Your browser does not fully support modern features. Please upgrade for a smoother experience.

Submitted Successfully!

+1 credit

+1 credit

Thank you for your contribution! You can also upload a video entry or images related to this topic.

For video creation, please contact our Academic Video Service.

| Version | Summary | Created by | Modification | Content Size | Created at | Operation |

|---|---|---|---|---|---|---|

| 1 | Huibrecht Margaretha Van der Poll | + 2598 word(s) | 2598 | 2021-09-24 10:17:44 | | | |

| 2 | Vicky Zhou | + 2 word(s) | 2600 | 2021-09-29 08:22:48 | | |

Video Upload Options

We provide professional Academic Video Service to translate complex research into visually appealing presentations. Would you like to try it?

Cite

If you have any further questions, please contact Encyclopedia Editorial Office.

Van Der Poll, H. Green Goldmining. Encyclopedia. Available online: https://encyclopedia.pub/entry/14713 (accessed on 09 August 2026).

Van Der Poll H. Green Goldmining. Encyclopedia. Available at: https://encyclopedia.pub/entry/14713. Accessed August 09, 2026.

Van Der Poll, Huibrecht. "Green Goldmining" Encyclopedia, https://encyclopedia.pub/entry/14713 (accessed August 09, 2026).

Van Der Poll, H. (2021, September 29). Green Goldmining. In Encyclopedia. https://encyclopedia.pub/entry/14713

Van Der Poll, Huibrecht. "Green Goldmining." Encyclopedia. Web. 29 September, 2021.

Copy Citation

Green goldmining was proposed since goldmining has brought about hardship in local communities through pollution of water and air; lost grazing and agricultural land; the creation of unprotected mining pits; exploitation and depletion of natural resources; as well as forced eviction and relocation of communities without fair compensation. Environmental management accounting practices are suggested to facilitate greener goldmining processes.

activity-based costing (ABC)

environmental management accounting (EMA)

environmental management accounting practices (EMAPS)

green goldmining

life cycle costing (LCC)

material flow cost accounting (MFCA)

sustainability

1. Introduction

According to the Chamber of Mines Report, Zimbabwe, being a goldmining country, produced an average of 27 tonnes of gold per annum at its peak in 1999. Although opportunities for expansion do exist, lately production averages 15 tonnes per annum [1]. In Zimbabwe, the mining sector is a major driver of foreign direct investment (FDI) [2]. Despite the positive contribution of the mining sector to economic development, the sector has also brought about hardship in local communities through pollution of water and air; lost grazing and agricultural land; the creation of unprotected mining pits; exploitation and depletion of natural resources; as well as forced eviction and relocation of communities without fair compensation [2][3].

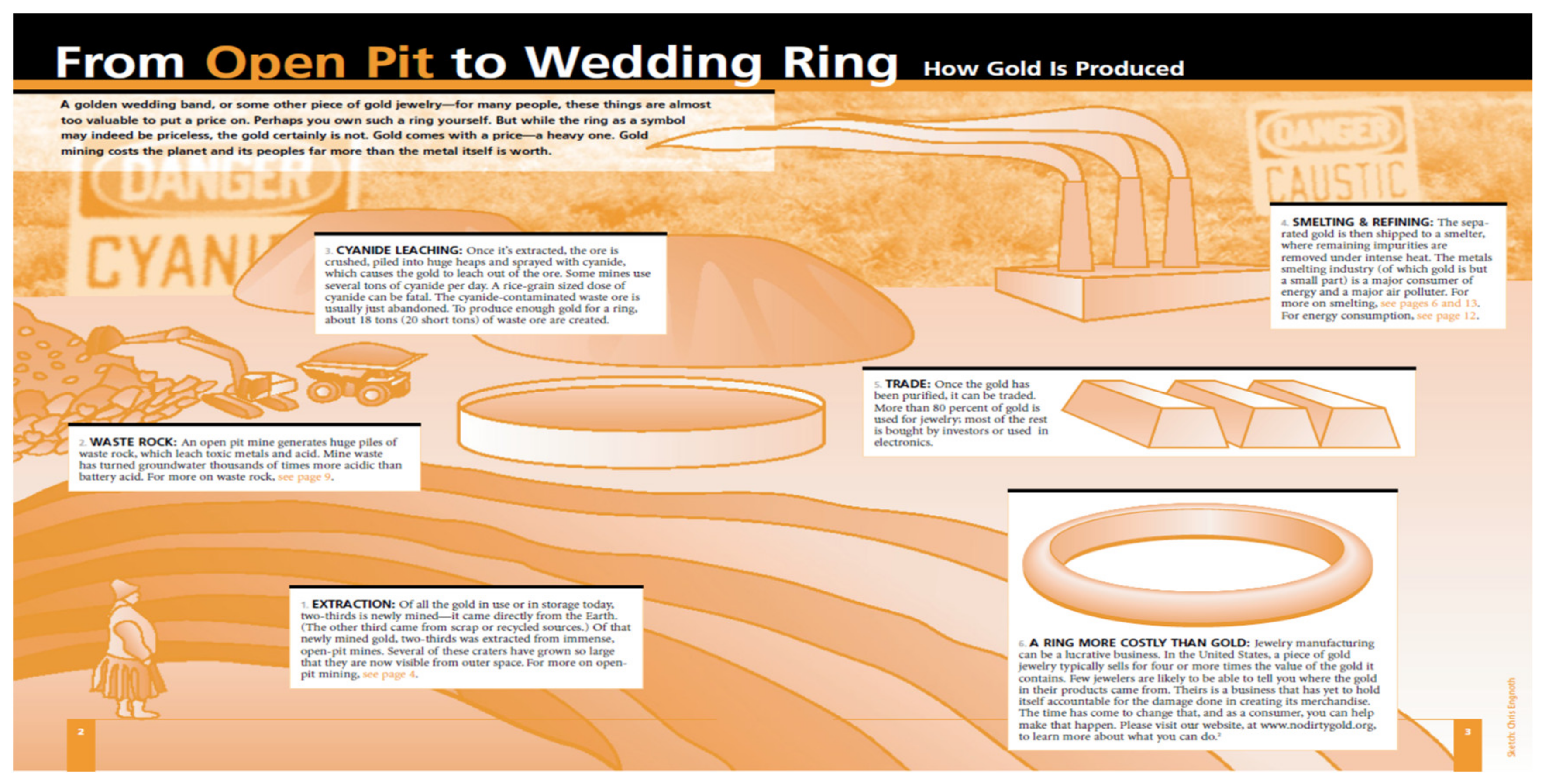

The impact of goldmining is not confined to Zimbabwe as a developing economy but is of global concern. Ref. [4] explains, in Figure 1, how gold is produced, and how the processes from the open pit to a piece of jewellery have an impact on the environment and host communities. To produce gold costs the environment much more than what a golden ring, for instance, is worth.

Figure 1. How gold is produced [4] (https://www.earthworks.org/ - reproduced with permission).

Following Figure 1, extraction from open pit mines leaves craters large enough to be visible from space. The second process entails waste rock, containing toxic metals which turn water to be more acidic than battery acid. Cyanide leaching occurs when the ore is sprayed with cyanide to release the gold from the rock. During the next phase, gold is heated to be smelted at high temperatures, and refined through a process using substantial amounts of energy. Once a piece of jewellery is made, it is sold at almost four times the cost of production, and this may lead to the jewellery industry being just as responsible for a negative environmental footprint [4]. This is where LCC (Section 2.4.2) may also play an important role to elicit these effects.

An area that needs to be further researched in surface goldmining, as is practised in Zimbabwe, is how it impacts local livelihoods. Conflicts regarding the use of land escalate to conflicts at a local, national, and ultimately a global level, with surface goldmining being one of the main sources of conflict. Western Ghana was identified as one of the leading goldmining regions, and a study by [5] assessed the land cover due to gold surface mining. They reported deforestation (58%), a substantial loss of farmland (45%), and relocation of farmers who then expand farmland into forests, as concerns. It is clear, therefore, that the effects of goldmining on the natural environment expands to the African continent, and not only Zimbabwe.

Owing to the population growth and humanity’s growing need for fuel, freshwater, fibres, and lumber, natural resources are consumed faster and more extensively during past decades, hence our natural habitat is over-exploited [6]. Consequently, ref. [6] argues for the transition towards green growth as a key to sustainable development and prosperity. Sustainability which is based on proactive decision making and innovation minimises the negative impact and maintains balance between environmental management, economic growth, political justice, and cultural aspects to work towards a desirable planet for all species [7]. The United Nations Environmental Programme [8] provides that when these pillars are integrated into a green economy framework; decision makers would be able to define policies based on a more complete picture. The major challenge in corporate sustainability is the development of a management framework to systematically follow the integration of sustainability in business strategy [9]. Sustainability has become important for each organisation and human being when the Sustainable Development Goals (SDGs) were proposed in 2015. Goals of importance for the mining industry are: good health and well-being (3), clean water and sanitation (6), responsible consumption and production (12), and climate action (13) [10]. In the same vein, the African Union developed Agenda 2063: The Africa we want with the following goals: healthy and well-nourished citizens (3) and environmentally sustainable and climate resilient economies and communities (7) which are aligned to the SDGs mentioned before [11].

Figure 2 presents all the Sustainable Development Goals (SDGs) developed in 2015.

Figure 2. The Sustainable Development Goals [12] (reproduced with permission: The content of this publication has not been approved by the United Nations and does not reflect the views of the United Nations or its officials or Member States).

In the light of the importance of sustainability based on the SDGs and Agenda 2063, it is apparent that the goldmining industry also need to decrease their environmental footprint. In adherence, the World Gold Council reported in 2019 that they launched the Responsible Gold Mining Principles (RGMPs) to ensure all stakeholders are aware how responsible goldmining is defined [13]. In this research, we propose that the goldmining sector incorporate environmental management accounting (EMA) into their operations. EMA has different practices to measure the flow of material (physical units) as well as money (monetary units). These are called environmental management accounting practices (EMAPs) which include, amongst others, activity-based costing (ABC), Life Cycle Costing (LCC), and material flow cost accounting (MFCA) [14]. These practices may enable the goldmining industry to identify and decrease waste and, at the same time, decrease costs, thereby increasing their profitability.

2. Literature about Green Goldmining

2.1. Environmental Impacts

Ref. [15] did a study in Zimbabwe on abandoned goldmines, regarding the surrounding soil of a tailings dam, and found that a low pH (acidity), electrical conductivity, potentially toxic elements (PTEs), and sulphate in the soil holds a threat to communities and the environment. To safeguard the environmental integrity and public health, they suggest stricter legislation, environmental stewardship, and environmental impact assessments. Their findings support our propositions Cp1 and Cp4 above.

Mineral production has a direct economic impact on surrounding communities, leading to poor health and wellbeing of local residents [16][17], and [18] argues that mineral development has severe negative social and economic impacts on multiple scales, ranging from local to global measurements. Industrial accidents, violation of human rights, health and safety issues, environmental degradation, and impact on livelihood of local communities are examples of some of the extreme negative social and environmental impacts of the mining sector [19], plausibly, therefore, goldmining in developing economies as well, leading to the cognition that goldmining activities have adverse effects on the natural environment, as they leave a strong footprint on the environment, arguably more than any other industrial activity.

Mining operations have a finite lifespan, hence humanity’s dependence on non-renewable resources cannot continue indefinitely [20]. Environmental impacts caused by mining range from destruction of habitat including fauna and flora; land disturbance which includes change of land use and land forms; natural watersheds and drainage patterns; adverse chemical impacts of improperly treated wastes, which include air pollution, waste dumps, and effluents, for example acid mine drainage (AMD); and noise and vibration due to blasting [21]. Hence, noise and dust pollution generated during the excavation process would affect surrounding plants and animals [22]. Ref. [23] concurs that mining can destroy the ecosystems, thereby resulting in the loss of the service values of the surrounding ecosystem. If not carefully managed, goldmining activities may destroy the environment, as their activities have an influence on adjacent ecosystem services, plausibly more for a developing economy, which may lack the resources to put remedial measures in place.

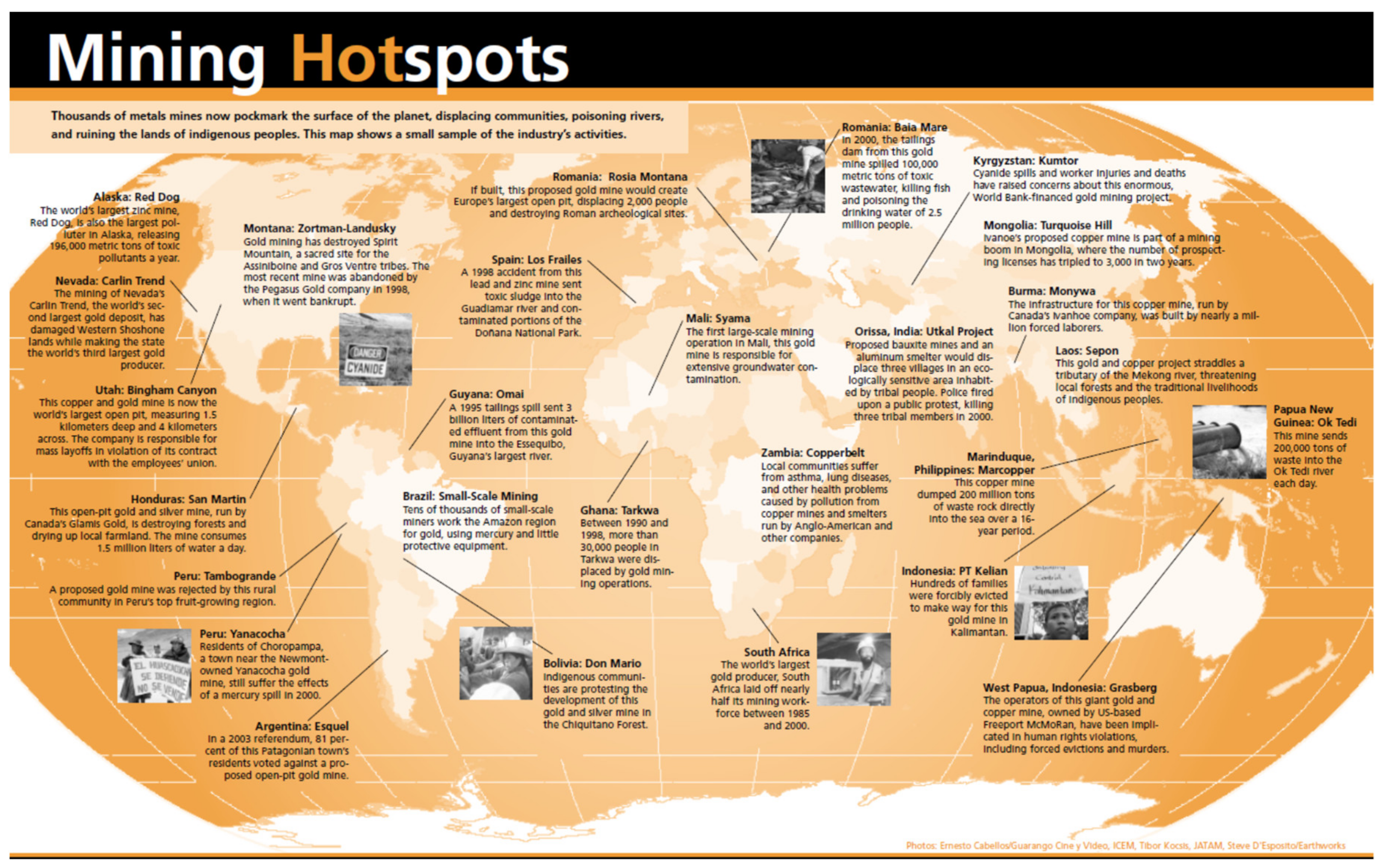

Figure 3 indicates global mining hotspots and their impact on the environment, as well as communities.

Figure 3. Mining hotspots and their impact [4] (https://www.earthworks.org/ - reproduced with permission).

2.2. Economic Impacts

Local livelihoods rarely profit sufficiently from mining activities, as mining has widespread and invasive environmental and social effects on these communities [24]. Ref. [25] advocates that the mining industry, owing to their environmental impacts, does not necessarily have direct links to the growth of the local economy, hence it does not contribute fully to the diversified sustainable development of a local, developing economy. It may, however, be a dominant industry in terms of providing for employment and generating income.

2.3. Impact on Society

Mineral extracting industries often cause conflicts between goals of the mining venture, the needs of the host community, and government policies [26]. Specifically, governments of developing countries have been observed to lacking the political will to effectively address the impacts of mining, for example, social injustice and inequality [27], leading to our next content proposition:

-

To be granted a social license to operate (SLO), goldmining organisations should consider the societal needs of communities in which they operate.

We furthermore observe our second association proposition:

-

There is an association between meeting objectives/goals of a mining company and expected results with respect to cost savings and minimising environmental impacts.

In most cases, mining development has been observed to cause an influx in the population, with employees from outside of the region moving closer to work [28], leading to an increase in demand for accommodation, resulting in an increase in rentals in communities with insufficient housing supply [29], in turn causing an increase in property prices. The population influx has been observed to further result in an increased cost of living [28] and to cause displacement from local towns of the most vulnerable groups in society [29], as well as exerting financial and societal pressures on local residents, which has been linked to psychological and health problems [30]. Therefore, if not carefully managed via a framework or guidelines to address the conflicts between the mining company and the surrounding community, goldmining activities can adversely impact communities with respect to housing, financial aspects, and health problems.

The neglect of the welfare of people in host communities in the mining regions has been attributed to the lack of defensive measurement of the impacts of mining on host communities [18]. Ref. [31] reports that goldmining activities taking place underneath the town in Zaruma, Ecuador, resulted in an elementary school being swallowed by a collapse in the ground just before Christmas 2016.

The observations in this section lead to a general proposition that holds in most walks of life:

-

Communication and engagement are essential among stakeholders to create common vision.

The foregoing discussion in (this) Section 2.3 provide an answer to our first research question, namely: What are the effects of mining operations on the environment? (RQ1). The rest of the research questions are addressed in the sections that follow in the solutions proposed in this article, namely, the use of EMA and its subsidiaries as core aspects of the proposed framework.

Next, we move to the tools of this article, namely, a discussion of environmental management accountings and its underlying sub tools.

2.4. Environmental Management Accounting (EMA)

The traditional way environmental-related costs have been accounted for indicates there has been little effort to reduce such costs, even though these costs could have been reduced if appropriate information had been provided for these [32]. According to ref. [33] and ref. [32] if, for example, material waste is included as part of total raw material costs and not as waste, opportunities to reduce waste might go amiss owing to a lack of information about the presence of waste. Environmental-related costs became increasingly essential to improve on waste management [34], and as a result a number of accounting methodologies such as EMA, carbon management accounting (CMA), and greenhouse-gas accounting (GHGA) have been developed [35]. Traditional methods that were in use did not consider environmental protection costs as well as integrated technologies [36][37], hence a more structured approach to costing environmental impacts had to be developed [38]. EMA therefore, encompasses a wide range of accounting tools given the diversity of management decisions [39], leading to:

-

Goldmining systems should have a management accounting system that determines wasteful activities and enhances cost optimisation.

Proposition Cp10 is a complementary proposition as it supports many other propositions in this article.

Ref. [40] defines EMA as a generic term that includes both monetary and physical EMA. Monetary environmental management accounting (MEMA) addresses environmental aspects of organisational activities expressed in monetary terms [40]. It provides the basis for most internal management decisions as it addresses aspects about tracing and treating costs and revenues incurred resulting from the company’s impact on the environment [41]. Physical environmental management accounting (PEMA) focuses on an organisation’s impact on the natural environment expressed in physical units [40]. Environmental measurement aspects and information are becoming vital, as stakeholders now pay increased attention to environmental performance [42]. Therefore, techniques that accurately measure environmental aspects should be used by organisations [43], and consequently a growing interest in accounting for the environment was sparked [44]. EMA as a response to environmental challenges can play an essential role in fostering an integrated approach to environmental management [45], hence the following content propositions:

-

EMA may hold much promise to be employed to manage the various challenges facing the goldmining sector;

-

EMA divisions of PEMA and MEMA, together with carbon management accounting (CMA) and greenhouse-gas accounting (GHGA), may provide essential information for the sustainable management of the challenges facing goldmining.

Ref. [46] promotes EMA as the most developed subset of sustainability accounting which, therefore, generates physical as well as monetary data through the use of various accounting techniques or methods. Material flow cost accounting (MFCA), life cycle costing (LCC) and activity-based costing (ABC) are methods to cost environmental impacts [38]. Therefore, this research aims to contribute to this body of knowledge by defining an integrated conceptual framework embedding MFCA, LCC, and ABC.

3. Conclusions

The literature revealed that, although the goldmining sector is a major driver of FDI, particularly for developing economies, it is also a major threat to environmental sustainability. Key environmental challenges noted include waste generation; water and air pollution; creation of unprotected pits; exploitation and depletion of natural resources; loss of fertile soils for farming; destruction of the ecosystems; and violation of human rights.

It was further noted that the drivers of environmental management can be grouped into internal forces (such as managerial level, leadership values, and organisational context) and external forces (such as regulation and competitive forces). Existing frameworks have been noted in lacking common ground that reconcile the major segments of sustainability development. We elucidated that an integrated conceptual framework to facilitate greener goldmining should, therefore, be developed within the context of EMA. Analyses of EMA revealed that this can be divided into two (2) aspects: Monetary environmental management accounting (MEMA) and Physical environmental management accounting (PEMA). EMA has been observed from the literature review to have come as a response to environmental challenges and is essential in fostering an integrated approach.

The discussion of EMAPs established that MFCA can be used in addressing material wastage and supporting eco-efficient decisions. LCC can be used in gauging the complete cost of waste management over the complete life cycle of a mining project. Further, ABC can be used in providing accurate environmental cost assignment to the mining sector, besides revealing where value is being added and where it is being lost. It was further noted that EMA plays an essential role in fostering an integrated approach of environmental management and carbon management accounting (CMA), greenhouse gas accounting (GHGA), MFCA, LCC, and ABC were identified as EMA variants and EMAPs.

We observed that sustainability could be improved using integrated management accounting systems that would integrate economic and social resources, supporting the view that the aforementioned methods should be combined to measure environmental costs more accurately. Whilst the adoption of EMA was noted to be voluntary and motivated by social structural inspirations and institutional theory in other countries, its adoption in Zimbabwe was observed to be a result of the need to comply to regulations and pressures from law enforcement agents [47].

References

- About Zimbabwe. Available online: http://metcorp.co.uk/about-us/about-zimbabwe.aspx (accessed on 20 June 2020).

- Murombo, T. Regulating mining in South Africa and Zimbabwe: Communities, the environment and perpetual exploitation. Law Environ. Dev. J. 2013, 9, 1–49.

- Dhliwayo, M. Public interest litigation as an empowerment tool: The case of the Chiadzwa community development trust and diamond mining in Zimbabwe. In Legal Tools for Citizen Empowerment Publication; IIED: London, UK, 2013; pp. 1–13.

- Earthworks; Oxfam America. Dirty Metals: Mining Communities and the Environment. Available online: https://www.earthworks.org/ (accessed on 18 August 2021).

- Schueler, V.; Kuemmerle, T.; Schröder, H. Impacts of surface gold mining on land use systems in western Ghana. Ambio 2011, 40, 528–539.

- Eze, C.C.; Chikezie, C.; Ibeagwa, O.; Ejike, R. Indigenous perspective and green economy: The pathway to sustainable indigenous perspective and green economy. Int. J. Agric. Innov. Res. 2015, 3, 1119–1123.

- Magee, L.; Scerri, A.; James, P.; Thom, J.A.; Padgham, L.; Hickmott, S.; Deng, H.; Cahill, F.; Magee, L.; Scerri, Á.A.; et al. Reframing social sustainability reporting: Towards an engaged approach. Environ. Dev. Sustain. 2013, 15, 225–243.

- United Nations Environment Programme (UNEP). Environment for the Future We Want; UNEP: Nairobi, Kenya, 2012; Volume 24.

- Gond, J.-P.; Grubnic, S.; Herzig, C.; Moon, J. Configuring management control systems: Theorizing the integration of strategy and sustainability. Manag. Account. Res. 2012, 23, 205–223.

- United Nations Development Programme. Sustainable Development Goals; UNDP: New York, NY, USA, 2015; p. 283.

- African Union. Agenda 2063: The Africa We Want; African Union: Addis Abeba, Ethiopia, 2015.

- United Nations. Sustainable Development Goals Kick Off with Start of New Year. Available online: https://www.un.org/sustainabledevelopment/blog/2015/12/sustainable-development-goals-kick-off-with-start-of-new-year/ (accessed on 18 August 2021).

- World Gold Council. Responsible Gold Mining. Available online: https://www.gold.org/about-gold/gold-supply/responsible-gold (accessed on 18 August 2021).

- United Nations. Environmental Management Accounting Procedures and Principles; UN: New York, NY, USA, 2001.

- Kanda, A.; Ncube, F.; Gadaga, T.; Dudu, V.P.; Makumbe, P.; Nyamadzawo, G. Contamination of soil around an abandoned gold mine tailings dam with trace elements in a small town, Northeastern Zimbabwe. Int. J. Glob. Environ. Issues 2019, 18, 283–302.

- Mactaggart, F.; McDermott, L.; Tynan, A.; Gericke, C. Systematic review examining health and well-being outcomes associated with mining activity in rural communities of high-income countries: A systematic review. Aust. J. Rural Health 2016, 24, 230–237.

- Smith, N.M. “Our gold is dirty, but we want to improve”: Challenges to addressing mercury use in artisanal and small-scale gold mining in Peru. J. Clean. Prod. 2019, 222, 646–654.

- Li, Q.; Stoeckl, N.; King, D.; Gyuris, E. Exploring the impacts of coal mining on host communities in Shanxi, China—Using subjective data. Resour. Policy 2017, 53, 125–134.

- Mutti, D.; Yakovleva, N.; Vasquez-Brust, D.; di Marco, M.H. Corporate social responsibility in the mining industry: Perspectives from stakeholder groups in Argentina. Resour. Policy 2012, 37, 212–222.

- Korolev, V.G. The development of countering monopolization in the electric energy industry. J. Environ. Account. Manag. 2020, 8, 311–322.

- Sahu, H.B.; Prakash, N.; Jayanthu, S. Underground mining for meeting environmental concerns—A strategic approach for sustainable mining in future. Procedia Earth Planet. Sci. 2015, 11, 232–241.

- Chukwuma, C. Environmental impact assessment, land degradation and remediation in Nigeria: Current problems and implications for future global change in agricultural and mining areas. Int. J. Sustain. Dev. World Ecol. 2011, 18, 36–41.

- Qian, W.; Burritt, R.L.; Monroe, G.S. Environmental management accounting in local government: Functional and institutional imperatives. Financ. Account. Manag. 2018, 34, 148–165.

- Kumah, A. Sustainability and gold mining in the developing world. J. Clean. Prod. 2006, 14, 315–323.

- Ivanova, G. The mining industry in Queensland, Australia: Some regional development issues. Resour. Policy 2014, 39, 101–114.

- Li, Z.; Nieto, A.; Zhao, Y.; Cao, Z.; Zhao, H. Assessment tools, prevailing issues and policy implications of mining community sustainability in China. Int. J. Min. Reclam. Environ. 2012, 26, 148–162.

- Morrice, E.; Colagiuri, R. Coal mining, social injustice and health: A universal conflict of power and priorities. Health Place 2013, 19, 74–79.

- Hresc, J.; Riley, E.; Harris, P. Mining project’s economic impact on local communities, as a social determinant of health: A documentary analysis of environmental impact statements. Environ. Impact Assess. Rev. 2018, 72, 64–70.

- Haslam Mckenzie, F.M.; Rowley, S. Housing market failure in a booming economy. Hous. Stud. 2013, 28, 373–388.

- Hossain, D.; Gorman, D.; Chapelle, B.; Mann, W.; Saal, R.; Penton, G. Impact of the mining industry on the mental health of landholders and rural communities in southwest Queensland. Australas. Psychiatry 2013, 21, 32–37.

- Frækaland Vangsnes, G. The meanings of mining: A perspective on the regulation of artisanal and small-scale gold mining in southern Ecuador. Extr. Ind. Soc. 2018, 5, 317–326.

- Deegan, C. Environmental costing in capital investment decisions: Electricity distributors and the choice of power poles. Aust. Account. Rev. 2008, 18, 1–15.

- Gale, R. Environmental management accounting as a reflexive modernization strategy in cleaner production. J. Clean. Prod. 2006, 14, 1228–1236.

- Tsai, W.; Chen, H.; Liu, J.; Chen, S. Using activity-based costing to evaluate capital investments for green manufacturing systems. Int. J. Prod. Res. ISSN 2011, 49, 7275–7292.

- Tsai, W.H.; Shen, Y.S.; Lee, P.L.; Chen, H.C.; Kuo, L.; Huang, C.C. Integrating information about the cost of carbon through activity-based costing. J. Clean. Prod. 2012, 36, 102–111.

- Jasch, C. The use of Environmental Management Accounting (EMA) for identifying environmental costs. J. Clean. Prod. 2003, 11, 667–676.

- Schaltegger, S.; Wagner, M. Current trends in environmental cost accounting—And its interaction with ecoefficiency performance measurement and indicators. In Implementing Environmental Management Accounting: Status and Challenges; Rikhardsson, P.M., Bennett, M., Bouma, J.J., Schaltegger, S., Eds.; Springer: Dordrecht, The Netherlands, 2005; p. 374.

- Du Plessis, A.; Oberholzer, M. A Framework for measuring and internal reporting of environmental costs at a mine. Environ. Econ. 2014, 5, 53–62.

- Christ, K.L.; Burritt, R.L. Material flow cost accounting: A review and agenda for future research. J. Clean. Prod. 2015, 108, 1378–1389.

- Burritt, R.L.; Hahn, T.; Schaltegger, S. Towards a comprehensive framework for environmental management accounting—Links between business actors and environmental management accounting tools. Aust. Account. Rev. 2002, 12, 39–50.

- Burritt, R.L.; Herzig, C.; Schaltegger, S.; Viere, T. Diffusion of Environmental Management Accounting for Cleaner Production: Evidence from Some Case Studies. J. Clean. Prod. 2019, 224, 479–491.

- Schaltegger, S.; Burritt, R. Contemporary Environmental Accounting: Issues, Concepts and Practice; Routledge: London, UK, 2000.

- Sroufe, R.; Montabon, F.L.; Narasimhan, R.; Wang, X. Environmental management practices: A framework. Greener Manag. Int. 2002, 40, 23–44.

- Ilinitch, A.Y.; Soderstrom, N.S.; Thomas, T.E. Measuring corporate environmental performance. J. Account. Public Policy 1998, 17, 383–408.

- Gunarathne, A.D.N. Fostering the adoption of environmental management with the help of accounting: An integrated framework. In Social Audit Regulation; Springer International Publishing: Cham, Switzerland, 2015.

- Burnett, R.D.; Hansen, D.R. Ecoefficiency: Defining a role for environmental cost management. Account. Organ. Soc. 2008, 33, 551–581.

- Mbedzi, M.D.; van der Poll, H.M.; van der Poll, J.A. An information framework for facilitating cost saving of environmental impacts in the coal mining industry in south Africa. Sustainability 2018, 10, 1690.

More

Information

Subjects:

Others; Others; Environmental Studies

Contributor

MDPI registered users' name will be linked to their SciProfiles pages. To register with us, please refer to https://encyclopedia.pub/register

:

View Times:

1.2K

Entry Collection:

Environmental Sciences

Revisions:

2 times

(View History)

Update Date:

29 Sep 2021

Table of Contents

Notice

You are not a member of the advisory board for this topic. If you want to update advisory board member profile, please contact office@encyclopedia.pub.

OK

Confirm

Only members of the Encyclopedia advisory board for this topic are allowed to note entries. Would you like to become an advisory board member of the Encyclopedia?

Yes

No

${ textCharacter }/${ maxCharacter }

Submit

Cancel

Back

Comments

${ item }

|

${ item.createdUser.fullName }

${ item.createdAt }

${ item.vote }

${ item.reply }

Delete

${ reply.createdUser.fullName }

${ reply.createdAt }

${ reply.vote }

Delete

There is no reply to this comment~

${ item.replyTextCharacter }/${ item.replyMaxCharacter }

Submit

Cancel

More

No more~

There is no comment~

${ textCharacter }/${ maxCharacter }

Submit

Cancel

${ selectedItem.replyTextCharacter }/${ selectedItem.replyMaxCharacter }

Submit

Cancel

Confirm

Are you sure to Delete?

Yes

No