Your browser does not fully support modern features. Please upgrade for a smoother experience.

Please note this is an old version of this entry, which may differ significantly from the current revision.

The fourth industrial revolution (4IR) emerged as a major issue at the 2016 World Economic Forum in Davos. Countries are trying to implement various policies from a preemptive point of view to respond to the fourth industrial revolution. Especially, the construction industry is also going through huge technological innovations, affected by 4IR. And technological innovation leads to improvements in various project outcomes and is a key factor that greatly affects the development of the construction industry.

- smart technology

- industrial competitiveness

- diffusion of innovation

- digitization

- construction industry

- contract

1. Introduction

1.1. Fourth Industrial Revolution and Construction Industry

The fourth industrial revolution (4IR) emerged as a major issue at the 2016 World Economic Forum in Davos. Countries are trying to implementing various policies from a preemptive point of view to respond to the fourth industrial revolution. In the UK, the “Construction 2025” strategy aims to reduce construction period by 50% through research and development in digital design, cutting-edge materials, and innovation in new technologies, reducing carbon emissions by 50% and reducing overall cost and life-cycle costs by 33% [1]. The German government announced its “Industry 4.0” strategy and selected nine key technologies, such as big data, self-aware robots, and simulations, as future drivers for its manufacturing industry and is pushing ahead with its evolutionary strategy [2]. The Japanese government is pushing for “I-Construction” to cope with the productivity degradation caused by the expected manpower shortage of the construction industry in the future. This is a policy that utilizes new technologies such as ICT throughout the production process and aims to improve the productivity of the construction industry by 2025 [3]. The Chinese government has announced its “China Manufacturing 2025” strategy, which focuses on 10 key areas such as IT technology, digital control, and robots through innovation, quality, and green development [4]. These policy trends are considered as a center of the key strategy for national industry development in the future.

The construction industry is also going through huge technological innovations, affected by 4IR. The construction industry generally has been considered as stuck with labor-centered construction, low-tech images, low productivity, and poor quality [5,6,7,8,9]. In addition, this industry tends to adapt slowly to new technologies and has conditions where it is difficult for innovation to take place [10,11]. This is a unique characteristic of the construction industry, and the challenge of innovation is applying the technology used in other industries to the construction industry [12,13]. Meanwhile, 4IR is able to create an opportunity for the construction industry to bring a much higher efficiency than ever before in terms of productivity, the business model, and the value chain. This opportunity is possible, via a convergence between existing technologies and emerging technologies from 4IR, and this change is called Construction 4.0 [13,14,15]. In the 4IR trend, Construction 4.0 represents a change in the construction industry, ranging from automated construction in the construction phase to high-level digitization by connecting virtual space and real construction projects [14,15]. The innovative technologies arising from the transition to Construction 4.0 are also called smart technologies [12,16], which improve the productivity, safety, and quality of the construction project [11,17,18,19,20]. Therefore, technological innovation leads to improvements in various project outcomes and is a key factor that greatly affects the development of the construction industry [21,22].

1.2. Necessity of Industry Competitiveness

Smart technology located in the center of technological innovation can change the paradigm of productivity in the construction industry, so construction firms are trying to utilize smart technology. In order to expand smart technology into the construction industry as a whole, the various factors of the industry must be corresponding with the acceptance condition of technology. The construction industry as public contracting work is more sensitive to government policy than other industries. The economic stimulation policies based on the construction industry have led to an increase in the volume and budget of construction projects, which affects the economic stimulus in the construction market and the impact of related industries. In addition, there are various stakeholders that comprise the construction industry. In particular, smart technology has unique characteristics in which the source technology of various industries is applied to construction technology in the project phases [15,23]. Source technologies such as sensors, drones, IoTs, and robots are developed in the electronics, telecommunications, and machinery industries, but these technologies are used in various ways in the construction industry for aircraft surveys, as safety sensors, and in robotics construction. Moreover, since the performance of the project is affected by various structured aspects such as systems, contracts, regulations, etc., institutional perspectives should also be considered for technical innovation in the construction industry [24,25,26,27]. As set out in the above, an industrial approach needs to consider a wide range of aspects, from the introduction of smart technology by companies to government policies.

2. The Diffusion of Innovation

In order to consider the industrial competitiveness, the current status of a country regarding the acceptance of innovation needs to be understood. This is because industrial competitiveness changes dynamically due to the country’s efforts for improving competitive [28]. In this regard, the national background for technology innovation needs to be understood about the innovation diffusion of users in the construction industry as well as the country’s policy activities. In other words, experts dealing with technology have to be considered as innovation adopters and national policies relating to smart technology have to be reviewed in detail.

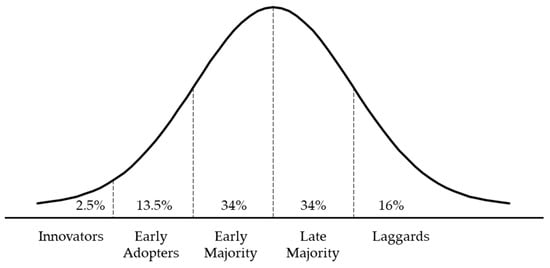

The diffusion of innovation theory (DIT) describes the process of accepting and adopting innovation, regarding the innovation of novelty felt by the acceptor, and has been studied in a wide variety of fields [29,30,31,32,33]. Rogers first proposed the theory of diffusion of innovation in 1962, which has evolved into a five-step study of the property of innovation and an acceptor perspective on innovation [34]. In particular, the innovation-acceptance curve is able to classify innovation adopters and indicates the size of a group varies depending on the period since innovation was introduced. It is significant in that it has shifted primarily from a conceptual study of the property and diffusion process of innovation to an acceptor perspective that accepts innovation over time [34]. The innovation-acceptance curve is described in five stages over time from the perspective of the acceptor who accepts the innovation (Figure 1). First, innovators are aggressive in innovation, adventurous, and willing to actively embrace uncertainty. Second, early adopters form a decisive cluster of large groups as innovations spread, which has a significant impact on innovation as groups discuss prior to adoption. Third, the early majority refers to layers in which innovations are accepted and adopted before they spread and reach their average values. Fourth, the majority is cautious and passive, showing a tendency to adopt innovation after it reaches an average point. Fifth, non-innovators are very unlikely to adopt innovation because they are negative about it and tend to choose to be very secure. From the perspective of accepting innovation, the innovation-acceptance curve shows that sales of innovative products are distributed with a bell-shaped curve when an innovation is released to the market. This curve separates the process of settling in the market from the time when an innovative technology appears in the market, which makes it easy to understand the current state of the industry where innovative technology is being introduced. Therefore, this paper studies the current status of the introduction of smart technology in the KCI through the innovation-acceptance curve.

Figure 1. Adopter categorization on the basis of innovativeness.

3. Policy in Korean Construction Industry

The Korean government announced the “4th Industrial Revolution Response Strategy” in 2017 to respond to 4IR. Korea’s Ministry of Land, Infrastructure and Transport announced the “6th Construction Technology Promotion Framework Plan” at the end of 2017 to reflect the fourth industrial revolution and respond to government policy directions. Since then, with the announcement of the “Smart Construction Technology Roadmap” as a detailed action plan, for the basic plan, the KCI has begun to move toward smart technology in earnest (Table 1). This roadmap is in the early stages of introducing technologies that develop other technologies, and has been conducting pilot tests from 2020 while establishing short-term goals to establish a foundation for using smart technologies by 2025. It also aims to complete automation of the construction industry by 2030 from a long-term perspective.

Table 1. Smart technology policy in KCI.

| Smart Technology Policies | Governments | Date | Policy Goals |

|---|---|---|---|

| 4th Industrial Revolution Response Strategy [35] | A 1 | April 2017 | Four goals are presented, such as smart land, transportation service industry innovation, public infrastructure safety efficiency improvement, and innovation foundation. |

| 4th Industrial Revolution Response Plan I-KOREA [36] | B 2 | November 2017 | Challenges are promoted by securing technology for growth engines, creating industrial infrastructure/ecosystems, and responding to changes in future society. |

| 6th Construction Technology Promotion Framework Plan [37] | A | December 2017 | It will present “Smart Construction 2025”, which is applied by BIM and AI as its vision by 2025. |

| Construction Industry Innovation Plan [38] | A | June 2018 | Presentation of innovation measures on four themes, such as technology, production structure, market order, and jobs. |

| Smart Construction Technology Roadmap [39] | A | October 2018 | A roadmap is presented to specify the tasks implemented in the “6th Construction Technology Promotion Framework Plan”. |

| Construction Engineering Development Plan [40] | C 3 | September 2020 | Proposal of paradigm shift and smart-construction engineering promotion and development centered on high value-added construction engineering. |

1 A = the Ministry of Land, Infrastructure and Transport, 2 B = the 4th Industrial Revolution Committee, 3 C = joint government departments.

In order to understand the current status of smart technology spreading in the KCI, an interview with an expert was conducted on policies and the status of government policies. According to the interview, a few major firms were using smart technologies, but construction firms outside the top five in revenue were only aware of smart technologies. A common situation in the small number of major firms utilizing technology is that they are building independent teams to have smart-technology expertise, because they have expectations for business performance despite uncertainties related to the verification of smart technology. It started as a separate task-force team and operated within the firm as a project-support team. A common opinion of most construction firms is that they do not utilize smart technology, as they were collecting technical information by surveying the market situation from a risk-avoidance perspective, along with having doubts about the utility of smart technology. Although there is no separate smart-technology team, the management-support team has been collecting information or visiting sites utilizing technology.

Despite the government’s activation policy, the status of the KCI is one of restrictively using smart technology. A few major firms were organizing their own teams to spread technical information to project departments and to provide guidance on technology utilization, and they were exploring construction sites for finding smart-technology needs. However, most construction firms have observed, rather than actively accepted, smart technology and have avoided the potential risks of unfamiliar technology. Firms utilizing smart technologies were less than 1% of the whole number of construction firms, ones that could handle the potential risks, had formed a special organization within the firm, and had tried to use technologies on their construction sites. Thus, considering the circumstances of the policies and firms, KCI was considered as having a few innovators that led to smart-technology application in the early stages of technology introduction, which implies that it is important to be expanding smart technology to the construction industry as a whole.

4. Industry Competitiveness

The theory of industrial competitiveness was largely classified as a theory of national competitiveness, and various theories have emerged over time. In the 1930s, American economists developed the structural–conduct–performance (SCP) model to understand the causal relationship between the environment, behavior, and performance of a company, in an attempt to eliminate factors that hinder competition in the industry. Starting with this, research on competitiveness from an industry perspective has continued to develop [41]. Based on the SCP model, the most influential model presented as an analysis of the corporate perspective is the five-forces framework, developed by Michael Porter [42]. However, the model is limited in that it does not describe specific competitive strategies between companies, because it describes the industrial structure as a static analytic component of changes in industrial trends. Therefore, the proposed model to overcome these limitations is the diamond model [43].

The diamond model explains that a country’s competitiveness is due to environmental conditions, including the characteristics of the industry. These environmental conditions have Factor Condition, Demand Condition, Firm Strategy, Structure and Rivalry, and Related and Supporting Industry as endogenous variables, and Governance and Chance as exogenous variables [28]. For each factor, the endogenous and exogenous variables are divided as follows. Factor Condition represents everything in the human, technological, resource, and supply chain that is fundamental to production. It is divided into basic elements such as natural resources, workers, and advanced elements such as technology. Demand Condition refers to the presence of local and important consumers under market conditions that facilitate the continuous research on and development of products and businesses. In general, market size and demand can be viewed as related factors. Firm Strategy, Structure, and Rivalry derive the overall structure and strategy in which an enterprise is created, organized, and operated in a country, indicating the extent to which it can continue to gain a competitive advantage. Related and Supporting Industry indicates the presence of internationally competing related industries or support industries. These industries support target industries or competitiveness and make production activities work well. Government affects national competitiveness externally through the role of regulations on trade, industrial competition, etc., and Chance can be an unexpected opportunity for related industries through events such as war, climate change, and social events. Porter suggested that the diamond model consists of these endogenous and exogenous variables, which affect each other, and endogenous elements are influenced by exogenous variables.

The diamond model can effectively analyze the competitiveness of industries [44], and a lot of research applying this model has been conducted in various industries, including the construction industry [45,46,47,48,49,50,51]. As such, the model provides a good framework for analyzing the concept of competitiveness at the national level and provides directions for presenting elements that diagnose the competitiveness of the industry [47]. Therefore, this study intends to derive and analyze the industrial competitiveness of smart technology in the construction industry by utilizing the diamond model.

This entry is adapted from the peer-reviewed paper 10.3390/su14148348

This entry is offline, you can click here to edit this entry!