+1 credit

+1 credit

| Version | Summary | Created by | Modification | Content Size | Created at | Operation |

|---|---|---|---|---|---|---|

| 1 | Camila Xu | -- | 15714 | 2022-11-11 01:44:41 |

Video Upload Options

The financial crisis of 2007–08, also known as the global financial crisis and the 2008 financial crisis, was a severe worldwide economic crisis considered by many economists to have been the most serious financial crisis since the Great Depression of the 1930s, to which it is often compared. It began in 2007 with a crisis in the subprime mortgage market in the United States , and developed into a full-blown international banking crisis with the collapse of the investment bank Lehman Brothers on September 15, 2008. Excessive risk-taking by banks such as Lehman Brothers helped to magnify the financial impact globally. Massive bail-outs of financial institutions and other palliative monetary and fiscal policies were employed to prevent a possible collapse of the world financial system. The crisis was nonetheless followed by a global economic downturn, the Great Recession. The Asian markets (China, Hong Kong, Japan, India, etc.) were immediately impacted and volatilized after the U.S. sub-prime crisis. The European debt crisis, a crisis in the banking system of the European countries using the euro, followed later. In 2010, the Dodd–Frank Wall Street Reform and Consumer Protection Act was enacted in the US following the crisis to "promote the financial stability of the United States". The Basel III capital and liquidity standards were adopted by countries around the world.

1. Summary

1.1. Timeline

Following is a timeline of major events during the financial crisis:[1][2][3]

- April 2007: New Century, an American REIT specialising in sub-prime mortgages, filed for Chapter 11 bankruptcy protection. This propagated the sub-prime crisis, through securitization, to banks around the world.[4]

- August 9, 2007: BNP Paribas blocked withdrawals from three of its hedge funds,[5] since there was no liquidity, making valuation of the funds impossible – a clear sign that banks were refusing to do business with each other.[4]

- August 2007: The Federal Open Market Committee began reducing the federal funds rate from its peak of 5.25% in response to worries about liquidity and confidence.

- October 9, 2007: The Dow Jones Industrial Average hit its peak closing price of 14,164.53.[6] Existing home sales also peaked this month and began to decline.

- December 12, 2007: The Federal Reserve instituted the Term Auction Facility to supply short-term credit to banks with sub-prime mortgages.

- February 13, 2008: The Economic Stimulus Act of 2008 was enacted, which included a tax rebate.

- March 17, 2008: The Federal Reserve guaranteed Bear Stearns' bad loans to facilitate its acquisition by JPMorgan Chase.

- July 11, 2008: IndyMac failed.

- July 30, 2008: The Housing and Economic Recovery Act of 2008 was enacted.

- September 7, 2008: Fannie Mae and Freddie Mac were taken over by the federal government.

- September 15, 2008: Lehman Brothers went bankrupt after the Federal Reserve declined to guarantee its loans, causing the Dow Jones to drop 504 points, its worst decline in seven years. The same day, Bank of America purchased Merrill Lynch.

- September 16, 2008: The Federal Reserve took over American International Group. The Reserve Primary Fund "broke the buck" as a result of massive withdrawals from money market accounts.

- September 21, 2008: Goldman Sachs and Morgan Stanley converted themselves from investment banks to bank holding companies to increase their protection by the Federal Reserve.

- September 26, 2008: Washington Mutual went bankrupt after a bank run.

- September 29, 2008: The House of Representatives rejected the Emergency Economic Stabilization Act of 2008 instituting the $700 billion Troubled Asset Relief Program. In response the Dow Jones dropped 777.68 points, its largest single-day decline.

- October 3, 2008: Congress passed the Emergency Economic Stabilization Act of 2008.

- November 25, 2008: The Term Asset-Backed Securities Loan Facility was announced.

- December 16, 2008: The federal funds rate was lowered to zero percent.

- January 2009: Two of the three Big Three automobile manufacturers received a bailout from the TARP program.

- February 13, 2009: Congress approved the American Recovery and Reinvestment Act of 2009, a $787 billion economic stimulus package.

- March 6, 2009: The Dow Jones hit its lowest level of 6,443.27.

1.2. Subprime Mortgage Bubble

The precipitating factor for the Financial Crisis of 2007–2008 was a high default rate in the United States subprime home mortgage sector, i.e. the bursting of the "subprime bubble". This happened when many housing mortgage debtors failed to make their regular payments, leading to a high rate of foreclosures. While the causes of the bubble are disputed, some or all of the following factors must have contributed.

- Low interest rates encouraged mortgage lending.

- Securitization. Many mortgages were bundled together and formed into new financial instruments called mortgage-backed securities, in a process known as securitization. These bundles could be sold as (ostensibly) low-risk securities partly because they were often backed by credit default swaps insurance.[7] Because mortgage lenders could pass these mortgages (and the associated risks) on in this way, they could and did adopt loose underwriting criteria (due in part to outdated and lax regulation).

- Lax regulation allowed predatory lending in the private sector,[8][9] especially after the federal government overrode anti-predatory state laws in 2004.[10]

- The Community Reinvestment Act (CRA),[11] a 1977 US federal law designed to help low- and moderate-income Americans get mortgage loans encouraged banks to grant mortgages to higher risk families.[12][13][14]

- Reckless lending by, for example, Bank of America's Countrywide Financial unit, caused Fannie Mae and Freddie Mac to lose market share and to respond by lowering their own standards.[15]

- Mortgage guarantees. Many of the subprime (high risk) loans were bundled and sold, finally accruing to the quasi-government agencies Fannie Mae and Freddie Mac.[16] The implicit guarantee by the US federal government created a moral hazard and contributed to a glut of risky lending.

The accumulation and subsequent high default rate of these subprime mortgages led to the financial crisis and the consequent damage to the world economy.

1.3. Banking Crisis

High mortgage approval rates led to a large pool of homebuyers, which drove up housing prices. This appreciation in value led large numbers of homeowners (subprime or not) to borrow against their homes as an apparent windfall. This "bubble" would be burst by a rising single-family residential mortgages delinquency rate beginning in August 2006 and peaking in the first quarter, 2010.[17]

The high delinquency rates led to a rapid devaluation of financial instruments (mortgage-backed securities including bundled loan portfolios, derivatives and credit default swaps). As the value of these assets plummeted, the market (buyers) for these securities evaporated and banks who were heavily invested in these assets began to experience a liquidity crisis. Freddie Mac and Fannie Mae were taken over by the federal government on September 7, 2008. Lehman Brothers filed for bankruptcy on September 15, 2008. Merrill Lynch, AIG, HBOS, Royal Bank of Scotland, Bradford & Bingley, Fortis, Hypo Real Estate, and Alliance & Leicester were all expected to follow—with a US federal bailout announced the following day beginning with $85 billion to AIG. In spite of trillions[18] paid out by the US federal government, it became much more difficult to borrow money. The resulting decrease in buyers caused housing prices to plummet. In 2018, Alistair Darling, who was the U.K.'s Chancellor of the Exchequer at the time, spoke out and stated that Britain came within hours of "a breakdown of law and order" the day that RBS was bailed-out.[19]

1.4. Consequences

While the collapse of large financial institutions was prevented by the bailout of banks by national governments, stock markets still dropped worldwide. In many areas, the housing market also suffered, resulting in evictions, foreclosures, and prolonged unemployment. The crisis played a significant role in the failure of key businesses, declines in consumer wealth estimated in trillions of US dollars, and a downturn in economic activity leading to the Great Recession of 2008–2012 and contributing to the European sovereign-debt crisis.[20][21] The active phase of the crisis, which manifested as a liquidity crisis, can be dated from August 9, 2007, when BNP Paribas terminated withdrawals from three funds citing "a complete evaporation of liquidity".[5]

The bursting of the US housing bubble, which peaked at the end of 2006,[22][23] caused the values of securities tied to US real estate pricing to plummet, damaging financial institutions globally.[24] The financial crisis was triggered by a complex interplay of policies that encouraged home ownership, providing easier access to loans for subprime borrowers; overvaluation of bundled subprime mortgages based on the theory that housing prices would continue to escalate; questionable trading practices on behalf of both buyers and sellers; compensation structures that prioritize short-term deal flow over long-term value creation; and a lack of adequate capital holdings from banks and insurance companies to back the financial commitments they were making.[25][26][27] Questions regarding bank solvency, declines in credit availability, and damaged investor confidence affected global stock markets, where securities suffered large losses during 2008 and early 2009. Economies worldwide slowed during this period, as credit tightened and international trade declined.[28] Governments and central banks responded with unprecedented fiscal stimulus, monetary policy expansion and institutional bailouts.[29] In the US, Congress passed the American Recovery and Reinvestment Act of 2009.

1.5. Background Causes

Many causes for the financial crisis have been suggested, with varying weight assigned by experts.[30]

- The US Senate's Levin–Coburn Report concluded that the crisis was the result of "high risk, complex financial products; undisclosed conflicts of interest; the failure of regulators, the credit rating agencies, and the market itself to rein in the excesses of Wall Street".[31]

- The Financial Crisis Inquiry Commission concluded that the financial crisis was avoidable and was caused by "widespread failures in financial regulation and supervision", "dramatic failures of corporate governance and risk management at many systemically important financial institutions", "a combination of excessive borrowing, risky investments, and lack of transparency" by financial institutions, ill preparation and inconsistent action by government that "added to the uncertainty and panic", a "systemic breakdown in accountability and ethics", "collapsing mortgage-lending standards and the mortgage securitization pipeline", deregulation of over-the-counter derivatives, especially credit default swaps, and "the failures of credit rating agencies" to correctly price risk.[32]

- The 1999 part-repeal of the Glass-Steagall Act effectively removed the separation between investment banks and depository banks in the United States.[33]

- Critics argued that credit rating agencies[34][35] and investors failed to accurately price the risk involved with mortgage-related financial products, and that governments did not adjust their regulatory practices to address 21st-century financial markets.[36]

- Research into the causes of the financial crisis has also focused on the role of interest rate spreads.[37]

- Fair value accounting was issued as US accounting standard SFAS 157 in 2006 by the privately run Financial Accounting Standards Board (FASB)—delegated by the SEC with the task of establishing financial reporting standards.[38] This required that tradable assets such as mortgage securities be valued according to their current market value rather than their historic cost or some future expected value. When the market for such securities became volatile and collapsed, the resulting loss of value had a major financial effect upon the institutions holding them even if they had no immediate plans to sell them.[39]

2. Causes

The immediate cause or trigger of the crisis was the bursting of the US housing bubble, which peaked in 2006/2007.[22][23] Already-rising default rates on "subprime" and adjustable-rate mortgages (ARM) began to increase quickly thereafter.

Easy availability of credit in the US, fueled by large inflows of foreign funds after the Russian debt crisis and Asian financial crisis of the 1997–1998 period, led to a housing construction boom and facilitated debt-financed consumer spending. As banks began to give out more loans to potential home owners, housing prices began to rise. Lax lending standards and rising real estate prices also contributed to the real estate bubble. Loans of various types (e.g., mortgage, credit card, and auto) were easy to obtain and consumers assumed an unprecedented debt load.[40][41][42]

As part of the housing and credit booms, the number of financial agreements called mortgage-backed securities (MBS) and collateralized debt obligations (CDO), which derived their value from mortgage payments and housing prices, greatly increased. Such financial innovation enabled institutions and investors around the world to invest in the US housing market. As housing prices declined, major global financial institutions that had borrowed and invested heavily in subprime MBS reported significant losses.[43]

Falling prices also resulted in homes worth less than the mortgage loan, providing borrowers with a financial incentive to enter foreclosure (as borrowers had little incentive to continue paying a loan collateralized with a home with negative net value). The ongoing foreclosure epidemic that began in late 2006 in the US and only reduced to historical levels in early 2014[44] drained significant wealth from consumers, losing up to $4.2 trillion[45] in wealth from home equity. Defaults and losses on other loan types also increased significantly as the crisis expanded from the housing market to other parts of the economy. Total losses are estimated in the trillions of US dollars globally.[43]

While the housing and credit bubbles were building, a series of factors caused the financial system to both expand and become increasingly fragile, a process called financialization. US government policy from the 1970s onward has emphasized deregulation to encourage business, which resulted in less oversight of activities and less disclosure of information about new activities undertaken by banks and other evolving financial institutions. Thus, policymakers did not immediately recognize the increasingly important role played by financial institutions such as investment banks and hedge funds, also known as the shadow banking system. Some experts believe these institutions had become as important as commercial (depository) banks in providing credit to the US economy, but they were not subject to the same regulations.[47]

These institutions, as well as certain regulated banks, had also assumed significant debt burdens while providing the loans described above and did not have a financial cushion sufficient to absorb large loan defaults or MBS losses.[48] These losses affected the ability of financial institutions to lend, slowing economic activity. Concerns regarding the stability of key financial institutions drove central banks to provide funds to encourage lending and restore faith in the commercial paper markets, which are integral to funding business operations. Governments also bailed out key financial institutions and implemented economic stimulus programs, assuming significant additional financial commitments.

The US Financial Crisis Inquiry Commission reported its findings in January 2011.[49] It concluded that:

... the crisis was avoidable and was caused by:

- widespread failures in financial regulation, including the Federal Reserve's failure to stem the tide of toxic mortgages;

- dramatic breakdowns in corporate governance including too many financial firms acting recklessly and taking on too much risk;

- an explosive mix of excessive borrowing and risk by households and Wall Street that put the financial system on a collision course with crisis;

- key policy makers ill prepared for the crisis, lacking a full understanding of the financial system they oversaw;

- and systemic breaches in accountability and ethics at all levels.

2.1. Subprime Lending

The 2000s were the decade of subprime borrowers; no longer was this a segment left to fringe lenders. The relaxing of credit lending standards by investment banks and commercial banks drove this about-face. Subprime did not become magically less risky; Wall Street just accepted this higher risk.[50] During a period of tough competition between mortgage lenders for revenue and market share, and when the supply of creditworthy borrowers was limited, mortgage lenders relaxed underwriting standards and originated riskier mortgages to less creditworthy borrowers. In the view of some analysts, the relatively conservative government-sponsored enterprises (GSEs) policed mortgage originators and maintained relatively high underwriting standards prior to 2003. However, as market power shifted from securitizers to originators and as intense competition from private securitizers undermined GSE power, mortgage standards declined and risky loans proliferated. The worst loans were originated in 2004–2007, the years of the most intense competition between securitizers and the lowest market share for the GSEs.

As well as easy credit conditions, there is evidence that competitive pressures contributed to an increase in the amount of subprime lending during the years preceding the crisis. Major US investment banks and GSEs such as Fannie Mae played an important role in the expansion of lending, with GSEs eventually relaxing their standards to try to catch up with the private banks.[51][52]

A contrarian view is that Fannie Mae and Freddie Mac led the way to relaxed underwriting standards, starting in 1995, by advocating the use of easy-to-qualify automated underwriting and appraisal systems, by designing the no-down-payment products issued by lenders, by the promotion of thousands of small mortgage brokers, and by their close relationship to subprime loan aggregators such as Countrywide.[53][54]

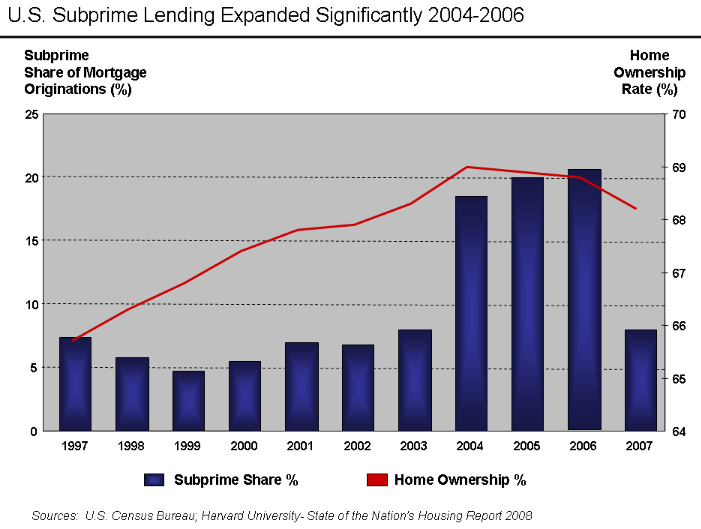

Depending on how "subprime" mortgages are defined, they remained below 10% of all mortgage originations until 2004, when they rose to nearly 20% and remained there through the 2005–2006 peak of the United States housing bubble.[55]

The majority report of the Financial Crisis Inquiry Commission, written by the six Democratic appointees, the minority report, written by three of the four Republican appointees, studies by Federal Reserve economists, and the work of several independent scholars generally contend that government affordable housing policy was not the primary cause of the financial crisis. Although they concede that governmental policies had some role in causing the crisis, they contend that GSE loans performed better than loans securitized by private investment banks, and performed better than some loans originated by institutions that held loans in their own portfolios.

In his dissent to the majority report of the Financial Crisis Inquiry Commission, American Enterprise Institute fellow Peter J. Wallison[56] stated his belief that the roots of the financial crisis can be traced directly and primarily to affordable housing policies initiated by the US Department of Housing and Urban Development (HUD) in the 1990s and to massive risky loan purchases by government-sponsored entities Fannie Mae and Freddie Mac. Later, based upon information in the SEC's December 2011 securities fraud case against six former executives of Fannie and Freddie, Peter Wallison and Edward Pinto estimated that, in 2008, Fannie and Freddie held 13 million substandard loans totaling over $2 trillion.[57]

In the early and mid-2000s, the Bush administration called numerous times[58] for investigation into the safety and soundness of the GSEs and their swelling portfolio of subprime mortgages. On September 10, 2003, the House Financial Services Committee held a hearing at the urging of the administration to assess safety and soundness issues and to review a recent report by the Office of Federal Housing Enterprise Oversight (OFHEO) that had uncovered accounting discrepancies within the two entities.[59] The hearings never resulted in new legislation or formal investigation of Fannie Mae and Freddie Mac, as many of the committee members refused to accept the report and instead rebuked OFHEO for their attempt at regulation.[60] Some believe this was an early warning to the systemic risk that the growing market in subprime mortgages posed to the US financial system that went unheeded.[61]

A 2000 United States Department of the Treasury study of lending trends for 305 cities from 1993 to 1998 showed that $467 billion of mortgage lending was made by Community Reinvestment Act (CRA)-covered lenders into low and mid level income (LMI) borrowers and neighborhoods, representing 10% of all US mortgage lending during the period. The majority of these were prime loans. Sub-prime loans made by CRA-covered institutions constituted a 3% market share of LMI loans in 1998,[62] but in the run-up to the crisis, fully 25% of all sub-prime lending occurred at CRA-covered institutions and another 25% of sub-prime loans had some connection with CRA.[63] However, most sub-prime loans were not made to the LMI borrowers targeted by the CRA, especially in the years 2005–2006 leading up to the crisis, nor did it find any evidence that lending under the CRA rules increased delinquency rates or that the CRA indirectly influenced independent mortgage lenders to ramp up sub-prime lending.

To other analysts the delay between CRA rule changes (in 1995) and the explosion of subprime lending is not surprising, and does not exonerate the CRA. They contend that there were two, connected causes to the crisis: the relaxation of underwriting standards in 1995 and the ultra-low interest rates initiated by the Federal Reserve after the terrorist attack on September 11, 2001. Both causes had to be in place before the crisis could take place.[64] Critics also point out that publicly announced CRA loan commitments were massive, totaling $4.5 trillion in the years between 1994 and 2007.[65] They also argue that the Federal Reserve's classification of CRA loans as "prime" is based on the faulty and self-serving assumption that high-interest-rate loans (3 percentage points over average) equal "subprime" loans.[66]

Others have pointed out that there were not enough of these loans made to cause a crisis of this magnitude. In an article in Portfolio Magazine, Michael Lewis spoke with one trader who noted that "There weren't enough Americans with [bad] credit taking out [bad loans] to satisfy investors' appetite for the end product." Essentially, investment banks and hedge funds used financial innovation to enable large wagers to be made, far beyond the actual value of the underlying mortgage loans, using derivatives called credit default swaps, collateralized debt obligations and synthetic CDOs.[67]

As of March 2011, the FDIC had paid out $9 billion to cover losses on bad loans at 165 failed financial institutions.[68] The Congressional Budget Office estimated, in June 2011, that the bailout to Fannie Mae and Freddie Mac exceeds $300 billion (calculated by adding the fair value deficits of the entities to the direct bailout funds at the time).[69]

Economist Paul Krugman argued in January 2010 that the simultaneous growth of the residential and commercial real estate pricing bubbles and the global nature of the crisis undermines the case made by those who argue that Fannie Mae, Freddie Mac, CRA, or predatory lending were primary causes of the crisis. In other words, bubbles in both markets developed even though only the residential market was affected by these potential causes.[70]

Countering Krugman, Peter J. Wallison wrote: "It is not true that every bubble—even a large bubble—has the potential to cause a financial crisis when it deflates." Wallison notes that other developed countries had "large bubbles during the 1997–2007 period" but "the losses associated with mortgage delinquencies and defaults when these bubbles deflated were far lower than the losses suffered in the United States when the 1997–2007 [bubble] deflated." According to Wallison, the reason the US residential housing bubble (as opposed to other types of bubbles) led to financial crisis was that it was supported by a huge number of substandard loans—generally with low or no downpayments.[71]

Krugman's contention (that the growth of a commercial real estate bubble indicates that US housing policy was not the cause of the crisis) is challenged by additional analysis. After researching the default of commercial loans during the financial crisis, Xudong An and Anthony B. Sanders reported (in December 2010): "We find limited evidence that substantial deterioration in CMBS [commercial mortgage-backed securities] loan underwriting occurred prior to the crisis."[72] Other analysts support the contention that the crisis in commercial real estate and related lending took place after the crisis in residential real estate. Business journalist Kimberly Amadeo reported: "The first signs of decline in residential real estate occurred in 2006. Three years later, commercial real estate started feeling the effects.[73] Denice A. Gierach, a real estate attorney and CPA, wrote:

... most of the commercial real estate loans were good loans destroyed by a really bad economy. In other words, the borrowers did not cause the loans to go bad, it was the economy.[74]

2.2. Growth of the Housing Bubble

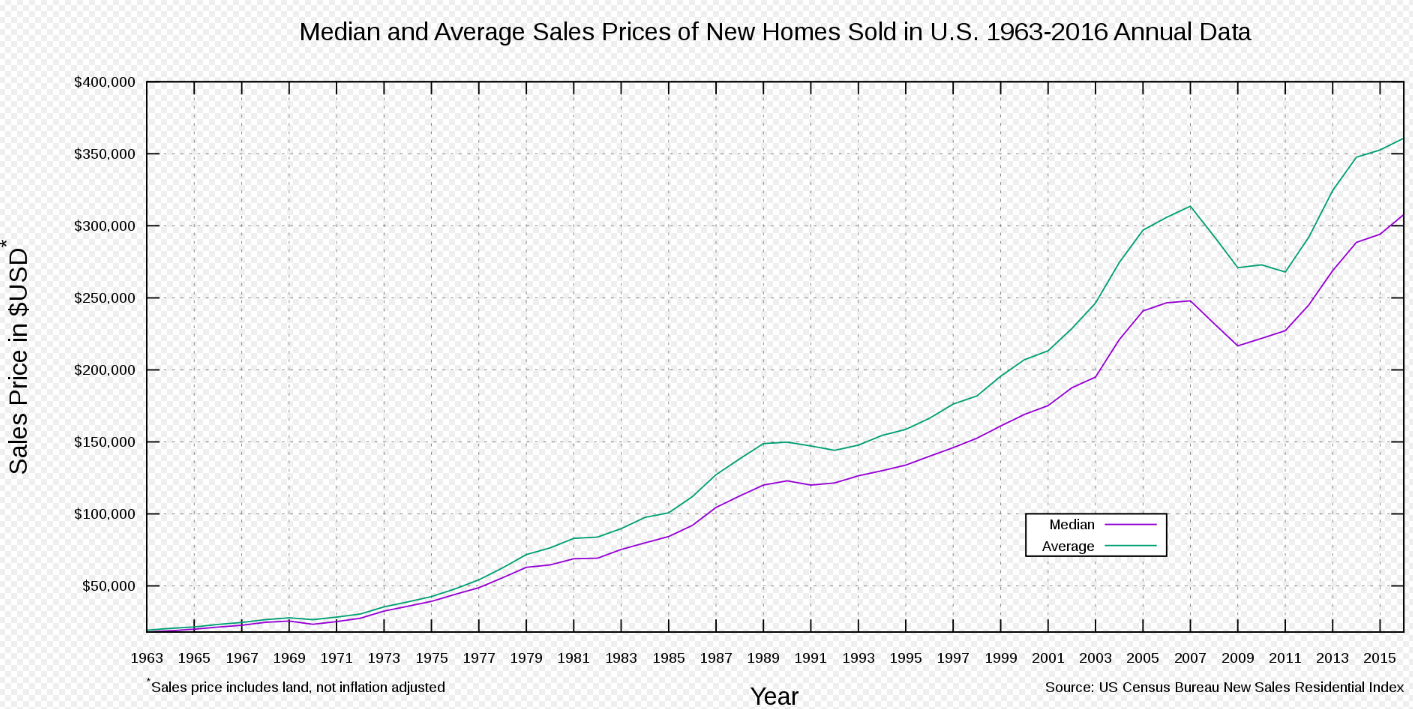

Between 1998 and 2006, the price of the typical American house increased by 124%.[75] In contrast, during the 1980s and 1990s, the national median home price ranged from 2.9 to 3.1 times median household income. This ratio increased to 4.0 in 2004, and 4.6 in 2006.[76] This housing bubble resulted in many homeowners refinancing their homes at lower interest rates, or financing consumer spending by taking out second mortgages secured by the price appreciation.

In a Peabody Award winning program, NPR correspondents argued that a "Giant Pool of Money" (represented by $70 trillion in worldwide fixed income investments) sought higher yields than those offered by US Treasury bonds early in the decade. This pool of money had roughly doubled in size from 2000 to 2007, yet the supply of relatively safe, income generating investments had not grown as fast. Investment banks on Wall Street answered this demand with products such as the mortgage-backed security and the collateralized debt obligation that were assigned safe ratings by the credit rating agencies.[77]

In effect, Wall Street connected this pool of money to the mortgage market in the US, with enormous fees accruing to those throughout the mortgage supply chain, from the mortgage broker selling the loans to small banks that funded the brokers and the large investment banks behind them. By approximately 2003, the supply of mortgages originated at traditional lending standards had been exhausted, and continued strong demand began to drive down lending standards.[77]

The collateralized debt obligation in particular enabled financial institutions to obtain investor funds to finance subprime and other lending, extending or increasing the housing bubble and generating large fees. This essentially places cash payments from multiple mortgages or other debt obligations into a single pool from which specific securities draw in a specific sequence of priority. Those securities first in line received investment-grade ratings from rating agencies. Securities with lower priority had lower credit ratings but theoretically a higher rate of return on the amount invested.[78][79]

By September 2008, average US housing prices had declined by over 20% from their mid-2006 peak.[80][81] As prices declined, borrowers with adjustable-rate mortgages could not refinance to avoid the higher payments associated with rising interest rates and began to default. During 2007, lenders began foreclosure proceedings on nearly 1.3 million properties, a 79% increase over 2006.[82] This increased to 2.3 million in 2008, an 81% increase vs. 2007.[83] By August 2008, approximately 9% of all US mortgages outstanding were either delinquent or in foreclosure.[84] By September 2009, this had risen to 14.4%.[85]

After the bubble burst, Australian economist John Quiggin wrote, "And, unlike the Great Depression, this crisis was entirely the product of financial markets. There was nothing like the postwar turmoil of the 1920s, the struggles over gold convertibility and reparations, or the Smoot-Hawley tariff, all of which have shared the blame for the Great Depression." Instead, Quiggin lays the blame for the 2008 near-meltdown on financial markets, on political decisions to lightly regulate them, and on rating agencies which had self-interested incentives to give good ratings.[86]

2.3. Easy Credit Conditions

Lower interest rates encouraged borrowing. From 2000 to 2003, the Federal Reserve lowered the federal funds rate target from 6.5% to 1.0%.[87] This was done to soften the effects of the collapse of the dot-com bubble and the September 2001 terrorist attacks, as well as to combat a perceived risk of deflation.[88] As early as 2002 it was apparent that credit was fueling housing instead of business investment as some economists went so far as to advocate that the Fed "needs to create a housing bubble to replace the Nasdaq bubble".[89] Moreover, empirical studies using data from advanced countries show that excessive credit growth contributed greatly to the severity of the crisis.[90]

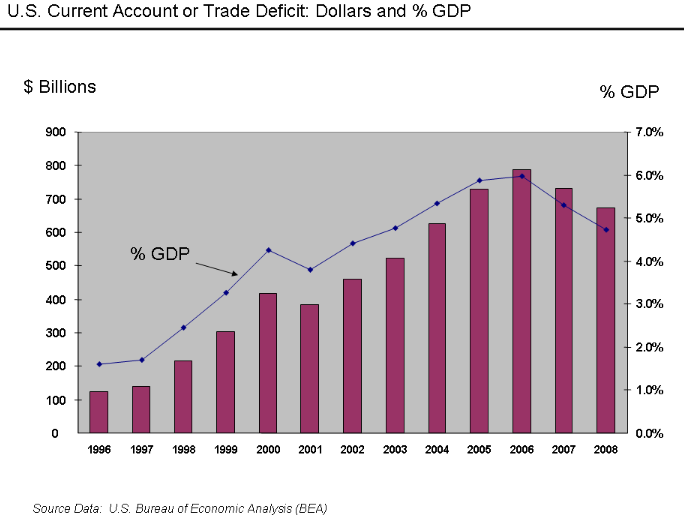

Additional downward pressure on interest rates was created by the high and rising US current account deficit, which peaked along with the housing bubble in 2006. Federal Reserve chairman Ben Bernanke explained how trade deficits required the US to borrow money from abroad, in the process bidding up bond prices and lowering interest rates.[91]

Bernanke explained that between 1996 and 2004, the US current account deficit increased by $650 billion, from 1.5% to 5.8% of GDP. Financing these deficits required the country to borrow large sums from abroad, much of it from countries running trade surpluses. These were mainly the emerging economies in Asia and oil-exporting nations. The balance of payments identity requires that a country (such as the US) running a current account deficit also have a capital account (investment) surplus of the same amount. Hence large and growing amounts of foreign funds (capital) flowed into the US to finance its imports.

All of this created demand for various types of financial assets, raising the prices of those assets while lowering interest rates. Foreign investors had these funds to lend either because they had very high personal savings rates (as high as 40% in China) or because of high oil prices. Ben Bernanke has referred to this as a "saving glut".[92]

A flood of funds (capital or liquidity) reached the US financial markets. Foreign governments supplied funds by purchasing Treasury bonds and thus avoided much of the direct effect of the crisis. US households, on the other hand, used funds borrowed from foreigners to finance consumption or to bid up the prices of housing and financial assets. Financial institutions invested foreign funds in mortgage-backed securities.

The Fed then raised the Fed funds rate significantly between July 2004 and July 2006.[93] This contributed to an increase in 1-year and 5-year adjustable-rate mortgage (ARM) rates, making ARM interest rate resets more expensive for homeowners.[94] This may have also contributed to the deflating of the housing bubble, as asset prices generally move inversely to interest rates, and it became riskier to speculate in housing.[95][96] US housing and financial assets dramatically declined in value after the housing bubble burst.[97][98]

2.4. Weak and Fraudulent Underwriting Practices

Subprime lending standards declined in the USA: in early 2000, a subprime borrower had a FICO score of 660 or less. By 2005, many lenders dropped the required FICO score to 620, making it much easier to qualify for prime loans and making subprime lending a riskier business. Proof of income and assets were de-emphasized. Loans moved from full documentation to low documentation to no documentation. One subprime mortgage product that gained wide acceptance was the no income, no job, no asset verification required (NINJA) mortgage. Informally, these loans were aptly referred to as "liar loans" because they encouraged borrowers to be less than honest in the loan application process.[99] Testimony given to the Financial Crisis Inquiry Commission by Richard M. Bowen III on events during his tenure as the Business Chief Underwriter for Correspondent Lending in the Consumer Lending Group for Citigroup (where he was responsible for over 220 professional underwriters) suggests that by the final years of the US housing bubble (2006–2007), the collapse of mortgage underwriting standards was endemic. His testimony stated that by 2006, 60% of mortgages purchased by Citi from some 1,600 mortgage companies were "defective" (were not underwritten to policy, or did not contain all policy-required documents)—this, despite the fact that each of these 1,600 originators was contractually responsible (certified via representations and warrantees) that its mortgage originations met Citi's standards. Moreover, during 2007, "defective mortgages (from mortgage originators contractually bound to perform underwriting to Citi's standards) increased ... to over 80% of production".[100]

In separate testimony to Financial Crisis Inquiry Commission, officers of Clayton Holdings—the largest residential loan due diligence and securitization surveillance company in the United States and Europe—testified that Clayton's review of over 900,000 mortgages issued from January 2006 to June 2007 revealed that scarcely 54% of the loans met their originators' underwriting standards. The analysis (conducted on behalf of 23 investment and commercial banks, including 7 "too big to fail" banks) additionally showed that 28% of the sampled loans did not meet the minimal standards of any issuer. Clayton's analysis further showed that 39% of these loans (i.e. those not meeting any issuer's minimal underwriting standards) were subsequently securitized and sold to investors.[101][102]

2.5. Predatory Lending

Predatory lending refers to the practice of unscrupulous lenders, enticing borrowers to enter into "unsafe" or "unsound" secured loans for inappropriate purposes.[103]

Countrywide Financial, sued by California Attorney General Jerry Brown for "unfair business practices" and "false advertising", was making high cost mortgages "to homeowners with weak credit, adjustable rate mortgages (ARMs) that allowed homeowners to make interest-only payments".[104] When housing prices decreased, homeowners in ARMs then had little incentive to pay their monthly payments, since their home equity had disappeared. This caused Countrywide's financial condition to deteriorate, ultimately resulting in a decision by the Office of Thrift Supervision to seize the lender. One Countrywide employee—who would later plead guilty to two counts of wire fraud and spent 18 months in prison—stated that, "If you had a pulse, we gave you a loan."[105]

Former employees from Ameriquest, which was United States' leading wholesale lender,[106] described a system in which they were pushed to falsify mortgage documents and then sell the mortgages to Wall Street banks eager to make fast profits.[106] There is growing evidence that such mortgage frauds may be a cause of the crisis.[106]

2.6. Deregulation

A 2012 OECD study[107] suggest that bank regulation based on the Basel accords encourage unconventional business practices and contributed to or even reinforced the financial crisis. In other cases, laws were changed or enforcement weakened in parts of the financial system. Key examples include:

- Jimmy Carter's Depository Institutions Deregulation and Monetary Control Act of 1980 (DIDMCA) phased out a number of restrictions on banks' financial practices, broadened their lending powers, allowed credit unions and savings and loans to offer checkable deposits, and raised the deposit insurance limit from $40,000 to $100,000 (thereby potentially lessening depositor scrutiny of lenders' risk management policies).[108]

- In October 1982, US President Ronald Reagan signed into law the Garn–St. Germain Depository Institutions Act, which provided for adjustable-rate mortgage loans, began the process of banking deregulation, and contributed to the savings and loan crisis of the late 1980s/early 1990s.[109]

- In November 1999, US President Bill Clinton signed into law the Gramm–Leach–Bliley Act, which repealed provisions of the Glass-Steagall Act that prohibit a bank holding company from owning other financial companies. The repeal effectively removed the separation that previously existed between Wall Street investment banks and depository banks, providing a government stamp of approval for a universal risk-taking banking model. Investment banks such as Lehman would now be thrust into direct competition with commercial banks.[110] Most analysts say that this repeal directly contributed to the severity of the Financial crisis of 2007–2010. However, there is perspective that repeal made little difference because the institutions that were greatly affected did not fall under the jurisdiction of the act itself.[111]

- In December 2000, President Clinton signed the Commodities Futures Modernization Act of 2000 into law. Written by Congress with lobbying assistance from the financial industry, it banned the further regulation of the derivatives market.

- In 2004, the US Securities and Exchange Commission relaxed the net capital rule, which enabled investment banks to substantially increase the level of debt they were taking on, fueling the growth in mortgage-backed securities supporting subprime mortgages. The SEC has conceded that self-regulation of investment banks contributed to the crisis.[112][113]

- Financial institutions in the shadow banking system are not subject to the same regulation as depository banks, allowing them to assume additional debt obligations relative to their financial cushion or capital base.[114] This was the case despite the Long-Term Capital Management debacle in 1998, in which a highly leveraged shadow institution failed with systemic implications and was bailed out.

- Regulators and accounting standard-setters allowed depository banks such as Citigroup to move significant amounts of assets and liabilities off-balance sheet into complex legal entities called structured investment vehicles, masking the weakness of the capital base of the firm or degree of leverage or risk taken. One news agency estimated that the top four US banks will have to return between $500 billion and $1 trillion to their balance sheets during 2009.[115] This increased uncertainty during the crisis regarding the financial position of the major banks.[116] Off-balance sheet entities were also used by Enron as part of the scandal that brought down that company in 2001.[117]

- As early as 1997, Federal Reserve chairman Alan Greenspan fought to keep the derivatives market unregulated.[118] With the advice of the President's Working Group on Financial Markets,[119] the US Congress and President Bill Clinton allowed the self-regulation of the over-the-counter derivatives market when they enacted the Commodity Futures Modernization Act of 2000. Derivatives such as credit default swaps (CDS) can be used to hedge or speculate against particular credit risks without necessarily owning the underlying debt instruments. The volume of CDS outstanding increased 100-fold from 1998 to 2008, with estimates of the debt covered by CDS contracts, as of November 2008, ranging from US$33 to $47 trillion. Total over-the-counter (OTC) derivative notional value rose to $683 trillion by June 2008.[120] Warren Buffett famously referred to derivatives as "financial weapons of mass destruction" in early 2003.[121][122]

2.7. Increased Debt Burden or Overleveraging

Prior to the crisis, financial institutions became highly leveraged, increasing their appetite for risky investments and reducing their resilience in case of losses. Much of this leverage was achieved using complex financial instruments such as off-balance sheet securitization and derivatives, which made it difficult for creditors and regulators to monitor and try to reduce financial institution risk levels.

US households and financial institutions became increasingly indebted or overleveraged during the years preceding the crisis.[123] This increased their vulnerability to the collapse of the housing bubble and worsened the ensuing economic downturn.[124] Key statistics include:

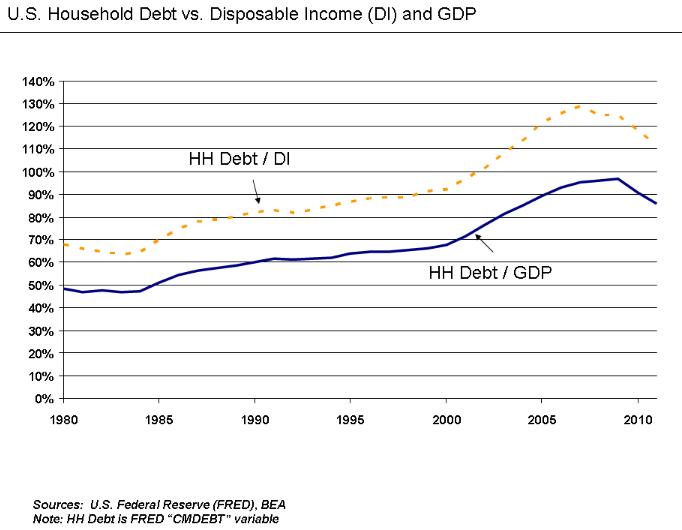

Free cash used by consumers from home equity extraction doubled from $627 billion in 2001 to $1,428 billion in 2005 as the housing bubble built, a total of nearly $5 trillion over the period, contributing to economic growth worldwide.[125][126][127] US home mortgage debt relative to GDP increased from an average of 46% during the 1990s to 73% during 2008, reaching $10.5 trillion.[128]

US household debt as a percentage of annual disposable personal income was 127% at the end of 2007, versus 77% in 1990.[123] In 1981, US private debt was 123% of GDP; by the third quarter of 2008, it was 290%.[129]

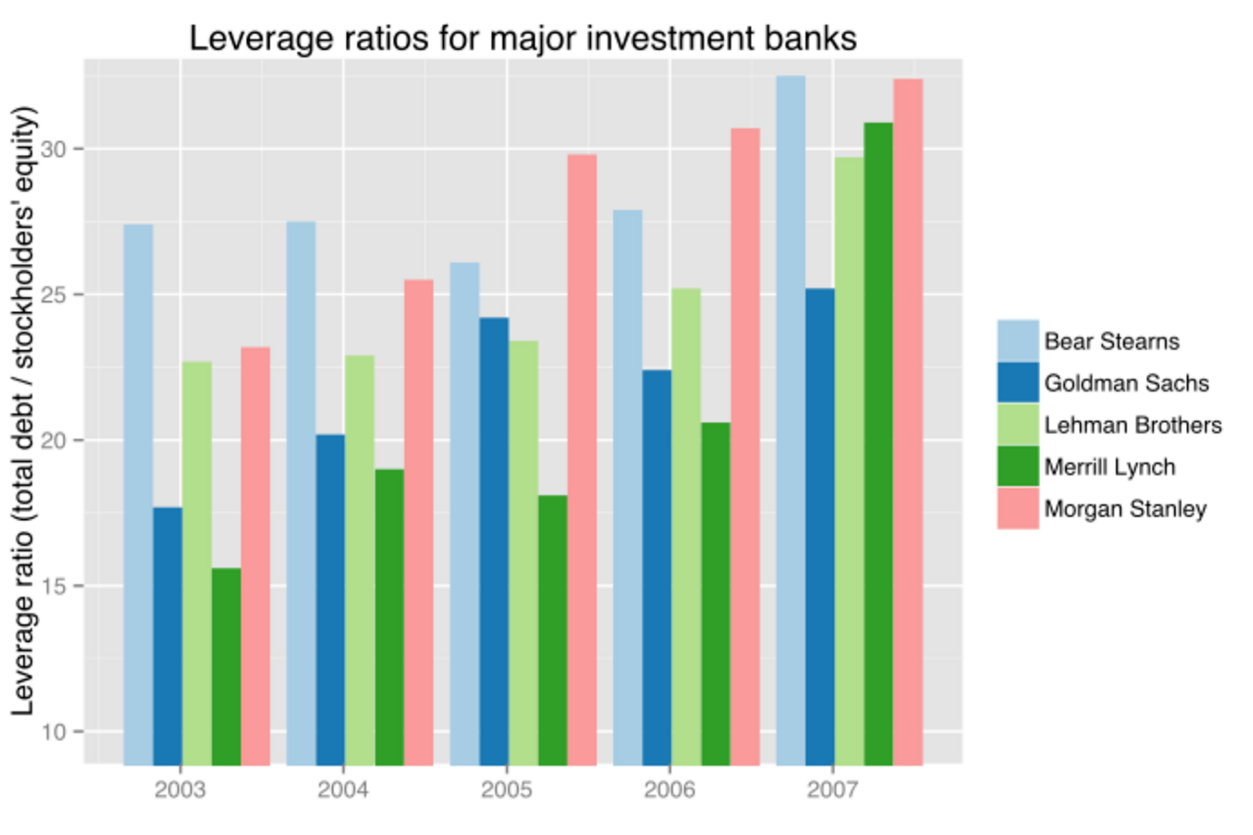

From 2004 to 2007, the top five US investment banks each significantly increased their financial leverage (see diagram), which increased their vulnerability to a financial shock. Changes in capital requirements, intended to keep US banks competitive with their European counterparts, allowed lower risk weightings for AAA securities. The shift from first-loss tranches to AAA tranches was seen by regulators as a risk reduction that compensated the higher leverage.[130] These five institutions reported over $4.1 trillion in debt for fiscal year 2007, about 30% of US nominal GDP for 2007. Lehman Brothers went bankrupt and was liquidated, Bear Stearns and Merrill Lynch were sold at fire-sale prices, and Goldman Sachs and Morgan Stanley became commercial banks, subjecting themselves to more stringent regulation. With the exception of Lehman, these companies required or received government support.[131] Lehman reported that it had been in talks with Bank of America and Barclays for the company's possible sale. However, both Barclays and Bank of America ultimately declined to purchase the entire company.[132]

Fannie Mae and Freddie Mac, two US government-sponsored enterprises, owned or guaranteed nearly $5 trillion in mortgage obligations at the time they were placed into conservatorship by the US government in September 2008.[133][134]

These seven entities were highly leveraged and had $9 trillion in debt or guarantee obligations; yet they were not subject to the same regulation as depository banks.[114][135]

Behavior that may be optimal for an individual (e.g., saving more during adverse economic conditions) can be detrimental if too many individuals pursue the same behavior, as ultimately one person's consumption is another person's income. Too many consumers attempting to save (or pay down debt) simultaneously is called the paradox of thrift and can cause or deepen a recession. Economist Hyman Minsky also described a "paradox of deleveraging" as financial institutions that have too much leverage (debt relative to equity) cannot all de-leverage simultaneously without significant declines in the value of their assets.[124]

In April 2009, US Federal Reserve vice-chair Janet Yellen discussed these paradoxes:

Once this massive credit crunch hit, it didn't take long before we were in a recession. The recession, in turn, deepened the credit crunch as demand and employment fell, and credit losses of financial institutions surged. Indeed, we have been in the grips of precisely this adverse feedback loop for more than a year. A process of balance sheet deleveraging has spread to nearly every corner of the economy. Consumers are pulling back on purchases, especially on durable goods, to build their savings. Businesses are cancelling planned investments and laying off workers to preserve cash. And, financial institutions are shrinking assets to bolster capital and improve their chances of weathering the current storm. Once again, Minsky understood this dynamic. He spoke of the paradox of deleveraging, in which precautions that may be smart for individuals and firms—and indeed essential to return the economy to a normal state—nevertheless magnify the distress of the economy as a whole.[124]

2.8. Financial Innovation and Complexity

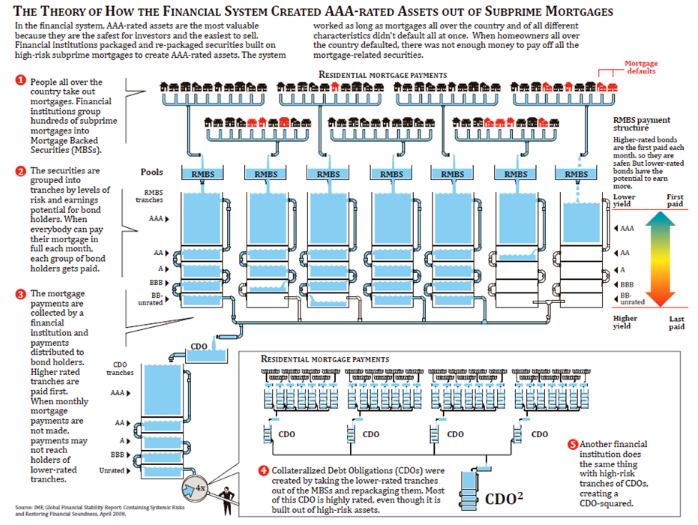

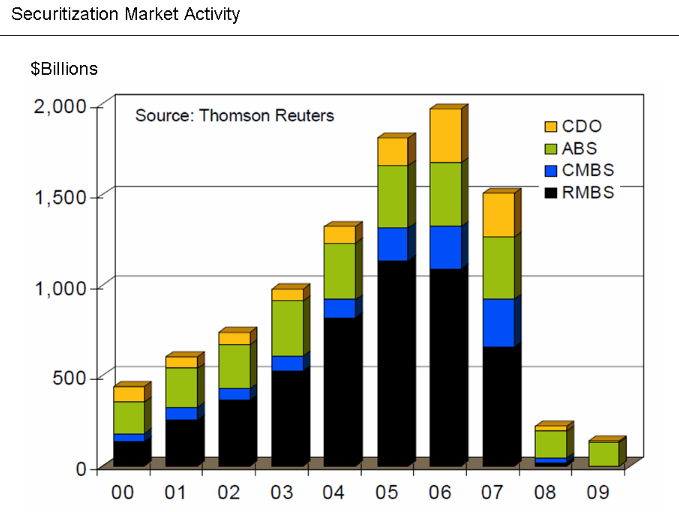

The term financial innovation refers to the ongoing development of financial products designed to achieve particular client objectives, such as offsetting a particular risk exposure (such as the default of a borrower) or to assist with obtaining financing. Examples pertinent to this crisis included: the adjustable-rate mortgage; the bundling of subprime mortgages into mortgage-backed securities (MBS) or collateralized debt obligations (CDO) for sale to investors, a type of securitization; and a form of credit insurance called credit default swaps (CDS). The usage of these products expanded dramatically in the years leading up to the crisis. These products vary in complexity and the ease with which they can be valued on the books of financial institutions.

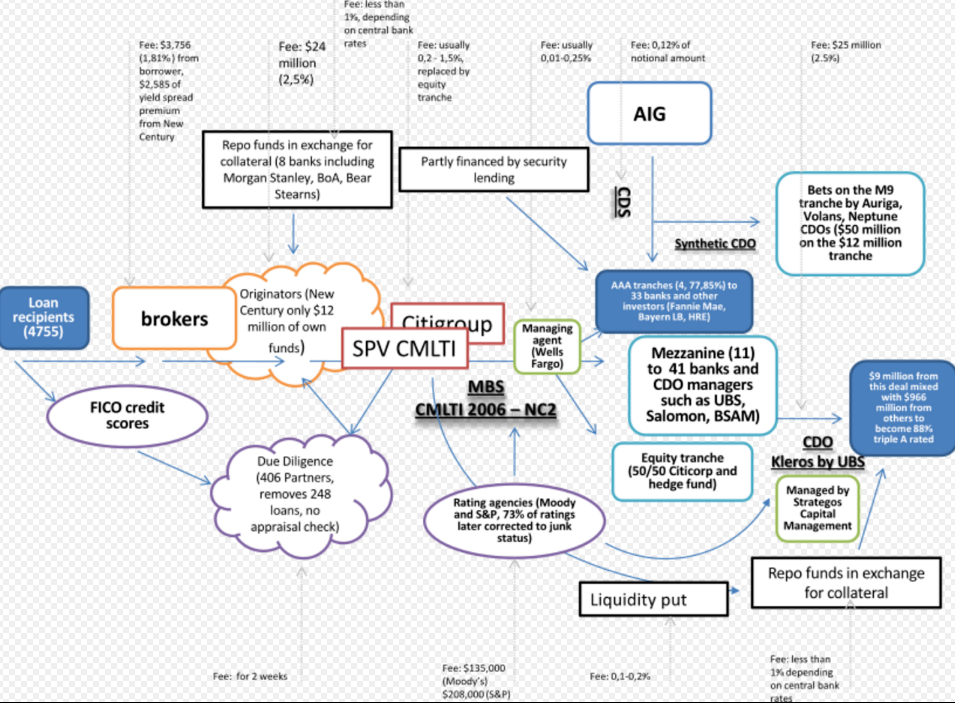

CDO issuance grew from an estimated $20 billion in Q1 2004 to its peak of over $180 billion by Q1 2007, then declined back under $20 billion by Q1 2008. Further, the credit quality of CDO's declined from 2000 to 2007, as the level of subprime and other non-prime mortgage debt increased from 5% to 36% of CDO assets.[136] As described in the section on subprime lending, the CDS and portfolio of CDS called synthetic CDO enabled a theoretically infinite amount to be wagered on the finite value of housing loans outstanding, provided that buyers and sellers of the derivatives could be found. For example, buying a CDS to insure a CDO ended up giving the seller the same risk as if they owned the CDO, when those CDO's became worthless.[137]

This boom in innovative financial products went hand in hand with more complexity. It multiplied the number of actors connected to a single mortgage (including mortgage brokers, specialized originators, the securitizers and their due diligence firms, managing agents and trading desks, and finally investors, insurances and providers of repo funding). With increasing distance from the underlying asset these actors relied more and more on indirect information (including FICO scores on creditworthiness, appraisals and due diligence checks by third party organizations, and most importantly the computer models of rating agencies and risk management desks). Instead of spreading risk this provided the ground for fraudulent acts, misjudgments and finally market collapse.[138]

Martin Wolf further wrote in June 2009 that certain financial innovations enabled firms to circumvent regulations, such as off-balance sheet financing that affects the leverage or capital cushion reported by major banks, stating: "... an enormous part of what banks did in the early part of this decade—the off-balance-sheet vehicles, the derivatives and the 'shadow banking system' itself—was to find a way round regulation."[139]

2.9. Incorrect Pricing of Risk

Mortgage risks were underestimated by almost all institutions in the chain from originator to investor by underweighting the possibility of falling housing prices based on historical trends of the past 50 years. Limitations of default and prepayment models, the heart of pricing models, led to overvaluation of mortgage and asset-backed products and their derivatives by originators, securitizers, broker-dealers, rating-agencies, insurance underwriters and the vast majority of investors (with the exception of certain hedge funds).[140][141] While financial derivatives and structured products helped partition and shift risk between financial participants, it was the underestimation of falling housing prices and the resultant losses that led to aggregate risk.[141]

The pricing of risk refers to the incremental compensation required by investors for taking on additional risk, which may be measured by interest rates or fees. Several scholars have argued that a lack of transparency about banks' risk exposures prevented markets from correctly pricing risk before the crisis, enabled the mortgage market to grow larger than it otherwise would have, and made the financial crisis far more disruptive than it would have been if risk levels had been disclosed in a straightforward, readily understandable format.

For a variety of reasons, market participants did not accurately measure the risk inherent with financial innovation such as MBS and CDOs or understand its effect on the overall stability of the financial system.[36] For example, the pricing model for CDOs clearly did not reflect the level of risk they introduced into the system. Banks estimated that $450 billion of CDO were sold between "late 2005 to the middle of 2007"; among the $102 billion of those that had been liquidated, JPMorgan estimated that the average recovery rate for "high quality" CDOs was approximately 32 cents on the dollar, while the recovery rate for mezzanine CDO was approximately five cents for every dollar.[142]

Another example relates to AIG, which insured obligations of various financial institutions through the usage of credit default swaps. The basic CDS transaction involved AIG receiving a premium in exchange for a promise to pay money to party A in the event party B defaulted. However, AIG did not have the financial strength to support its many CDS commitments as the crisis progressed and was taken over by the government in September 2008. US taxpayers provided over $180 billion in government support to AIG during 2008 and early 2009, through which the money flowed to various counterparties to CDS transactions, including many large global financial institutions.[143][144]

The Financial Crisis Inquiry Commission (FCIC) made the major government study of the crisis. It concluded in January 2011:

The Commission concludes AIG failed and was rescued by the government primarily because its enormous sales of credit default swaps were made without putting up the initial collateral, setting aside capital reserves, or hedging its exposure—a profound failure in corporate governance, particularly its risk management practices. AIG's failure was possible because of the sweeping deregulation of over-the-counter (OTC) derivatives, including credit default swaps, which effectively eliminated federal and state regulation of these products, including capital and margin requirements that would have lessened the likelihood of AIG's failure.[145][146][147]

The limitations of a widely used financial model also were not properly understood.[148][149] This formula assumed that the price of CDS was correlated with and could predict the correct price of mortgage-backed securities. Because it was highly tractable, it rapidly came to be used by a huge percentage of CDO and CDS investors, issuers, and rating agencies.[149] According to one wired.com article:

Then the model fell apart. Cracks started appearing early on, when financial markets began behaving in ways that users of Li's formula hadn't expected. The cracks became full-fledged canyons in 2008—when ruptures in the financial system's foundation swallowed up trillions of dollars and put the survival of the global banking system in serious peril... Li's Gaussian copula formula will go down in history as instrumental in causing the unfathomable losses that brought the world financial system to its knees.[149]

As financial assets became more complex and harder to value, investors were reassured by the fact that the international bond rating agencies and bank regulators accepted as valid some complex mathematical models that showed the risks were much smaller than they actually were.[150] George Soros commented that "The super-boom got out of hand when the new products became so complicated that the authorities could no longer calculate the risks and started relying on the risk management methods of the banks themselves. Similarly, the rating agencies relied on the information provided by the originators of synthetic products. It was a shocking abdication of responsibility."[151]

Moreover, a conflict of interest between professional investment managers and their institutional clients, combined with a global glut in investment capital, led to bad investments by asset managers in over-priced credit assets. Professional investment managers generally are compensated based on the volume of client assets under management. There is, therefore, an incentive for asset managers to expand their assets under management in order to maximize their compensation. As the glut in global investment capital caused the yields on credit assets to decline, asset managers were faced with the choice of either investing in assets where returns did not reflect true credit risk or returning funds to clients. Many asset managers continued to invest client funds in over-priced (under-yielding) investments, to the detriment of their clients, so they could maintain their assets under management. They supported this choice with a "plausible deniability" of the risks associated with subprime-based credit assets because the loss experience with early "vintages" of subprime loans was so low.[152]

Despite the dominance of the above formula, there are documented attempts of the financial industry, occurring before the crisis, to address the formula limitations, specifically the lack of dependence dynamics and the poor representation of extreme events.[153] The volume "Credit Correlation: Life After Copulas", published in 2007 by World Scientific, summarizes a 2006 conference held by Merrill Lynch in London where several practitioners attempted to propose models rectifying some of the copula limitations. See also the article by Donnelly and Embrechts[154] and the book by Brigo, Pallavicini and Torresetti, that reports relevant warnings and research on CDOs appeared in 2006.[155]

2.10. Boom and Collapse of the Shadow Banking System

There is strong evidence that the riskiest, worst performing mortgages were funded through the "shadow banking system" and that competition from the shadow banking system may have pressured more traditional institutions to lower their own underwriting standards and originate riskier loans.

In a June 2008 speech, President and CEO of the New York Federal Reserve Bank Timothy Geithner—who in 2009 became Secretary of the United States Treasury—placed significant blame for the freezing of credit markets on a "run" on the entities in the "parallel" banking system, also called the shadow banking system. These entities became critical to the credit markets underpinning the financial system, but were not subject to the same regulatory controls. Further, these entities were vulnerable because of maturity mismatch, meaning that they borrowed short-term in liquid markets to purchase long-term, illiquid and risky assets. This meant that disruptions in credit markets would make them subject to rapid deleveraging, selling their long-term assets at depressed prices. He described the significance of these entities:

In early 2007, asset-backed commercial paper conduits, in structured investment vehicles, in auction-rate preferred securities, tender option bonds and variable rate demand notes, had a combined asset size of roughly $2.2 trillion. Assets financed overnight in triparty repo grew to $2.5 trillion. Assets held in hedge funds grew to roughly $1.8 trillion. The combined balance sheets of the five largest investment banks totaled $4 trillion. In comparison, the total assets of the top five bank holding companies in the United States at that point were just over $6 trillion, and total assets of the entire banking system were about $10 trillion. The combined effect of these factors was a financial system vulnerable to self-reinforcing asset price and credit cycles.[47]

Paul Krugman, laureate of the Nobel Prize in Economics, described the run on the shadow banking system as the "core of what happened" to cause the crisis. He referred to this lack of controls as "malign neglect" and argued that regulation should have been imposed on all banking-like activity.[114]

The securitization markets supported by the shadow banking system started to close down in the spring of 2007 and nearly shut-down in the fall of 2008. More than a third of the private credit markets thus became unavailable as a source of funds.[156] According to the Brookings Institution, the traditional banking system does not have the capital to close this gap as of June 2009: "It would take a number of years of strong profits to generate sufficient capital to support that additional lending volume." The authors also indicate that some forms of securitization are "likely to vanish forever, having been an artifact of excessively loose credit conditions".[157]

2.11. Commodities Boom

Rapid increases in a number of commodity prices followed the collapse in the housing bubble. The price of oil nearly tripled from $50 to $147 from early 2007 to 2008, before plunging as the financial crisis began to take hold in late 2008.[158] Experts debate the causes, with some attributing it to speculative flow of money from housing and other investments into commodities, some to monetary policy,[159] and some to the increasing feeling of raw materials scarcity in a fast-growing world, leading to long positions taken on those markets, such as Chinese increasing presence in Africa. An increase in oil prices tends to divert a larger share of consumer spending into gasoline, which creates downward pressure on economic growth in oil importing countries, as wealth flows to oil-producing states.[160] A pattern of spiking instability in the price of oil over the decade leading up to the price high of 2008 has been recently identified.[161] The destabilizing effects of this price variance has been proposed as a contributory factor in the financial crisis.

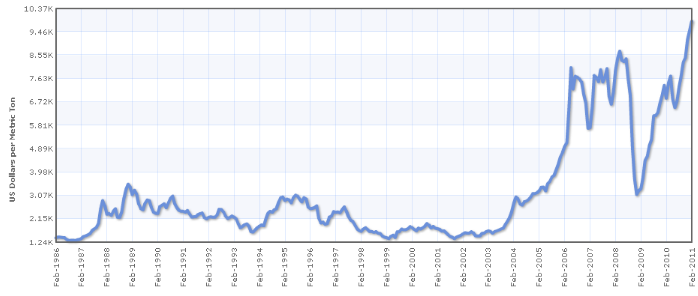

Copper prices increased at the same time as oil prices. Copper traded at about $2,500 per ton from 1990 until 1999, when it fell to about $1,600. The price slump lasted until 2004, when a price surge pushed copper to $7,040 per ton in 2008.[162]

Nickel prices boomed in the late 1990s, then declined from around $51,000 /£36,700 per metric ton in May 2007 to about $11,550/£8,300 per metric ton in January 2009. Prices were only just starting to recover as of January 2010, but most of Australia's nickel mines had gone bankrupt by then.[163] As the price for high grade nickel sulphate ore recovered in 2010, so did the Australian nickel mining industry.[164]

Coincidentally with these price fluctuations, long-only commodity index funds became popular—by one estimate investment increased from $90 billion in 2006 to $200 billion at the end of 2007, while commodity prices increased 71% – which raised concern as to whether these index funds caused the commodity bubble.[165] The empirical research has been mixed.[165]

2.12. Systemic Crisis

Another analysis is that the financial crisis was merely a symptom of another, deeper crisis, which is a systemic crisis of capitalism itself.[166]

Ravi Batra's theory is that growing inequality of financial capitalism produces speculative bubbles that burst and result in depression and major political changes. He has also suggested that a "demand gap" related to differing wage and productivity growth explains deficit and debt dynamics important to stock market developments.[167]

John Bellamy Foster, a political economy analyst and editor of the Monthly Review, believes that the decrease in GDP growth rates since the early 1970s is due to increasing market saturation.[168]

The conventional Marxist explanation of capitalist crises was pointed to by economists Andrew Kliman, Michael Roberts, and Guglielmo Carchedi, in contradistinction to the Monthly Review school represented by Foster. These Marxist economists do not point to low wages or underconsumption as the cause of the crisis, but instead point to capitalism's long-term tendency of the rate of profit to fall as the underlying cause of crises generally. From this point of view, the problem was the inability of capital to grow or accumulate at sufficient rates through productive investment alone. Low rates of profit in productive sectors led to speculative investment in riskier assets, where there was potential for greater return on investment. The speculative frenzy of the late 90s and 2000s was, in this view, a consequence of a rising organic composition of capital, expressed through the fall in the rate of profit. According to Michael Roberts, the fall in the rate of profit "eventually triggered the credit crunch of 2007 when credit could no longer support profits".[169]

In 2005, John C. Bogle wrote that a series of challenges face capitalism that have contributed to past financial crises and have not been sufficiently addressed:

Corporate America went astray largely because the power of managers went virtually unchecked by our gatekeepers for far too long ... . They failed to 'keep an eye on these geniuses' to whom they had entrusted the responsibility of the management of America's great corporations.

Echoing the central thesis of James Burnham's 1941 seminal book, The Managerial Revolution, Bogle cites particular issues, including:[170]

- that "Manager's capitalism" has replaced "owner's capitalism", meaning management runs the firm for its benefit rather than for the shareholders, a variation on the principal–agent problem;

- the burgeoning executive compensation;

- the management of earnings, mainly a focus on share price rather than the creation of genuine value; and

- the failure of gatekeepers, including auditors, boards of directors, Wall Street analysts, and career politicians.

An analysis conducted by Mark Roeder, a former executive at the Swiss-based UBS Bank, suggested that large-scale momentum, or The Big Mo "played a pivotal role" in the 2008–09 global financial crisis. Roeder suggested that "recent technological advances, such as computer-driven trading programs, together with the increasingly interconnected nature of markets, has magnified the momentum effect. This has made the financial sector inherently unstable."[171]

Robert Reich attributes the current economic downturn to the stagnation of wages in the United States, particularly those of the hourly workers who comprise 80% of the workforce. He says this stagnation forced the population to borrow to meet the cost of living.[172]

Economists Ailsa McKay and Margunn Bjørnholt argue that the financial crisis and the response to it revealed a crisis of ideas in mainstream economics and within the economics profession, and call for a reshaping of both the economy, economic theory and the economics profession.[173]

2.13. Role of Economic Forecasting

The financial crisis was not widely predicted by mainstream economists.

A cover story in BusinessWeek magazine claims that economists mostly failed to predict the worst international economic crisis since the Great Depression of the 1930s.[174] The Wharton School of the University of Pennsylvania's online business journal examines why economists failed to predict a major global financial crisis.[175] Popular articles published in the mass media have led the general public to believe that the majority of economists have failed in their obligation to predict the financial crisis. For example, an article in the New York Times informs that economist Nouriel Roubini warned of such crisis as early as September 2006, and the article goes on to state that the profession of economics is bad at predicting recessions.[176] According to The Guardian , Roubini was ridiculed for predicting a collapse of the housing market and worldwide recession, while The New York Times labelled him "Dr. Doom".[177]

Within mainstream financial economics, most believe that financial crises are simply unpredictable,[178] following Eugene Fama's efficient-market hypothesis and the related random-walk hypothesis, which state respectively that markets contain all information about possible future movements, and that the movements of financial prices are random and unpredictable. Recent research casts doubt on the accuracy of "early warning" systems of potential crises, which must also predict their timing.[179]

The Austrian economic school regarded the crisis as a vindication and classic example of a predictable credit-fueled bubble caused by laxity in monetary supply.[180]

A number of heterodox economists predicted the crisis, with varying arguments. Dirk Bezemer in his research[181] credits (with supporting argument and estimates of timing) 12 economists with predicting the crisis: Dean Baker (US), Wynne Godley (UK), Fred Harrison (UK), Michael Hudson (US), Eric Janszen (US), Steve Keen (Australia), Jakob Brøchner Madsen & Jens Kjaer Sørensen (Denmark), Med Jones (US) [182] Kurt Richebächer (US), Nouriel Roubini (US), Peter Schiff (US), and Robert Shiller (US). Examples of other experts who gave indications of a financial crisis have also been given.[183][184][185] Shiller, an expert in housing markets, wrote an article a year before the collapse of Lehman Brothers in which he predicted that a slowing US housing market would cause the housing bubble to burst, leading to financial collapse.[186] Schiff regularly appeared on television in the years before the crisis and warned of the impending real estate collapse.[187]

Karim Abadir, based on his work with Gabriel Talmain,[188] predicted the timing of the recession[189] whose trigger had already started manifesting itself in the real economy from early 2007.[190]

The former Governor of the Reserve Bank of India, Raghuram Rajan, had predicted the crisis in 2005 when he became chief economist at the International Monetary Fund. In 2005, at a celebration honoring Alan Greenspan, who was about to retire as chairman of the US Federal Reserve, Rajan delivered a controversial paper that was critical of the financial sector.[191] In that paper, Rajan "argued that disaster might loom".[192] Rajan argued that financial sector managers were encouraged to "take risks that generate severe adverse consequences with small probability but, in return, offer generous compensation the rest of the time. These risks are known as tail risks. But perhaps the most important concern is whether banks will be able to provide liquidity to financial markets so that if the tail risk does materialize, financial positions can be unwound and losses allocated so that the consequences to the real economy are minimized."

Stock trader and financial risk engineer Nassim Nicholas Taleb, author of the 2007 book The Black Swan, spent years warning against the breakdown of the banking system in particular and the economy in general owing to their use of and reliance on bad risk models and reliance on forecasting, and framed the problem as part of "robustness and fragility".[193][194] He also took action against the establishment view by making a big financial bet on banking stocks and making a fortune from the crisis ("They didn't listen, so I took their money").[195] According to David Brooks from the New York Times, "Taleb not only has an explanation for what's happening, he saw it coming."[196]

2.14. Wrong Banking Model

A report by the International Labour Organization concluded that cooperative financial institutions were less likely to fail than their competitors during the crisis. The cooperative banking sector had 20% market share of the European banking sector, but accounted for only 7 per cent of all the write-downs and losses between the third quarter of 2007 and first quarter of 2011.[197] Similarly, credit unions in the US had five times lower failure rate than other banks during the crisis[198] and increased their lending to small- and medium-sized businesses while overall lending to those businesses decreased.[199]

3. Impact on Financial Markets

3.1. US Stock Market

The US stock market peaked in October 2007, when the Dow Jones Industrial Average index exceeded 14,000 points. It then entered a pronounced decline, which accelerated markedly in October 2008. By March 2009, the Dow Jones average had reached a trough of around 6,600. Four years later, it hit an all-time high. It is probable, but debated, that the Federal Reserve's aggressive policy of quantitative easing spurred the partial recovery in the stock market.[200][201][202]

Market strategist Phil Dow believes distinctions exist "between the current market malaise" and the Great Depression. He says the Dow Jones average's fall of more than 50% over a period of 17 months is similar to a 54.7% fall in the Great Depression, followed by a total drop of 89% over the following 16 months. "It's very troubling if you have a mirror image," said Dow.[203] Floyd Norris, the chief financial correspondent of The New York Times , wrote in a blog entry in March 2009 that the decline has not been a mirror image of the Great Depression, explaining that although the decline amounts were nearly the same at the time, the rates of decline had started much faster in 2007, and that the past year had only ranked eighth among the worst recorded years of percentage drops in the Dow. The past two years ranked third, however.[204]

3.2. Financial Institutions

The first notable event signaling a possible financial crisis occurred in the United Kingdom on August 9, 2007, when BNP Paribas, citing "a complete evaporation of liquidity", blocked withdrawals from three hedge funds. The significance of this event was not immediately recognized but soon led to a panic as investors and savers attempted to liquidate assets deposited in highly leveraged financial institutions.[5]

The International Monetary Fund estimated that large US and European banks lost more than $1 trillion on toxic assets and from bad loans from January 2007 to September 2009. These losses are expected to top $2.8 trillion from 2007 to 2010. US bank losses were forecast to hit $1 trillion and European bank losses will reach $1.6 trillion. The International Monetary Fund (IMF) estimated in 2009 that US banks were about 60% through their losses, but British and eurozone banks only 40%.[205]

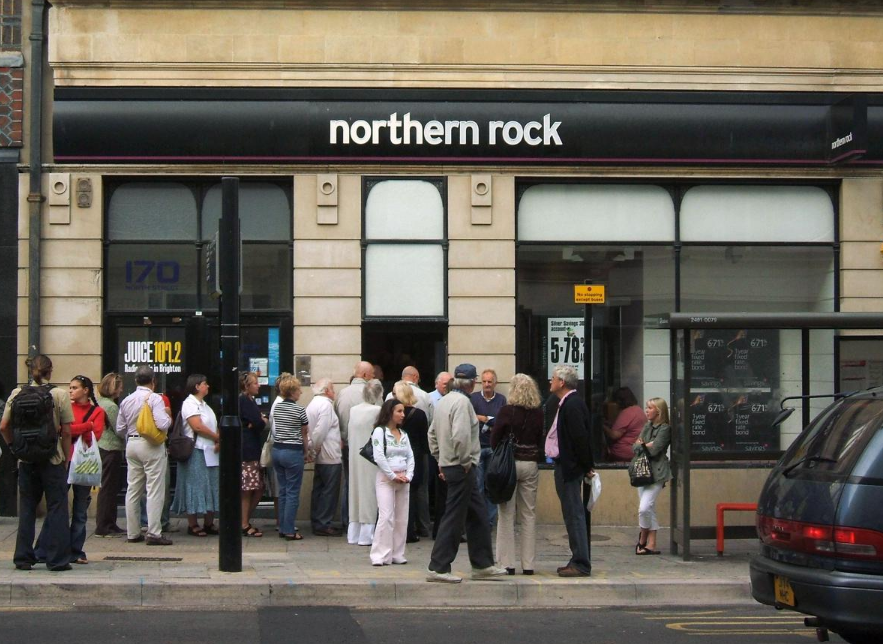

One of the first victims was Northern Rock, a medium-sized British bank.[206] The highly leveraged nature of its business led the bank to request security from the Bank of England. This in turn led to investor panic and a bank run[207] in mid-September 2007. Calls by Liberal Democrat Treasury Spokesman Vince Cable to nationalise the institution were initially ignored; in February 2008, however, the British government (having failed to find a private sector buyer) relented, and the bank was taken into public hands. Northern Rock's problems proved to be an early indication of the troubles that would soon befall other banks and financial institutions.

4. IndyMac

The first visible institution to run into trouble in the United States was the Southern California–based IndyMac, a spin-off of Countrywide Financial. Before its failure, IndyMac Bank was the largest savings and loan association in the Los Angeles market and the seventh largest mortgage originator in the United States.[208] The failure of IndyMac Bank on July 11, 2008, was the fourth largest bank failure in United States history up until the crisis precipitated even larger failures,[209] and the second largest failure of a regulated thrift.[210] IndyMac Bank's parent corporation was IndyMac Bancorp until the FDIC seized IndyMac Bank.[211] IndyMac Bancorp filed for Chapter 7 bankruptcy in July 2008.[211]

IndyMac Bank was founded as Countrywide Mortgage Investment in 1985 by David S. Loeb and Angelo Mozilo[212][213] as a means of collateralizing Countrywide Financial loans too big to be sold to Freddie Mac and Fannie Mae. In 1997, Countrywide spun off IndyMac as an independent company run by Mike Perry, who remained its CEO until the downfall of the bank in July 2008.[214]

The primary causes of its failure were largely associated with its business strategy of originating and securitizing Alt-A loans on a large scale. This strategy resulted in rapid growth and a high concentration of risky assets. From its inception as a savings association in 2000, IndyMac grew to the seventh largest savings and loan and ninth largest originator of mortgage loans in the United States. During 2006, IndyMac originated over $90 billion of mortgages.

IndyMac's aggressive growth strategy, use of Alt-A and other nontraditional loan products, insufficient underwriting, credit concentrations in residential real estate in the California and Florida markets—states, alongside Nevada and Arizona, where the housing bubble was most pronounced—and heavy reliance on costly funds borrowed from a Federal Home Loan Bank (FHLB) and from brokered deposits, led to its demise when the mortgage market declined in 2007.

IndyMac often made loans without verification of the borrower's income or assets, and to borrowers with poor credit histories. Appraisals obtained by IndyMac on underlying collateral were often questionable as well. As an Alt-A lender, IndyMac's business model was to offer loan products to fit the borrower's needs, using an extensive array of risky option-adjustable-rate-mortgages (option ARMs), subprime loans, 80/20 loans, and other nontraditional products. Ultimately, loans were made to many borrowers who simply could not afford to make their payments. The thrift remained profitable only as long as it was able to sell those loans in the secondary mortgage market. IndyMac resisted efforts to regulate its involvement in those loans or tighten their issuing criteria: see the comment by Ruthann Melbourne, Chief Risk Officer, to the regulating agencies.[215][216][217]

May 12, 2008, in a small note in the "Capital" section of its what would become its last 10-Q released before receivership, IndyMac revealed—but did not admit—that it was no longer a well-capitalized institution and that it was headed for insolvency.

IndyMac reported that during April 2008, Moody's and Standard & Poor's downgraded the ratings on a significant number of Mortgage-backed security (MBS) bonds—including $160 million issued by IndyMac that the bank retained in its MBS portfolio. IndyMac concluded that these downgrades would have harmed the Company's risk-based capital ratio as of June 30, 2008. Had these lowered ratings been in effect at March 31, 2008, IndyMac concluded that the bank's capital ratio would have been 9.27% total risk-based. IndyMac warned that if its regulators found its capital position to have fallen below "well capitalized" (minimum 10% risk-based capital ratio) to "adequately capitalized" (8–10% risk-based capital ratio) the bank might no longer be able to use brokered deposits as a source of funds.

Senator Charles Schumer (D-NY) later pointed out that brokered deposits made up more than 37 percent of IndyMac's total deposits, and ask the Federal Deposit Insurance Corporation (FDIC) whether it had considered ordering IndyMac to reduce its reliance on these deposits.[218] With $18.9 billion in total deposits reported on March 31,[219] Senator Schumer would have been referring to a little over $7 billion in brokered deposits. While the breakout of maturities of these deposits is not known exactly, a simple averaging would have put the threat of brokered deposits loss to IndyMac at $500 million a month, had the regulator disallowed IndyMac from acquiring new brokered deposits on June 30.

IndyMac was taking new measures to preserve capital, such as deferring interest payments on some preferred securities. Dividends on common shares had already been suspended for the first quarter of 2008, after being cut in half the previous quarter. The company still had not secured a significant capital infusion nor found a ready buyer.[220][221]

IndyMac reported that the bank's risk-based capital was only $47 million above the minimum required for this 10% mark. But it did not reveal some of that $47 million capital it claimed it had, as of March 31, 2008, was fabricated.

4.1. Collapse

When home prices declined in the latter half of 2007 and the secondary mortgage market collapsed, IndyMac was forced to hold $10.7 billion of loans it could not sell in the secondary market. Its reduced liquidity was further exacerbated in late June 2008 when account holders withdrew $1.55 billion or about 7.5% of IndyMac's deposits.[222] This "run" on the thrift followed the public release of a letter from Senator Charles Schumer to the FDIC and OTS. The letter outlined the Senator's concerns with IndyMac. While the run was a contributing factor in the timing of IndyMac's demise, the underlying cause of the failure was the unsafe and unsound way they operated the thrift.[215]

On June 26, 2008, Senator Charles Schumer (D-NY), a member of the Senate Banking Committee, chairman of Congress' Joint Economic Committee and the third-ranking Democrat in the Senate,[223] released several letters he had sent to regulators, which warned that, "The possible collapse of big mortgage lender IndyMac Bancorp Inc. poses significant financial risks to its borrowers and depositors, and regulators may not be ready to intervene to protect them." Some worried depositors began to withdraw money.[224]

On July 7, 2008, IndyMac announced on the company blog that it:

- Had failed to raise capital since its May 12, 2008 quarterly earnings report;

- Had been notified by bank and thrift regulators that IndyMac Bank was no longer deemed "well-capitalized";

IndyMac announced the closure of both its retail lending and wholesale divisions, halted new loan submissions, and cut 3,800 jobs.[225]