Your browser does not fully support modern features. Please upgrade for a smoother experience.

Please note this is a comparison between Version 2 by Nora Tang and Version 1 by Md Shahariar Chowdhury.

Electric vehicles (EVs) are considered to be a solution for sustainable transportation. EVs can reduce fossil fuel consumption, greenhouse gas emissions, and the negative impacts of climate change and global warming, as well as help improve air quality.

- electric vehicle

- EV

- financial

- performance

- infrastructure

1. Introduction

The transportation sector is a major contributor to emissions and air pollution in major cities. Transportation consumes approximately one quarter of the total global fossil fuel supply, and a large portion of this supply is consumed by road transport.

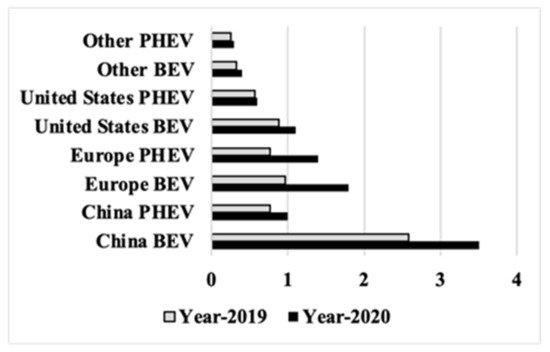

With more than 14% of total global emissions, the transportation industry is one of the major contributors to rising GHG emissions [1]. The 2020 International Energy Agency (IEA) report (Tracking Transport 2020) found that transportation is responsible for 24% of direct CO2 emissions from fuel combustion. The main problem is that emissions from this sector are projected to rise over time, up to 70% by 2050 based on a business-as-usual scenario [1]. In the 21st century, electric vehicles have captured the attention of the global automobile industry; according to recent research, three areas hit a 90% sales record in 2019 [2]: the USA, Europe, and China, which sold around 0.326 million, 0.56 million, and 1.06 million electric vehicles, respectively. In 2020, the global electric-car stock exceeded USD 10 million. The region-specific distribution is illustrated in Figure 1 for 2019 and 2020.

Figure 1. Global electric passenger car stock for 2019 and 2020. BEV: battery electric vehicles; PHEV: plug-in hybrid electric vehicles. Data source: IEA, Global EV Outlook 2021.

In 2019, annual global electric vehicle sales increased by 14%, accounting for 80% in Europe and 43% in Canada, with steady sales in China and the United States. Furthermore, EV adoption has globally increased, including in Norway (39.6%), Hong Kong (10.61%), the United States (3.32%), the United Kingdom (1.94%), and China (2.41%) [3,4][3][4]. EVs have various advantages, including fewer GHG emissions, safety, cost savings, and low maintenance, and offer a long-term solution to environmental concerns, as shown by their current acceptance rate and predicted improvement. Thus, EVs are an alternative to internal-combustion engine vehicles (ICEVs), and can provide sustainable transportation [5]. Electric vehicles have the potential to reduced reliance on fossil fuels. There are many varieties of EVs on the market, including hybrid electric vehicles (HEV) and plug-in electric cars.

Although EVs are environmentally friendly, they pose a number of problems for the distribution system, including increased system load due to PEV charging, which reduces substation reserve capacity and feeder load transfer capabilities, EV charging peaks, and traditional distribution loads. The European Union’s (EU) energy laws include a policy for distribution system operators (DSO); the rest of the world is yet to implement such a policy. Furthermore, inconstancy in electric vehicle operating patterns causes consumer preferences to change [6]. The impact of electric vehicle market integration on utility distribution load profiles has also received much attention. Charging an electric vehicle battery may use up to twice as much energy as that of a typical home. This would be quite the challenge to power system management when the adoption of EVs is more widespread [7]. Denmark pursued a project for electric vehicle battery storage in order to facilitate large-scale wind-power integration [8]. The vehicle-to-grid concept allows for EV owners to provide power from a battery to the grid during peak consumption. This concept could ensure grid reliability and flexibility.

In Thailand, the total final energy consumption in 2017 was 80,752 kton. The transport sector’s portion of this consumption constituted about 40.1% [9]. Road transportation activities in Thailand were estimated to be 77.05% of total transport activities. Registered vehicles in Thailand rose from 26.42 million in 2008 to 38.31 million in 2017 [10]. Key challenges of road transport in Thailand include the rapid growth of vehicles, which increases energy demand, thereby contributing to GHG emissions and air pollution as particulate matter (PM2.5). With regard to fuel consumption by fuel type, diesel constituted the highest with 43%, followed by gasoline, jet fuel, natural gas, liquefied petroleum gas (LPG) and fuel oil at 25%, 17%, 7%, 5%, and 3%, respectively. As alternatives, biodiesel, ethanol, natural gas, hydrogen, and electricity are used as fuel for vehicles [5].

The Thai government launched policies to promote EVs in 2015, which marked the beginning of EV policy in Thailand. However, the adoption of EVs is quite low, at 0.32% of the total number of registered vehicles (i.e., 123,967 EVs compared to 38.31 million cars registered with the Department of Land Transportation) [11].

Several EV policies have been launched for widespread EV adoption in the long run. The Energy Efficiency Plan (EEP2015) set a target of 1.2 million EVs by 2036 [12,13][12][13]. The National Science and Technology Development Agency (NSTDA) issued a plan for Thailand to be an ASEAN BEV hub, including the capacity to produce 1000 electric buses a year and develop prototype modified EVs [14]. In addition, the customs department and the Board of Investment of Thailand provided EV investments by creating tax incentives for investors, customs deductions for imported EVs, and EV parts and equipment [15]. Therefore, it is more interesting to investigate barriers to EV adoption than ICEVs, as it is essential to help develop innovative policy incentives and the wider adoption of EVs in Thailand.

Country-specific barrier and factor identification towards EV adoption can be found in the literature for countries such as in India [16,17][16][17] and Norway [18]. Although this may be true, a recent review compiled a list of countrywide EV-related scientific articles [19] and revealed that no study has been conducted for Thailand; this justifies the novelty of the present work. Therefore, this study investigated the factors that influence EV adoption in Thailand using an online questionnaire survey. Research questions included what the barriers to widespread adoption of EVs are, and whether these factors affect public acceptance of EVs.

2. Financial Barriers

High purchase cost, battery cost, the understanding of fuel and maintenance cost, and resale value are financial barriers to EV adoption. Compared with ICEVs, EVs have limited function [31][20]. As an emerging new technology, EVs are often expensive due to the lack of an economy of scale [29][21], and consumers must pay a much higher price than that of ICEVs; thus, the high purchase cost of EVs is a major barrier in many consumer surveys [20][22]. Battery cost is another barrier, and is a significant portion of EV cost [32][23]. Battery capacity increases with size, purchase cost, and range [33][24].

However, EVs have advantages in fuel and maintenance costs. The fuel cost of EVs comes from electricity, which is less expensive and produces fewer direct emissions compared to gasoline-fueled vehicles. EV maintenance cost is also less than that of ICEVs due to the reduced complexity of EV motors [15]. However, consumer purchasing decisions depend on several other factors besides technology and utility [32][23].

3. Vehicle Performance Barriers

EV performance barriers include range, engine power, reliability, battery lifespan, charging time, safety, size, and style. Numerous studies revealed that EV performance and range are major barriers to their adoption [23][25]. Drivers cannot estimate how far they could go or extend a journey on the basis of the remaining battery [33,34][24][26]. Therefore, battery depletion occurs while driving. The limited range of EVs is a concern to drivers and results in range anxiety during long journeys [30,35][27][28]. Other unsatisfying EV performance issues are charging time [31][20], safety, and reliability, which are raised by respondents who test-drive EVs. Consumers are also concerned about the limited EV sizes and styles on the market [32][23].

4. Infrastructure Barriers

Given that EV range is a major barrier to adoption, the availability of charging infrastructure is essential in order to support the wide adoption of EVs, as is the case with filling stations for ICEVs [29][21]. Public charging stations are important for EV demand and competition [36][29]. Overnight home charging is important to boost consumer convenience and the safety and security of vehicles [37][30].

Many studies in the literature have explored different barriers to global EV adoption. However, how all these barriers affect EV adoption in Thailand has not been addressed in the literature. Thus, this study analyzes all these barriers in the context of Thailand in order to close this research gap.

References

- Moeletsi, M.E. Socio-Economic Barriers to Adoption of Electric Vehicles in South Africa: Case Study of the Gauteng Province. World Electr. Veh. J. 2021, 12, 167.

- IEA. Electric Vehicles 2020c; IEA: Paris, France, 2021.

- Rietmann, N.; Lieven, T. How policy measures succeeded to promote electric mobility–Worldwide review and outlook. J. Clean. Prod. 2019, 206, 66–75.

- Patyal, V.S.; Kumar, R.; Kushwah, S. Modeling barriers to the adoption of electric vehicles: An Indian perspective. Energy 2021, 237, 121554.

- Swaraz, A.; Satter, M.A.; Rahman, M.M.; Asad, M.A.; Khan, I.; Amin, M.Z. Bioethanol production potential in Bangladesh from wild date palm (Phoenix sylvestris Roxb.): An experimental proof. Ind. Crops Prod. 2019, 139, 111507.

- Galiveeti, H.R.; Goswami, A.K.; Choudhury, N.B.D. Impact of plug-in electric vehicles and distributed generation on reliability of distribution systems. Eng. Sci. Technol. Int. J. 2018, 21, 50–59.

- Shalalfeh, L.; AlShalalfeh, A.; Alkaradsheh, K.; Alhamarneh, M.; Bashaireh, A. Electric Vehicles in Jordan: Challenges and Limitations. Sustainability 2021, 13, 3199.

- Pillai, J.R.; Bak-Jensen, B. Impacts of electric vehicle loads on power distribution systems. In Proceedings of the 2010 IEEE Vehicle Power and Propulsion Conference, Lille, France, 1–3 September 2010; pp. 1–6.

- Ministry of Energy. Thailand Energy Consumption Report 2017. 2018. Available online: http://www.eppo.go.th/index.php/en/en-energystatistics/electricity-statistic (accessed on 20 February 2021).

- Department of Land Transport. Department of Land Transportation. Total Vehicle Registration Data; 2018. Available online: http://www.dlt.go.th/minisite/m_upload/m_download/singburi/file_7cf81db11863f882ac1e6814fbb16c02.pdf (accessed on 20 February 2021).

- Kester, J.; Noel, L.; de Rubens, G.Z.; Sovacool, B.K. Policy mechanisms to accelerate electric vehicle adoption: A qualitative review from the Nordic region. Renew. Sustain. Energy Rev. 2018, 94, 719–731.

- Ministry of Energy. Energy Efficiency Plan 2015–2036 (EEP2015); National Energy Policy Council (NEPC): Bangkok, Thailand, 2015. Available online: http://energyefficiency.gov.np/uploads/21_ee_strategy__1449652787.pdf (accessed on 20 February 2021).

- Thananusak, T.; Punnakitikashem, P.; Tanthasith, S.; Kongarchapatara, B. The development of electric vehicle charging stations in Thailand: Policies, players, and key issues (2015–2020). World Electr. Veh. J. 2021, 12, 2.

- Energy Policy and Planning Office; Ministry of Energy. Project Prepare for Future Use of Electric Vehicles in Thailand. Available online: https://energy.go.th/2015/en/ (accessed on 20 February 2021).

- National Metal and Materials Technology Center (MTEC). Assessment of Electric Vehicle Technology Development and Its Implication in Thailand. Available online: https://www.mtec.or.th/en/ (accessed on 15 February 2021). (In Thai)

- Tarei, P.K.; Chand, P.; Gupta, H. Barriers to the adoption of electric vehicles: Evidence from India. J. Clean. Prod. 2021, 291, 125847.

- Dua, R.; Hardman, S.; Bhatt, Y.; Suneja, D. Enablers and disablers to plug-in electric vehicle adoption in India: Insights from a survey of experts. Energy Rep. 2021, 7, 3171–3188.

- Neaimeh, M.; Salisbury, S.D.; Hill, G.A.; Blythe, P.T.; Scoffield, D.R.; Francfort, J.E. Analysing the usage and evidencing the importance of fast chargers for the adoption of battery electric vehicles. Energy Policy 2017, 108, 474–486.

- Kumar, R.R.; Alok, K. Adoption of electric vehicle: A literature review and prospects for sustainability. J. Clean. Prod. 2020, 253, 119911.

- Weiss, M.; Patel, M.K.; Junginger, M.; Perujo, A.; Bonnel, P.; van Grootveld, G. On the electrification of road transport-Learning rates and price forecasts for hybrid-electric and battery-electric vehicles. Energy Policy 2012, 48, 374–393.

- Adner, R. When are technologies disruptive? A demand-based view of the emergence of competition. Strateg. Manag. J. 2002, 23, 667–688.

- Jabbari, P.; Chernicoff, W.; MacKenzie, D. Analysis of electric vehicle purchaser satisfaction and rejection reasons. Transp. Res. Rec. 2017, 2628, 110–119.

- Browne, D.; O’Mahony, M.; Caulfield, B. How should barriers to alternative fuels and vehicles be classified and potential policies to promote innovative technologies be evaluated? J. Clean. Prod. 2012, 35, 140–151.

- Bubeck, S.; Tomaschek, J.; Fahl, U. Perspectives of electric mobility: Total cost of ownership of electric vehicles in Germany. Transp. Policy 2016, 50, 63–77.

- Lim, M.K.; Mak, H.-Y.; Rong, Y. Toward mass adoption of electric vehicles: Impact of the range and resale anxieties. Manuf. Serv. Oper. Manag. 2015, 17, 101–119.

- Priessner, A.; Sposato, R.; Hampl, N. How to Trigger Mass-Market Adoption for Electric Vehicles?—An Analysis of Potential Electric Vehicle Drivers in Austria. Available online: https://www.eeg.tuwien.ac.at/conference/iaee2017/files/presentation/Pr_364_Priessner_Alfons.pdf (accessed on 15 February 2021).

- Illmann, U.; Kluge, J. Public charging infrastructure and the market diffusion of electric vehicles. Transp. Res. Part D Transp. Environ. 2020, 86, 102413.

- Liao, F.; Molin, E.; van Wee, B. Consumer preferences for electric vehicles: A literature review. Transp. Rev. 2017, 37, 252–275.

- Hardman, S.; Jenn, A.; Tal, G.; Axsen, J.; Beard, G.; Daina, N.; Figenbaum, E.; Jakobsson, N.; Jochem, P.; Kinnear, N. A review of consumer preferences of and interactions with electric vehicle charging infrastructure. Transp. Res. Part D Transp. Environ. 2018, 62, 508–523.

- Coffman, M.; Bernstein, P.; Wee, S. Electric vehicles revisited: A review of factors that affect adoption. Transp. Rev. 2017, 37, 79–93.

More