+1 credit

+1 credit

| Version | Summary | Created by | Modification | Content Size | Created at | Operation |

|---|---|---|---|---|---|---|

| 1 | Maw Maw Tun | + 1837 word(s) | 1837 | 2020-11-04 09:48:36 | | | |

| 2 | Vicky Zhou | Meta information modification | 1837 | 2020-11-16 08:46:21 | | | | |

| 3 | Vicky Zhou | -99 word(s) | 1738 | 2020-11-16 08:49:27 | | | | |

| 4 | Maw Maw Tun | -4 word(s) | 1734 | 2020-11-16 10:59:09 | | |

Video Upload Options

Renewable waste-to-energy in Southeast Asia is a kind of renewable and alternative energy gained from waste resource that most Southeast Asian countries explore and utilize not only to minimize the waste crisis but also to meet the actual fossil-free high demand [2] but also to reduce greenhouse gas emissions and other environmental impacts from the energy sector [9] across the region.

1. Introduction

As the world hurtles toward its urban future, the amount of municipal solid waste (MSW), one of the most important by-products of an urban lifestyle, is growing even faster than the rate of urbanization [1]. The amount of MSW generation of the cities around the world might increase from 1.3 billion tons per year to 2.2 by 2025, and waste generation rates might double over the next two decades in developing countries [1][2].

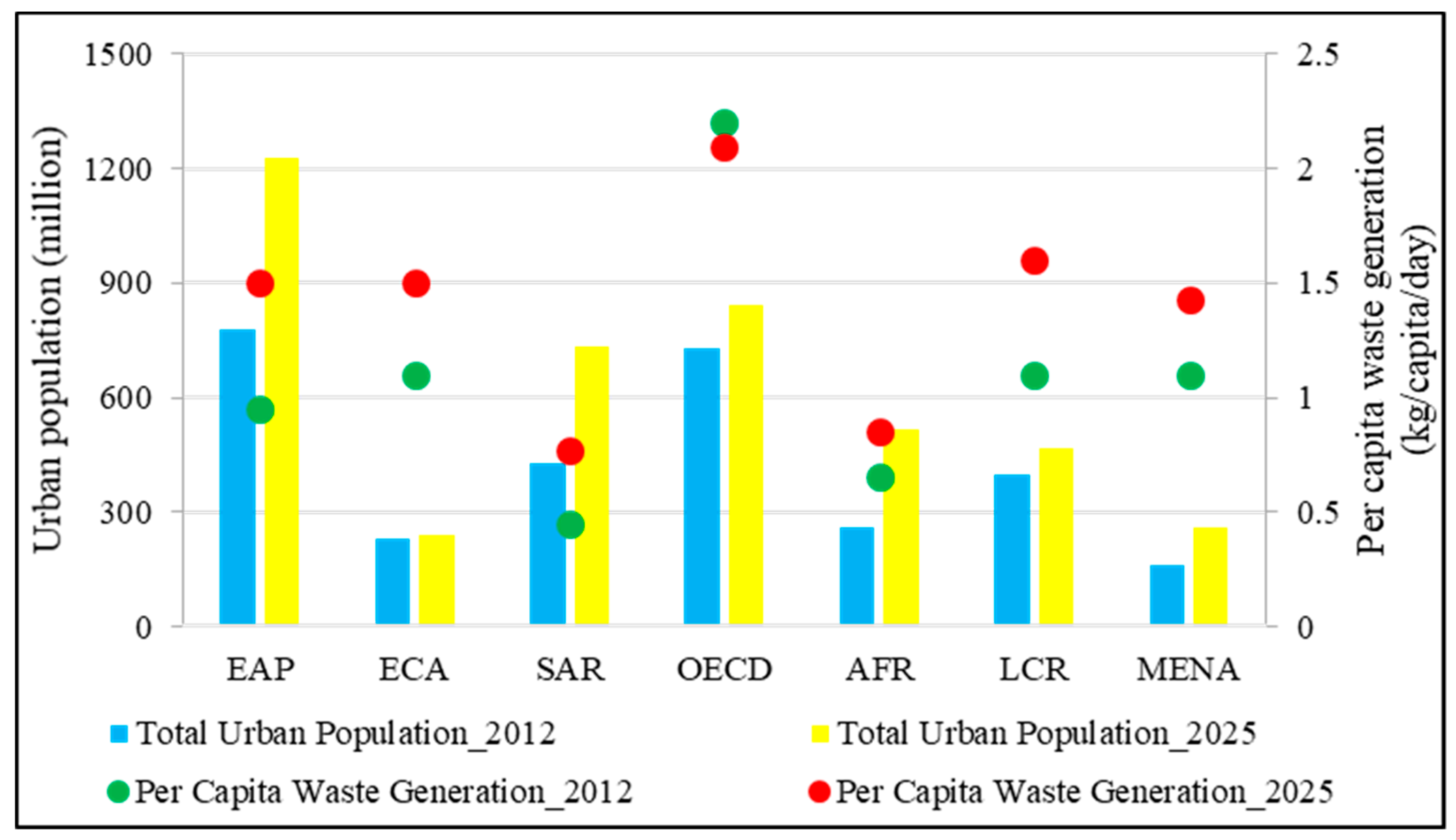

The East Asia and Pacific (EAP) region has a higher urban population than other regions, and it is projected to reach 1229 million in 2025, up from 777 million in 2012 (Figure 1). Despite the lower per capita waste generation rate in the region compared to the Organization for Economic Co-operation and Development (OECD) in 2012, it will be increased by 60% in 2025. Since the Southeast Asian countries (Brunei Darussalam, Cambodia, Indonesia, Laos PDR, Malaysia, Myanmar, Philippines, Singapore, Thailand, and Vietnam) belong to the East Asia and Pacific region, the annual urban population of these countries, as per the World Bank Report [1], is expected to grow considerably by 2025, hence increasing the amount of annual waste generation. However, only 30–70% of waste can be collected in most developing countries, including Myanmar, Laos PDR, and Cambodia, whereas developed countries have a 76–100% collection efficiency [1][3].

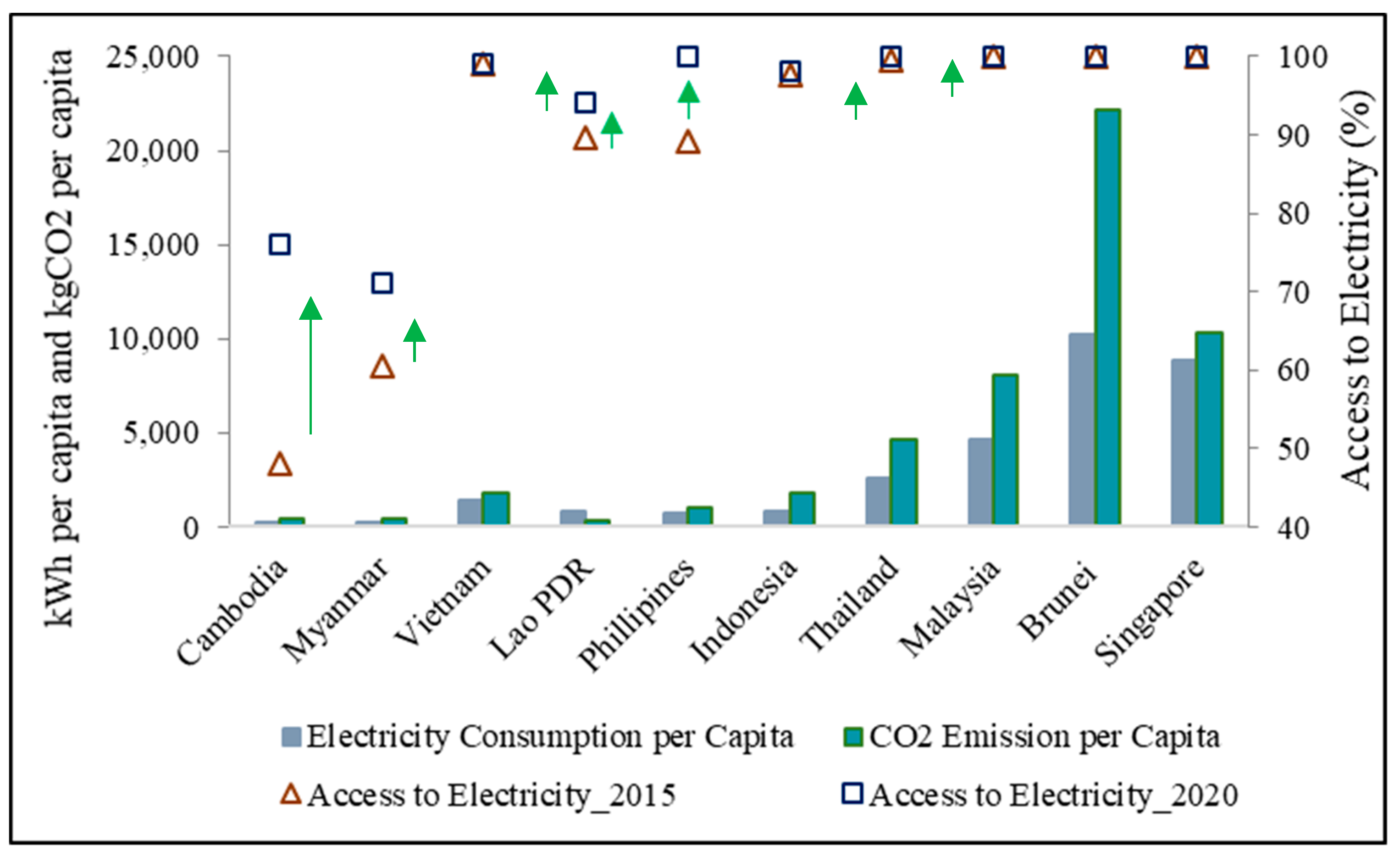

With accelerated urbanization, economic growth, and changing lifestyles [4], Southeast Asia’s urban population is projected to rise to nearly 400 million by 2030 [5]. Additionally, the growth of electricity demand is also prompting countries to more than double generation capacity by 2040 [5]. The projected rise of energy demand in Southeast Asia will have a considerable effect on CO2 emissions, which are projected to rise from 3.5% today to 5% by 2030 [6][7]. Figure 2 shows the access to electricity, per capita electricity consumption, and per capita CO2 emission in Southeast Asian countries. Per capita electricity consumption in the majority of the countries is below 2500 kWh per capita, and their per capita CO2 emissions are below 4500 kg. The average carbon emission in Southeast Asian countries has been increased by over 5% due to the fast economic growth in the region [8][9]. Though Singapore, Malaysia, Brunei Darussalam, and Thailand have already allowed 100% access to their electricity, other countries like Philippines and Vietnam are projecting to reach this 100% access by 2020 [9].

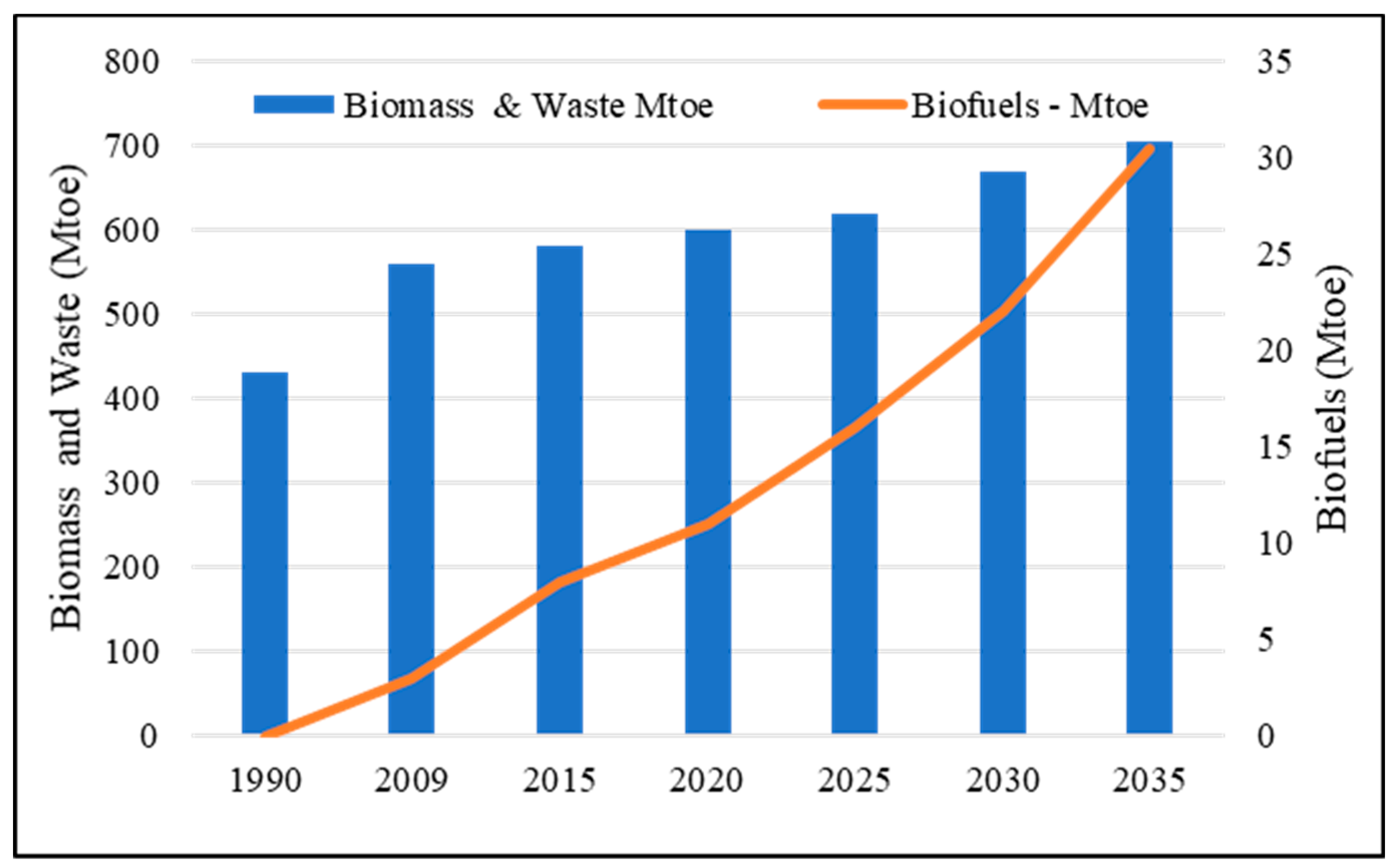

The total electricity generation from the renewables and non-renewables in the Southeast Asia region amounted to approximately 856 terawatt-hours (TWh) in 2014, out of which 20% came from renewable energy (74.1% hydropower, 12.6% biofuels, 11.5% geothermal, 1.2% solar photovoltaic (PV), and 0.6% wind) [10]. As shown in Figure 3, the bioenergy demand in non-OECD Asia is projected to grow dramatically by 2035. It has been observed that the demand for biofuels in this region will potentially rise from 2 million tons of oil equivalent (Mtoe) in 2009 to over 30 Mtoe in 2035, whereas the demand for biomass and waste might be increased by approximately 50% from 480 Mtoe in 1990 to over 700 Mtoe in 2035.

2. Waste to Energy in Asia

Due to the potential depletion of fossil fuel and climate change, Southeast Asian countries have looked to renewable and alternative energies to reduce greenhouse gas emissions and other environmental impacts from the energy sector [9]. On the other hand, the growing urban population will accelerate the amount of annual waste generation (approximately 97 million tons per year in 2015 to 165 million tons per year by 2025) in these countries [1][12], requiring significant investment in waste management to cope with the increase in waste [5]. The rapid urban population growth that has boosted waste generation and electricity demand has led to a possible alternative solution in Southeast Asia. Waste-to-energy—a catch-all for different technologies that allow countries to get rid of waste and generate electricity at the same time—is one obvious and quick solution to these two needs [5]. Therefore, the technologies constitute a meeting point for the waste management and energy sectors to work together and benefit from each other in the most efficient manner [2].

Actually, waste-to-energy is also a kind of biomass energy, offering benefits not only to minimize the waste crisis but also to meet the actual fossil-free high demand [2] and to reduce the greenhouse gas emissions and climate change impacts [13]. Nowadays, it has become a type of renewable energy utilization that can provide environmental and economic benefits in the world [13]. Currently, there are more than 2200 thermal waste treatment plants all over the world with a total capacity of 300 million tons per year, and it has been estimated that more than 600 new waste-to-energy facilities will be built with a capacity of 170 million tons per year by 2025 [2][14]. China had 7.3 gigawatts of energy production across 339 power plants in 2017, and they are expecting to grow to 10 gigawatts and 600 plants by 2020 [5]. The selection of the most suitable technology is based on social, economic, and technical factors, as well as environmental strategies to ensure the best outcomes [2]. In Europe, the most widespread options for upgrading waste treatment are the incineration of grey waste and anaerobic digestion (AD), often combined with the composting of the separated fraction of organic waste [3]. When it comes to waste-to-energy plants, there are regional preferences—gasification is in favor in South Asia, while grate incineration is generally used in Europe [3].

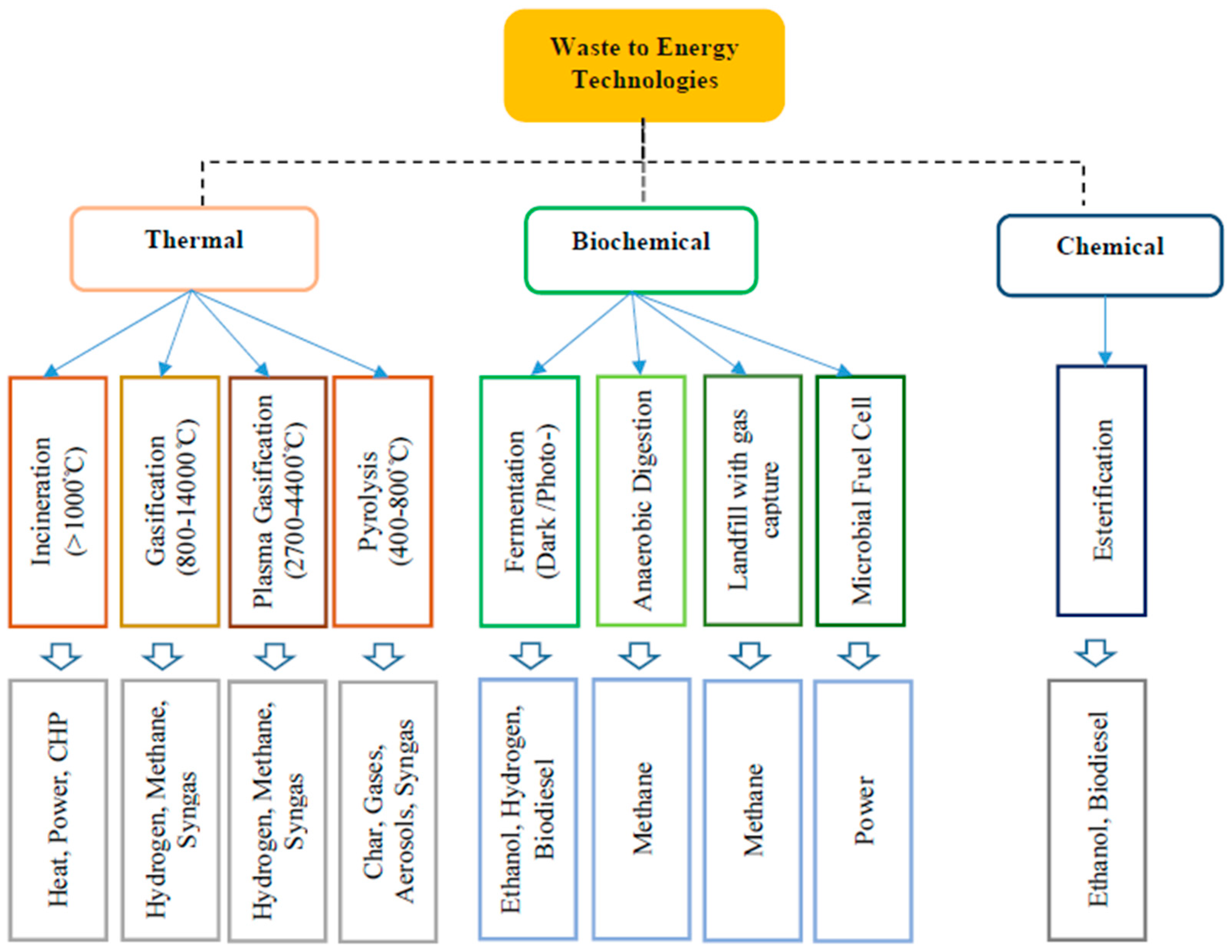

As described in Figure 4, the most common waste-to-energy technologies in the developing world include [2][15][16][17];

(i) Thermal conversion (incineration, pyrolysis, gasification, and plasma gasification).

(ii) Biochemical conversion (fermentation, anaerobic digestion, landfills with gas capture, and microbial fuel cell).

(iii) Chemical conversion (esterification).

The future trends in the area are in the direction of biological hydrogen production (photo-biological process and dark fermentation), bio-electrochemical processes (microbial fuel cells (MFCs), microbial electrolysis cells (MECs), and hydrothermal carbonization [2].

Technologies such as the incineration process have been advantageous, not only for reductions in the mass and volumes of initial waste but also for energy recovery and the reduction of land use for landfills [18]. When incinerated, waste can be reduced to 80–85% by weight and 95–96% by volume [19]. Additionally, incineration can be considered as a net greenhouse gas (GHG) reducer if GHG reductions, achieved by accounting for waste-to-energy, exceed GHG emissions [20].

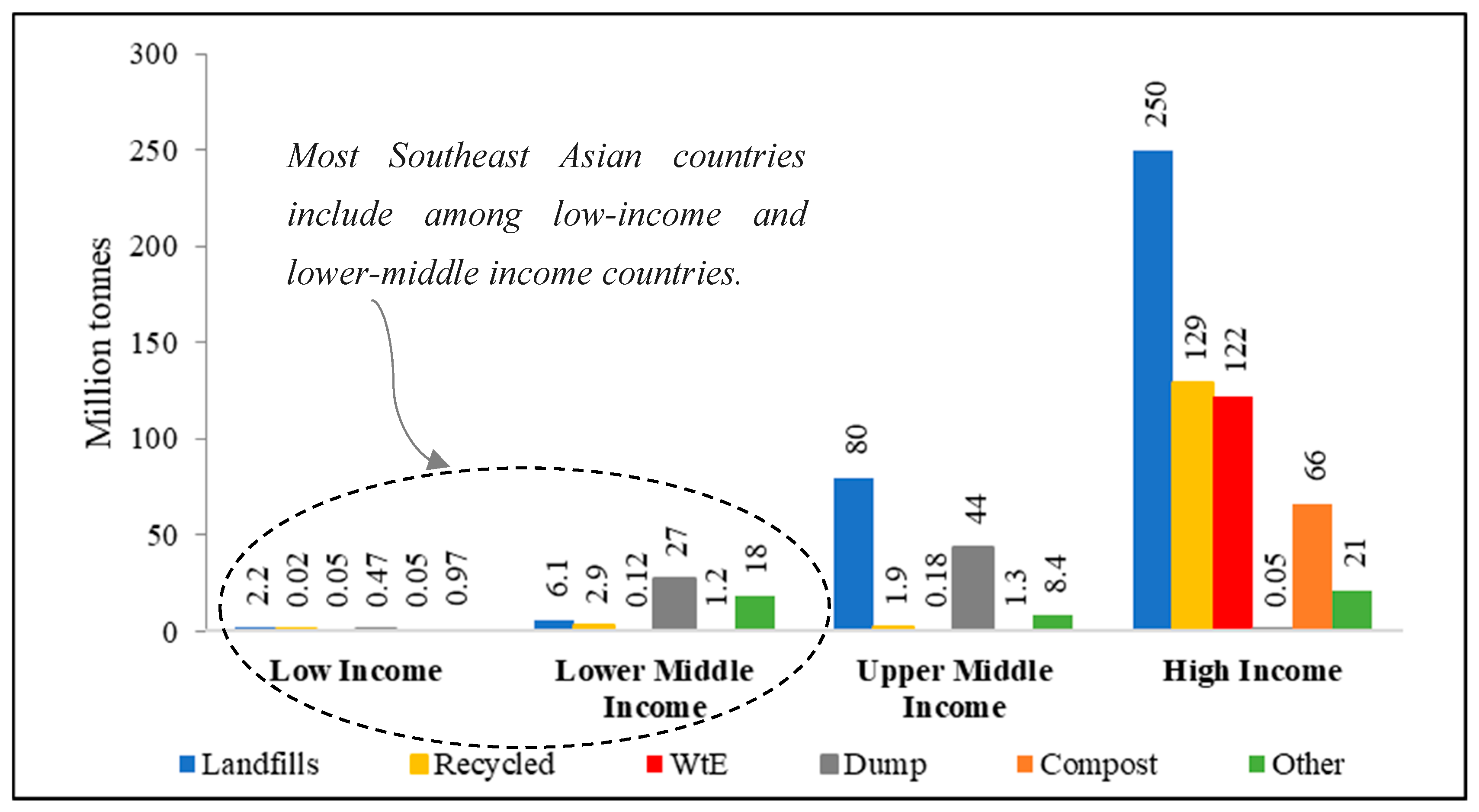

Nowadays, waste-to-energy plants are most often tailor made, depending on very specific local requirements. Thus, construction costs vary widely, and a typical range in Europe is around 500–700 Euro per ton per year in installed capacity, not including the cost for the site and project development [21]. Globally, the estimated cost for the waste-to-energy technologies in the lower middle income countries is in the range of 40–100 US dollar (USD) per ton for incineration and 20–80 USD per ton for anaerobic digestion (AD), while the estimated cost in high income countries is in the range of 70–200 USD per ton for incineration and 65–150 USD per ton for AD [1]. Figure 5 illustrates that the application of waste-to-energy technologies in low-income and lower middle-income countries is merely at the development stage compared to the upper middle-income and high-income countries, which are actively using these technologies.

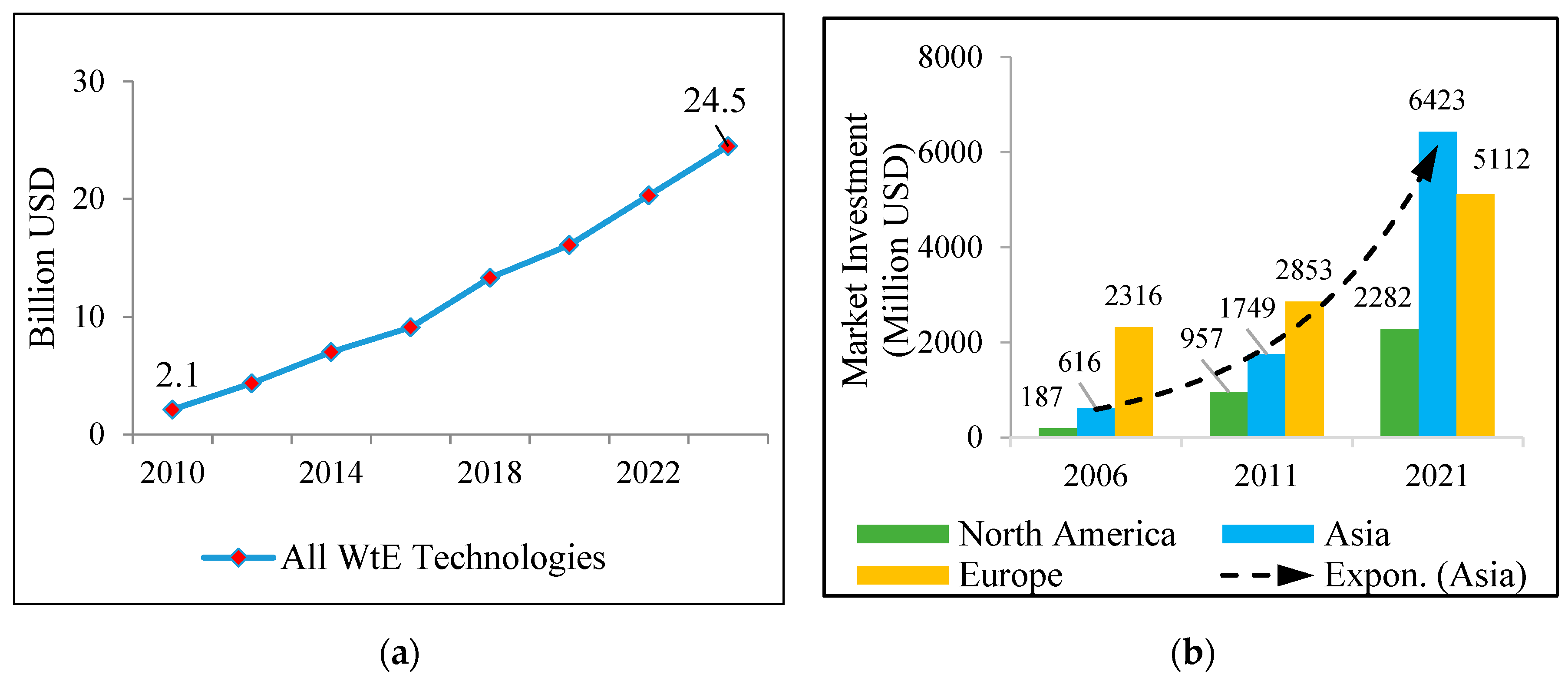

In Figure 6a, the forecast shows that, globally, the growth of waste-to-energy technologies is projected to reach 24.5 million USD in 2024 from 2.1 million USD in 2010. Meanwhile, the regional market investment in incineration in Asia will have grown from 616 million USD in 2006 to 6463 million USD in 2021, representing an investment increase by a factor of 10 (Figure 6b). Additionally, the Asia-Pacific waste-to-energy market is projected to grow at an annual rate of over 15% and will reach a value of 13.66 billion USD by 2023 [22]. Thus, it is seen that the waste-to-energy sector in Asia has a great potential in technological transfer and investment [15][23].

Currently, waste incineration is uncommon in developing countries, and, generally, it is not successful or experiences financial and operational difficulties due to the high capital cost of the plant, operation and maintenance costs, the high moisture content of MSW, and the need for sorting facilities and pretreatment processes [1][18]. However, energy-oriented conversion technologies for waste-to-fuel and waste-to-energy have been well-developed around the world to create energy/fuel from waste, reduce dependency on fossil fuel, reduce land use for waste disposal, and ensure socio-economic and environmental benefits [24][25][26]. Though there is still a long way until a global sustainable waste management strategy is achieved [15], developing countries can learn the lessons about and gain technology transfers from the waste-to-energy technologies and waste management practices in developed countries.

Nowadays, most Southeast Asian countries are facing several issues related to waste management, such as the increasing annual waste generation that has required more waste disposal sites, the scarcity of land areas, environmental pollution, and growth in energy demand [4][5][7][27]. Since these issues are especially important to be tackled in Southeast Asia, waste-to-energy technologies can play an essential role in sustainable waste management and the relief of environmental matters [17][25][26]. Meanwhile, some aspects such as regulation, finance, and technological suitability should be carefully considered to develop the waste-to-energy sector in the region [2][12][15][16][18][24].

Several studies have, to a reasonable extent, overviewed, analyzed, and evaluated the waste management and waste-to-energy sectors in Southeast Asian countries [1][28], but most have focused on the waste-to-energy sector in specific countries such as Thailand [29][30], Malaysia [31][32][33], Vietnam [17], and Myanmar [13]. Despite some issues such as public perception, public–private partnerships, all stakeholder involvement, funding, and climate factors, some Southeast Asian countries have made a reasonably successful step toward waste-to-energy technologies. Therefore, this study aimed to highlight an overview of the waste-to-energy sector in Southeast Asian countries to specify the status, challenges, opportunities, and selection of technologies suited for a specific country. As a major contribution, the study especially focuses on waste-to-energy alternatives, their potential, and the feasibility to implement them in the Southeast Asian countries where important data are not available.

References

- Hoornweg, D.; Bhada-Tata, P. What a Waste: A Global Review of Solid Waste Management; Urban Development Series; Knowledge Papers No. 15; World Bank: Washington, DC, USA, 2012.

- Edo, M.; Johansson, I. International perspectives of energy from waste—Challenges and trends. In Proceedings of the IRRC Waste-to-Energy Conference, Vienna, Austria, 1–2 October 2018.

- International Energy Agency (IEA). Waste-to-Energy. Summary and Conclusions from the IEA Bioenergy ExCo71 Workshop; ExCo:2014:03; IEA Bioenergy: Vienna, Austria, 2013; pp. 1–24.

- Curea, C. Sustainable societies and municipal solid waste management in Southeast Asia. In Sustainable Asia: Supporting the Transition to Sustainable Consumption and Production in Asian Developing Countries; Schroeder, P., Anggraeni, K., Sartori, S., Weber, U., Eds.; World Scientific Publishing Company: Singapore, 2017; pp. 391–415.

- Weatherby, C. Waste-to-Energy: A Renewable Opportunity for Southeast Asia? Available online: https://chinadialogue.net/en/energy/11093-waste-to-energy-a-renewable-opportunity-for-southeast-asia/ (accessed on 5 July 2020).

- International Energy Agency (IEA). Energy Balances of Non-OECD Countries; IEA/OECD: Paris, France, 2009.

- Ölz, S.; Beerepoot, M. Deploying Renewables in Southeast Asia: Trends and Potentials; International Energy Agency: Paris, France, 2010; pp. 7–157.

- Bakhtyar, B.; Sopian, K.; Sulaiman, M.Y.; Ahmad, S.A. Renewable Energy in Five South East Asian Countries: Review on Electricity Consumption and Economic Growth. Renew. Sustain. Energy Rev. 2013, 26, 506–514.

- Tun, M.M.; Juchelkova, D.; Win, M.M.; Thu, A.M.; Puchor, T. Biomass energy: An overview of biomass sources, energy potential, and management in Southeast Asian countries. Resources 2019, 8, 81.

- Tun, M.M.; Juchelkova, D. Biomass Sources and Energy Potential for Energy Sector in Myanmar: An Outlook. Resources 2019, 8, 102.

- Damen, B. Sustainable Bioenergy in Southeast Asia An FAO Perspective. Available online: www.fao.org/bioenergy/en/ (accessed on 5 July 2020).

- Modak, P.; Pariatamby, A.; Seadon, J.; Bhada-Tata, P. International Solid Waste Association. Asia Waste Management Outlook; United Nations Environment Programme: Manama, Bahrain, 2017.

- Tun, M.M.; Juchelková, D.; Raclavská, H.; Sassmanová, V. Utilization of biodegradable wastes as a clean energy source in the developing countries: A case study in Myanmar. Energies 2018, 11, 3183.

- Ecoprog. Waste-to-Energy 2016/2017. Technologies, Plants, Projects and Backgrounds of the Global Thermal Waste Treatment Business (Extract). 2016. Available online: https://www.ecoprog.com/fileadmin/user_upload/extract_market_report_WtE_2019-2020_ecoprog.pdf (accessed on 6 July 2020).

- Marshall, J.; Hoornweg, D.; Eremed, W.B.; Piamonti, G. World Energy Resources Waste-to-Energy; World Energy Council: London, UK, 2016; pp. 5–60. ISBN 978-0-946121-58-8.

- RPG Group. Project Proposal: Waste-to-Energy Technology, Policy and Investment Perspective. Raymond Tech Australia. Available online: http://www.raymondtech.com.au/docs/Waste_to_Energy%20Proposal.pdf (accessed on 5 July 2020).

- Hoang, N.H.; Fogarassy, C. Sustainability Evaluation of Municipal Solid Waste Management System for Hanoi (Vietnam)—Why to Choose the ‘Waste-to-Energy’ Concept. Sustainability 2020, 12, 1085.

- Tun, M.M.; Juchelková, D. Problems with Biodegradable Wastes—Potential in Myanmar and Other Asian Countries for Combination of Drying and Waste Incineration. In Proceedings of the IRRC Waste-to-Energy Conference, Vienna, Austria, 1–2 October 2018.

- Kreith, F. Waste to Energy Combustion. In Handbook of Solid Waste Management, 2nd ed.; Tchobanoglous, G., Kreith, F., Eds.; McGraw-Hill: New York, NY, USA, 2002; pp. 1–176.

- Tomohiro, T. In: Waste-to-energy incineration plants as greenhouse gas reducers: A case study of seven Japanese metropolises. Waste Manag. Res. 2013, 31, 1110–1117.

- European Suppliers of Waste-to-Energy Technology (ESWET). Everything You Always Wanted to Know about Waste-to-Energy. Available online: http://www.eswet.eu/tl_files/eswet/5.%20Documents/5.1.%20Waste-to-Energy%20Handbook/ESWET_Handbook_Waste-to-Energy.pdf (accessed on 7 August 2020).

- Lim, W.B.; Yuen, E.; Bhaska, A.R. Waste-to-Energy: Green Solutions for Emerging Markets. 2019. Available online: https://home.kpmg/xx/en/home/insights/2019/10/waste-to-energy-green-solutions-for-emerging-markets.html (accessed on 9 August 2020).

- Ouda, O.K.M.; Raza, S.A. Waste-to-Energy: Solution for Municipal Solid Waste Challenges—Global Perspective. In Proceedings of the 2014 International Symposium on Technology Management and Emerging Technologies, Bandung, Indonesia, 27–29 May 2014.

- Tun, M.M.; Juchelková, D. Drying Methods for Municipal Solid Waste Quality Improvement in the Developed and Developing Countries: A Review. Environ. Eng. Res. 2019, 24, 529–542.

- Brunner, P.H.; Rechberger, H. Waste-to-energy—Key element for sustainable waste management. Waste Manag. 2015, 37, 3–12.

- Di Matteo, U.; Nastasi, B.; Albo, A.; Astiaso Garcia, D. Energy contribution of OFMSW (Organic Fraction of Municipal SolidWaste) to energy-environmental sustainability in urban areas at small scale. Energies 2017, 10, 229.

- Choudhury, A.R. Environmental Sustainability: Coping with Raising Volume of Urban Waste. Available online: www.ramkyenviroengineers.com (accessed on 7 July 2020).

- Mutz, D.; Hengevoss, D.; Hugi, C.; Gross, T. Waste-to-Energy Options in Municipal Solid Waste Management a Guide for Decision Makers in Developing and Emerging Countries; Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH: Eschborn, Germany, 2017.

- Intharathirat, R.; Salam, P.A. Valorization of MSW-to-energy in Thailand: Status, challenges and prospects. Waste Biomass Valorization 2016, 7, 31–57.

- Jacob, P.; Kashyap, P.; Visvanathan, C. Overview of municipal solid waste—Waste-to-energy in Thailand. International Brainstorming on Waste to Energy in India, Mumbai, India, 25 June 2013.

- Tan, S.T.; Ho, W.S.; Hashim, H.; Lee, C.T.; Taib, M.R.; Ho, C.S. Energy, economic and environmental (3E) analysis of waste-to-energy (WTE) strategies for municipal solid waste (MSW) management in Malaysia. Energy Convers. Manag. 2015, 102, 111–120.

- Yong, Z.J.; Bashir, M.J.; Ng, C.A.; Sethupathi, S.; Lim, J.W.; Show, P.L. Sustainable Waste-to-Energy Development in Malaysia: Appraisal of Environmental, Financial, and Public Issues Related with Energy Recovery from Municipal Solid Waste. Processes 2019, 7, 676.

- Aja, O.C.; Al-Kayiem, H.H. Review of municipal solid waste management options in Malaysia, with an emphasis on sustainable waste-to-energy options. J. Mater. Cycles Waste Manag. 2014, 16, 693–710.