Your browser does not fully support modern features. Please upgrade for a smoother experience.

Submitted Successfully!

+1 credit

+1 credit

Thank you for your contribution! You can also upload a video entry or images related to this topic.

For video creation, please contact our Academic Video Service.

| Version | Summary | Created by | Modification | Content Size | Created at | Operation |

|---|---|---|---|---|---|---|

| 1 | Christos Kanellopoulos | -- | 2625 | 2024-02-22 13:00:53 | | | |

| 2 | Lindsay Dong | Meta information modification | 2625 | 2024-02-23 06:33:40 | | |

Video Upload Options

We provide professional Academic Video Service to translate complex research into visually appealing presentations. Would you like to try it?

Cite

If you have any further questions, please contact Encyclopedia Editorial Office.

Kanellopoulos, C.; Sboras, S.; Voudouris, P.; Soukis, K.; Moritz, R. Antimony as a Critical Raw Material. Encyclopedia. Available online: https://encyclopedia.pub/entry/55351 (accessed on 26 July 2026).

Kanellopoulos C, Sboras S, Voudouris P, Soukis K, Moritz R. Antimony as a Critical Raw Material. Encyclopedia. Available at: https://encyclopedia.pub/entry/55351. Accessed July 26, 2026.

Kanellopoulos, Christos, Sotiris Sboras, Panagiotis Voudouris, Konstantinos Soukis, Robert Moritz. "Antimony as a Critical Raw Material" Encyclopedia, https://encyclopedia.pub/entry/55351 (accessed July 26, 2026).

Kanellopoulos, C., Sboras, S., Voudouris, P., Soukis, K., & Moritz, R. (2024, February 22). Antimony as a Critical Raw Material. In Encyclopedia. https://encyclopedia.pub/entry/55351

Kanellopoulos, Christos, et al. "Antimony as a Critical Raw Material." Encyclopedia. Web. 22 February, 2024.

Copy Citation

Antimony is widely acknowledged as a critical raw material of worldwide significance, based on its recognition by many countries. According to current projections, there is an anticipated increase in the demand for antimony in the forthcoming years. An issue of significant concern within the supply chain, which poses a substantial obstacle to sustainable development, is the global unequal allocation of abundant antimony resources. Most nations exhibited a high degree of dependence on a few countries for their net imports of antimony, resulting in a notable disruption and raising concerns regarding the supply chain.

antimony (Sb)

stibnite

critical metal

1. Introduction

Antimony (Sb) is considered to be a critical raw material (CRM) of global significance, as acknowledged by multiple countries and unions, including the European Union [1], the United States of America [2], China [3], the United Kingdom [4], and Canada [5]. Antimony has been recognized as a CRM since its inclusion in the first European Union (EU) CRM report published by the European Commission in 2010 [6]. Despite this, the EU and many of the countries cited above do not extract antimony ores inside their territorial boundaries and are entirely dependent on imports.

Antimony has a strong affinity with sulfur; thereby, it is classified as a chalcophile element. Moreover, it is often seen to create chemical compounds with a range of metallic elements, leading to the formation of sulfosalts [7]. Although it is relatively uncommon in the Earth’s upper crust, with a concentration of 0.4 ppm [8], it exhibits similarities to certain other heavy rare-earth elements [9]. Antimony is often encountered in elevated concentrations at specific ore deposits. Antimony is widely acknowledged as a significant pathfinder element in the context of geochemical prospecting surveys, primarily owing to its strong association with various mineral occurrences [10].

Antimony has several applications in the industrial sector, such as in the realms of green energy and emerging technologies. The use of emerging technologies in developing high-capacity storage batteries highlights the significance of antimony as a CRM in facilitating the move toward sustainable development and energy transition [11]. The present projections for future antimony demand exhibit variability. Mordor Intelligence [12] predicts that the antimony market will have a yearly growth rate of 5% until 2026. Perpetua Resources [13] asserts that an extra annual production of 18 kt (equivalent to 12% of the 2018 production) will be necessary until the year 2030. Over 60% of the global supply originates from China, which can cause a significant supply disruptions and concern [11].

2. Global Perspective

2.1. World Resources, Production and Perspectives

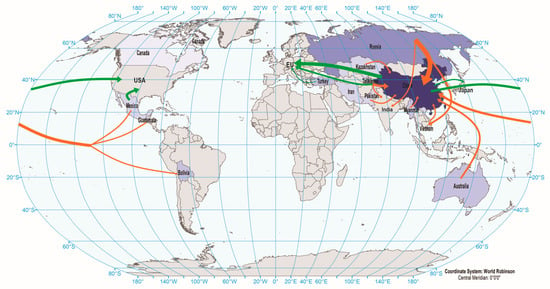

The distribution of antimony deposits is only located within a geographically restricted area. China and Russia, and their respective political and economic partners, have substantial influence over the worldwide antimony upstream supply chain (Figure 1 and Figure 2). According to the United States Geological Survey’s (USGS) estimate in 2021, these businesses jointly represent over 90% of the global mining production of antimony [13].

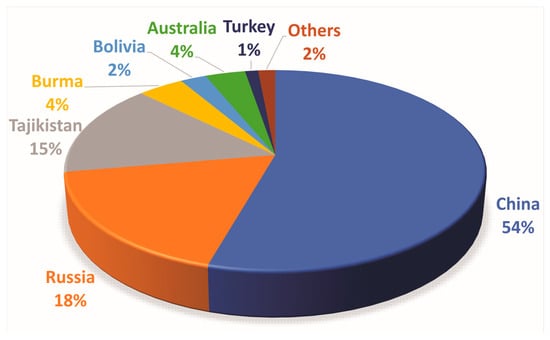

Figure 2. Distribution of Global Mine Production of Antimony (2022) (based on [15]).

In the year 2010, the Chinese government introduced two policies that led to a reduction in domestic antimony production, causing significant disruption in the markets. At the beginning of 2010, the Chinese government expressed its disinclination to provide authorization for any prospective antimony initiatives until the culmination of 30 June 2011. During a similar timeframe, the Chinese government enforced the shutdown of around 100 antimony smelters in its main antimony-producing region. The implementation of this action was carried out with the objective of ceasing unauthorized mining activities and minimizing the adverse effects on the environment [3][16].

Until 2021, China retained its status as the primary global producer of antimony, accounting for 55% of the total global mining production. Russia and Tajikistan also contributed, constituting 23% and 12% of the total, respectively [17]. In 2021, the global supply of antimony raw materials and the subsequent production of antimony products faced constraints as a result of environmental audits carried out in China and temporary mine closures implemented to mitigate the global transmission of the COVID-19 pandemic. The limited availability of raw materials, coupled with difficulties in worldwide transportation, led to a reduced supply of processed antimony in the market. As a result, there was a notable escalation in the price of antimony, reaching $6.65 per pound in October 2021, which marked a substantial rise compared to the average annual price of $2.67 per pound in 2020 [17].

Between 2012 and 2016, the European Union (EU) maintained a stable average importation of 22,200 tons per year of antimony metal and antimony oxides. China is the primary source of imports for the European Union, accounting for ca. 40% of the EU’s overall imports, with an annual import volume of 17,650 tons [18].

According to Laznicka [19][20] the global collection of 24 giant antimony deposits included a cumulative quantity of 6.97 million metric tons of antimony. According to Laznicka’s estimation, the overall world endowment of antimony is projected to range from 7.1 to 7.5 million metric tons [3]. The most significant reserves are located in China, Russia, Bolivia, Mexico, USA, South Africa, and Tajikistan. Approximately one-third of these deposits are found in China [3][21].

There are several known antimony resources which are mainly unevenly distributed over the planet. In the current market situation, there is a preference for exploiting only large deposits that are suitable for implementing high-volume bulk-mining techniques. The EU, the USA, and the other countries in the Western Hemisphere have antimony resources inside their territorial boundaries, but they are not ample resources [3]. For example, antimony resources are found in six European nations, i.e., France, Germany, Sweden, Finland, Slovakia, and Greece. An additional problem is that the majority of resources in Europe rely on historical estimations, and their economic significance at present is questionable [18].

The potential future mining of antimony resources is expected to mostly include either simple stibnite or precious metal deposits associated with copper, lead, and/or zinc. Also, gold is a significant co-product of antimony. However, it is often the primary focus of extraction in gold–antimony vein mining operations. The inclusion of antimony in gold ore poses challenges in terms of processing, leading to increased difficulty and cost. Consequently, it may be necessary to accumulate a quantity of gold ore with a significant antimony content [3][9]. In the future, the recovery of antimony from precious metal deposits might potentially serve as the most easily accessible source of antimony in the event of a sudden spike in demand [3].

In Greece, a member of the EU, the presence of antimony was identified in several locations and different geological settings, including cases of simple antimony deposits and cases of precious metal deposits. In some cases, antimony exploitation projects took place mainly in the first half of the last century. Proposing the feasibility of sustainable exploitation initiatives in the present day.

2.2. Antimony Uses, Substitution, Recycling and Environmental Considerations

Antimony is categorized as a metalloid due to its chemical characteristics. According to Miller [7], antimony demonstrates brittleness when used as an independent material. However, when integrated into alloys, it provides improved strength, hardness, and corrosion resistance. The material has a low level of thermal and electrical conductivity. The natural abundance of this metal is limited, owing to its strong affinity for sulfur and other metals, including lead, copper, and silver [22].

Antimony has played a significant role as an element of great importance throughout human history. As early as around 3100 B.C., stibnite (Sb2S3), the primary ore mineral for antimony, was employed by the ancient Egyptians and early Hindus to produce black eye makeup [3]. The initial application of antimony in the field of technology was primarily associated with the advancement of cast metal printing types, mirrors, bell metal, and pigments. During the 18th century, France, Germany, and Italy emerged as the primary nations engaged in antimony production. The greater utilization of storage batteries in automobiles throughout the 1930s led to a significant rise in the demand for antimony. During the 1940s, the demand for antimony experienced a significant increase due to its numerous military uses in World War II [7]. The global mining output saw substantial growth from 1900 to 2016, with a rise from 7710 metric tons to 186,000 metric tons [23].

Nowadays, antimony is predominantly utilized as a flame retardant and in lead–acid storage batteries designed for automotive applications. The batteries comprise a lead alloy containing around 4%–6% antimony. It has been shown that including antimony in the alloy contributes to increased resistance [24]. Metallurgical antimony is predominantly utilized in lead–acid storage batteries, constituting almost 66% of its overall usage [3].

According to Tercero Espinoza et al. [25], substituting antimony in specific applications is relatively easy. Other elements have the potential to serve as substitutes for antimony compounds in various applications. Calcium, copper, selenium, strontium, sulfur, and tin have been identified as potential alternatives to antimony for strengthening lead and replacing antimony in lead–acid batteries. It is worth noting that these substitutes have demonstrated improved performance in certain cases [9]. The implementation of substitutes may necessitate modifications in manufacturing procedures and industrial equipment. However, it is important to note that these substitutes have their own supply challenges and may incur higher costs.

Antimony recovery through recycling has been achieved in certain cases, especially in specific applications where it is employed as an addition in lead alloys. Most secondary antimony metal, i.e., recovered after recycling, is derived from the recycling of lead–acid batteries, which typically contain a Sb content ranging from 0.6% to 1.5% [22]. Secondary antimony plays a substantial role in the supply chain of several nations, constituting around 20% of the overall antimony utilized and amounting to an annual production of over 40,000 tons [22][26].

Antimony mining and refining processes give rise to significant environmental concerns since, in humans, antimony has been associated with many disorders affecting the liver, pulmonary, and cardiovascular systems, as well as the skin [27]. The Rish [28] and Seal et al. [3] studies present a thorough review of the environmental considerations concerning antimony. Presently, there is a lack of comprehensive environmental studies concerning case studies that examine the behavior of antimony and associated trace elements in a modern mining environment [3]. The environmental concern of the local communities is one of the main reasons for the cancellation of mining projects, especially in developed countries.

2.3. Characteristics and Classifications of Antimony Deposits

Antimony occurs in many ore deposits in diverse geological settings, types, and ages. However, it is important to acknowledge that the occurrence of elevated concentrations of antimony in ores is infrequent, and the presence of economically exploited stibnite deposits is generally constrained by restricted size and sporadic features (Figure 3) [22]. Usually, these types of deposits are associated with hydrothermal processes [29] and, in several cases, are tectonically controlled. The deposits that produce antimony can be classified into two primary categories based on their metal and mineral composition: (i) deposits primarily consisting of simple stibnite, where antimony is the main commodity extracted during mining operations, and (ii) complex polymetallic deposits containing varying amounts of different elements, where antimony is obtained as a byproduct of mining for other commodities [3][22]. According to Schwarz-Schampera [22], these types of antimony deposit can be distinguished based on fluid generation and metal source into: (i) low-temperature hydrothermal (epithermal) origin in shallow crustal environments associated with magmatic fluids, (ii) metamorphogenic hydrothermal origin in consolidated crustal environments derived from crustal fluids, triggered by, and with contributions from, magmatic heat and expelled fluids; and (iii) reduced intrusion-related gold systems.

Antimony fissure-vein deposits can manifest in areas enclosed by extensive shear zones and strike-slip fault zones [3]. According to the study conducted by Pitcairn et al. [30], it was suggested that high-grade metamorphism, distinguished by temperatures over 400 °C, can facilitate the mobilization of antimony and its subsequent transportation by hydrothermal fluids. Under certain conditions, these fluids may subsequently lead to the development of quartz–antimony veins at lower temperatures. Most prominent quartz–stibnite deposits exhibit distinct features, such as siliciclastic sedimentary host rocks and focused migration pathways for upward hydrothermal fluid circulation from deeper high-temperature crustal levels. The primary sources of present and recent mine production are the quartz–stibnite veins and replacement deposits. Various types of hydrothermal systems have the potential to give rise to these formations, such as the peripheral regions of orogenic gold deposits, intrusion-related gold deposits, porphyry copper and molybdenum deposits, polymetallic mesothermal vein deposits, and sediment-hosted Carlin-type gold deposits [31]. Additionally, they may be isolated without any discernible connection to other mineral deposits. Notable quartz–stibnite deposits of the utmost importance include the Kharma deposit (Bolivia), the Beaver Brook and Lake George deposits (Canada), the Xikuangshan deposit (China), the Sarylakh and Sentachan deposits (Russia), the Consolidated Murchison deposit (South Africa), and the Yellow Pine and U.S. Antimony Mine deposits in Montana (MT, USA) (Figure 3) [3].

There are many deposits, such as the Xikuangshan deposit (China), the Sentachan and Sarylakh (Russia), the Antimony Line deposit (South Africa), and the U.S. Antimony Mine in Montana (USA), that exhibit a connection with notable structural fault systems. These fault systems can facilitate the migration of deep regional metamorphic fluids. However, it is important to acknowledge that igneous heat sources associated with more confined fault and fracture zones have been detected at the deposits in Bolivia and the Lake George and Beaver Brook deposits (Canada) [3].

Antimony-bearing deposits are generally associated with calc-alkaline to peralkaline, porphyritic felsic to intermediate volcanic, and intrusive rocks in a volcanic cauldron setting. The host rocks exhibit varying hydrothermal alteration processes, including silicification, carbonatization, sericitization, chloritization, and greisenization. The primary volcanic host rocks consist of submarine, subaerial, and pyroclastic deposits, mostly composed of rhyodacite, dacite, and andesite. Intrusive host rocks range from subvolcanic to hypabyssal and consist of granite, granodiorite, quartz, and monzonite. Antimony deposits associated with intrusions, such as skarns, replacement ores, and vein-type deposits, occur near the magmatic source and are influenced by magmatic-hydrothermal processes. These deposits are generally found in plutons of various kinds, exhibiting features of I-, S-, and A-type granitoids [22][32].

Antimony occurs in a large variety of minerals, including sulfides, sulfosalts, oxides, antimonates, and antimonites [3][10]. The occurrence of antimony (Sb0) in its original state is rare, mostly because of its high affinity for sulfur and other metals/metalloids, including cobalt, lead, bismuth, arsenic, and silver. Up to now, 264 unique mineral phases that include antimony have been documented [22]. A few of them have considerable economic importance as valuable sources of antimony. Several notable examples of minerals containing antimony include boulangerite (Pb5Sb4S11), bournonite (PbCuSbS3), gudmundite (FeSbS), jamesonite (Pb4FeSb6S14), polybasite ([(Ag,Cu)6(Sb,As)2S7][Ag9CuS4]), pyrargyrite (Ag3SbS3), tetrahedrite ((Cu,Fe)12Sb4S13), and valentinite (Sb2O3) [7][9]. Pohl (2011) states that the Sb ore has the capacity to include deleterious elements, such as arsenic (As) and mercury (Hg). According to Pohl [33], stibnite (Sb2S3) is the most common and abundant Sb-ore-bearing mineral, typically found in association with small quantities of other metals such as iron (Fe), cobalt (Co), lead (Pb), gold (Au), and silver (Ag). Based on Miller’s [7] findings, it has been observed that the primary Sb ores generally consist of several metallic accessory minerals, including arsenopyrite, chalcopyrite, galena, gold, pyrite, pyrrhotite, sphalerite, and silver. Furthermore, the most prevalent gangue minerals included in these ores are quartz, calcite, and barite. The most regularly observed supergene antimony minerals are bindheimite (Pb2Sb2O6O), kermesite (Sb2S2O), nadorite (PbSbO2Cl), senarmontite (Sb2O3), and stibiconite (Sb3+Sb5+2O6(OH)) [3].

In conclusion, it can be said that enriched levels of antimony are mostly found in low-temperature magmatic-hydrothermal systems inside the epithermal environment. Antimony often demonstrates a tendency for enrichment in the distal segments of these geological systems, particularly at shallow depths and in close proximity to the Earth’s surface. Also, it presents a strong correlation with hydrothermal silica and carbon dioxide, whereas the prevailing rock formation is generally carbonate, present either as sedimentary limestone or a notable hydrothermal alteration mineral phase [22].

References

- European Commission, Directorate-General for Internal Market. Industry, Entrepreneurship and SMEs. In Study on the Critical Raw Materials for the EU 2023—Final Report; Grohol, M., Veeh, C., Eds.; Publications Office of the European Union: Luxembourg, 2023; Available online: https://data.europa.eu/doi/10.2873/725585 (accessed on 1 September 2023).

- U.S. Congress. Consolidated Appropriations Act. 2021. Available online: https://rules.house.gov/sites/democrats.rules.house.gov/files/BILLS-116HR133SARCP-116-68.pdf (accessed on 4 March 2021).

- Seal, R.R., II; Schulz, K.J.; DeYoung, J.H., Jr.; Sutphin, D.M.; Drew, L.J.; Carlin, J.F., Jr.; Berger, B.R. Antimony. In Critical Mineral Resources of the United States—Economic and Environmental Geology and Prospects for Future Supply; Schulz, K.J., DeYoung, J.H., Jr., Seal, R.R., II, Bradley, D.C., Eds.; Geological Survey Professional Paper 1802; U.S. Geological Survey: Reston, VA, USA, 2017; 19p, C1–C17.

- Lusty, P.A.J.; Shaw, R.A.; Gunn, A.G.; Idoine, N.E. UK Criticality Assessment of Technology Critical Minerals and Metals; British Geological Survey Commissioned Report, CR/21/120; British Geological Survey: Nottingham, UK, 2021; 76p.

- Government of Canada. The Canadian Critical Minerals Strategy. From Exploration to Recycling: Powering the Green and Digital Economy for Canada and the World. Government of Canada. 2022. Available online: https://www.canada.ca/en/campaign/critical-minerals-in-canada/canadian-critical-minerals-strategy.html (accessed on 15 September 2023).

- European Commission. Critical Raw Materials for the EU. European Commission. 2010. Available online: https://ec.europa.eu/growth/sectors/raw-materials/specific-interest/critical_en (accessed on 1 May 2023).

- Miller, M.H. Antimony. In United States Mineral Resources; Brobst, D.A., Pratt, W.P., Eds.; U.S. Geological Survey Professional Paper 820; US Government Printing Office: Washington, DC, USA, 1973; pp. 45–50.

- Rudnick, R.L.; Gao, S. Composition of the Continental Crust, Treatise on Geochemistry, 2nd ed.; Elsevier Ltd.: Amsterdam, The Netherlands, 2014.

- Eyi, E. Antimony Uses, Production, Prices; Tristar Resources plc: London, UK, 2012; p. 14.

- Boyle, R.W.; Jonasson, I.R. The geochemistry of antimony and its use as an indicator element in geochemical prospecting. J. Geochem. Explor. 1984, 20, 223–302.

- Van den Brink, S.; Kleijn, R.; Sprecher, B.; Mancheri, N.; Tukker, A. Resilience in the antimony supply chain. Resour. Conserv. Recycl. 2022, 186, 106586.

- Mordor Intelligence. Market Snapshot. Mordor Intelligence. 2021. Available online: https://www.mordorintelligence.com/industry-reports/antimony-market (accessed on 15 September 2023).

- Perpetua Resources. Antimony. A Critical Metalloid for Manufacturing, National Defense and the Next Generation of Energy Generation and Storage Technologies. Perpetua Resources. 2021. Available online: https://perpetuaresources.com/wp-content/uploads/Antimony-White-Paper.pdf (accessed on 1 February 2023).

- Roskill. Extract of Antimony: Global Industry, Markets and Outlook to 2028, 13th ed; Roskill Information Services Ltd.: London, UK, 2018; 194p.

- U.S. Geological Survey (USGS). USGS Mineral Commodities Summary for 2023: Antimony; USGS: Reston, VA, USA, 2023.

- Carlin, J.F., Jr. Antimony: U.S. Geological Survey Mineral Commodity Summaries 2011; USGS: Reston, VA, USA, 2011; pp. 18–19. Available online: https://minerals.usgs.gov/minerals/pubs/commodity/antimony/mcs-2011-antim.pdf (accessed on 1 September 2022).

- U.S. Geological Survey (USGS). Mineral Commodity Summaries; USGS: Reston, VA, USA, 2022.

- European Commission; Directorate-General for Internal Market, Industry, Entrepreneurship and SMEs; Blengini, G.; Cynthia, E.L.; Eynard, U.; De Matos Cristina, T.; Dominic, W.; Konstantinos, G.; Claudiu, P.; Samuel, C.; et al. Study on the EU’s List of Critical Raw Materials (2020)–Executive Summary; Publications Office: Luxembourg, 2020; Available online: https://data.europa.eu/doi/10.2873/24089 (accessed on 1 February 2023).

- Laznicka, P. Quantitative relationships among giant deposits of metals. Econ. Geol. 1999, 94, 455–473.

- Laznicka, P. Giant Metallic Deposits—Future Sources of Industrial Metals; Springer: Berlin, Germany, 2010; p. 834.

- Guberman, D.E. Antimony: U.S. Geological Survey Mineral Commodity Summaries 2014; USGS: Reston, VA, USA, 2014; pp. 18–19. Available online: https://minerals.usgs.gov/minerals/pubs/commodity/antimony/mcs-2014-antim.pdf (accessed on 1 February 2023).

- Schwarz-Schampera, U. Antimony. In Critical Metals Handbook; Gunn, G., Ed.; Wiley and Sons: Hoboken, NJ, USA, 2014; pp. 70–98.

- U.S. Geological Survey (USGS). Mineral Commodities Summary for 2015: Antimony; USGS: Reston, VA, USA, 2016.

- Gibson, R.I. Type-cast—Antimony, the Metallic Sidekick, Sets the World on Fire and Puts it Out. Geotimes 1998, February, 58. Available online: https://www.gravmag.com/antimony.shtml (accessed on 1 September 2023).

- Tercero Espinoza, L.; Hummen, T.; Brunot, A.; Pena Garay, I.; Velte, D.; Smuk, L.; Todorovic, J.; Eijk, C.; Joce, C. CRM_InnoNet. Critical Raw Materials; Substitution Profiles September 2013 Revised May 2015; European Commission: Brussels, Belgium, 2015; 96p.

- Roskill. The Economics of Antimony, 10th ed.; Roskill Information Services Ltd.: London, UK, 2007; p. 231.

- Wu, F.; Fu, Z.; Liu, B.; Mo, C.; Chen, B.; Corns, W.; Liao, H. Health risk associated with dietary co-exposure to high levels of antimony and arsenic in the world’s largest antimony mine area. Sci. Total Environ. 2011, 409, 3344–3351.

- Rish, M.A. Antimony. In Elements and their Compounds in the Environment—Occurrence, Analysis, and Biological Relevance, 2nd ed.; Merian, E., Anke, M., Ihnat, M., Stoeppler, M., Eds.; Wiley-VCH Verlag: Weinheim, Germany, 2004; Chapter 4; pp. 659–670.

- Obolensky, A.A.; Gushchina, L.V.; Borisenko, A.S.; Borovikov, A.A.; Pavlova, G.G. Antimony in hydrothermal processes. Solubility, conditions of transfer, and metal-bearing capacity of solutions. Russ. Geol. Geophys. 2007, 48, 992–1001.

- Pitcairn, I.K.; Teagle, D.A.; Craw, D.; Olivo, G.R.; Kerrich, R.; Brewer, T.S. Sources of metals and fluids in orogenic gold deposits—Insights from the Otago and Alpine schists, New Zealand. Econ. Geol. 2006, 101, 1525–1546.

- Hofstra, A.H.; Marsh, E.E.; Todorov, T.I.; Emsbo, P. Fluid inclusion evidence for a genetic link between simple antimony veins and giant silver veins in the Coeur d’Alene mining district, ID and MT, USA. Geofluids 2013, 13, 475–493.

- Hart, C.J.R. Reduced intrusion-related gold systems. In Mineral deposits of Canada. A Synthesis of Major Deposit Types, District Metallogeny, the Evolution of Geological Priovinces, and Exploration Methods; Goodfellow, W.D., Ed.; Special Publication No.5; Geological Association of Canada, Mineral Deposits Division: St. John’s, NL, Canada, 2007; pp. 95–112.

- Pohl, W.L. Economic Geology: Principles and Practice; Wiley Blackwell: Hoboken, NJ, USA, 2011.

More

Information

Subjects:

Geology; Others; Mineralogy

Contributors

MDPI registered users' name will be linked to their SciProfiles pages. To register with us, please refer to https://encyclopedia.pub/register

:

View Times:

3.3K

Revisions:

2 times

(View History)

Update Date:

23 Feb 2024

Table of Contents

Notice

You are not a member of the advisory board for this topic. If you want to update advisory board member profile, please contact office@encyclopedia.pub.

OK

Confirm

Only members of the Encyclopedia advisory board for this topic are allowed to note entries. Would you like to become an advisory board member of the Encyclopedia?

Yes

No

${ textCharacter }/${ maxCharacter }

Submit

Cancel

Back

Comments

${ item }

|

${ item.createdUser.fullName }

${ item.createdAt }

${ item.vote }

${ item.reply }

Delete

${ reply.createdUser.fullName }

${ reply.createdAt }

${ reply.vote }

Delete

There is no reply to this comment~

${ item.replyTextCharacter }/${ item.replyMaxCharacter }

Submit

Cancel

More

No more~

There is no comment~

${ textCharacter }/${ maxCharacter }

Submit

Cancel

${ selectedItem.replyTextCharacter }/${ selectedItem.replyMaxCharacter }

Submit

Cancel

Confirm

Are you sure to Delete?

Yes

No