diversification". Financial Services Review 2 (2): 73–85. doi:10.1016/1057-0810(92)90003-U. https://pdfs.semanticscholar.org/0a5e/ec924dae3ea30b6cae8e66f7070344d47631.pdf.