Green finance is a sustainable force in promoting green development. China’s social financing structure determines the key role that green credit plays in sustainable development. Under the dual pressure of future economic downturn and huge capital gaps, it is worth exploring whether to continue promoting green credit that conforms to the long-term market mechanism.

- green credit

- “Two High and One Surplus”

- financial results

1. Introduction

2. Related Content of Green Finance in Line with the Long-Term Market Mechanism

3. Financial Comparison between “Green” and “Two High and One Surplus”Enterprises

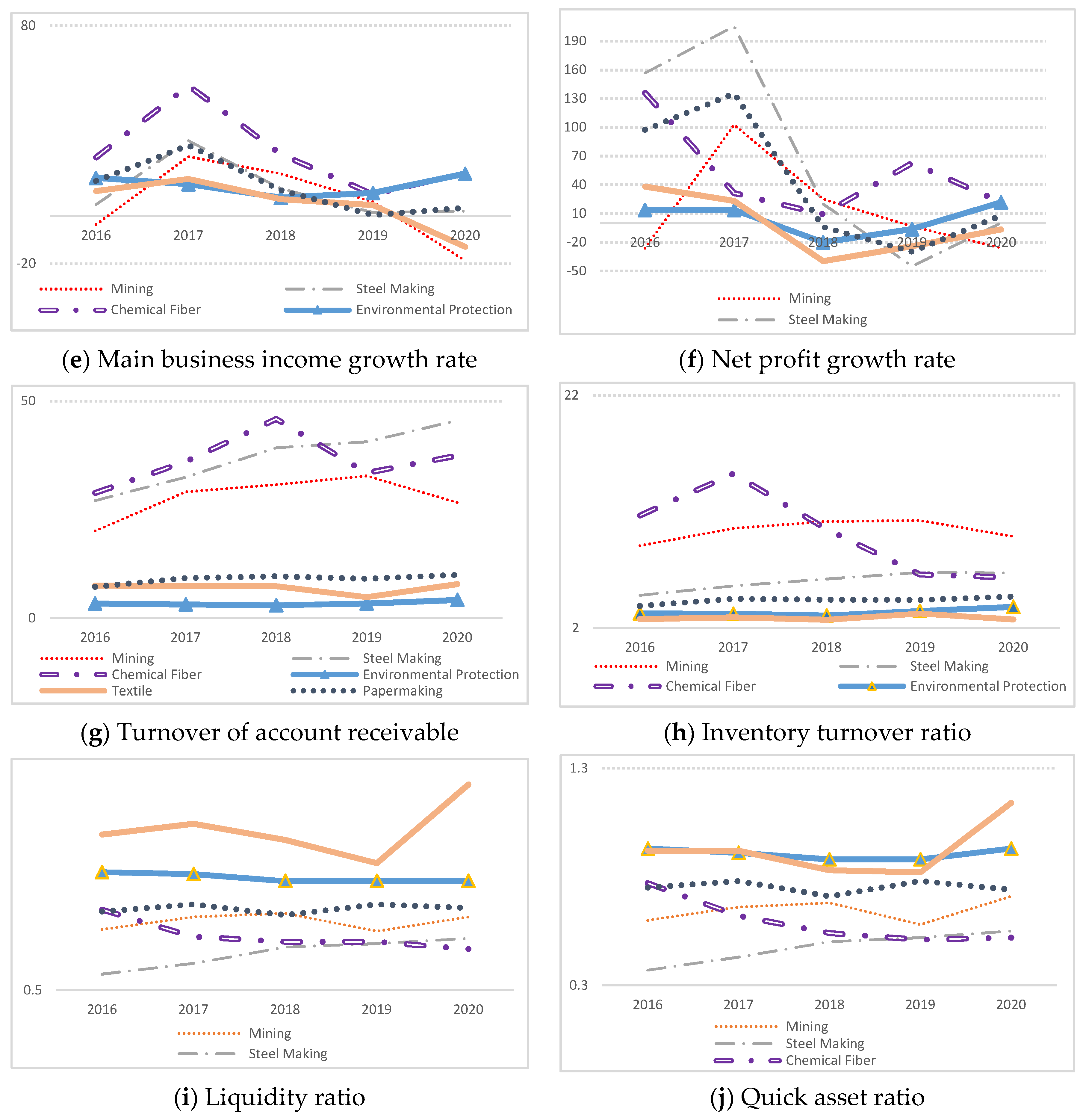

The main purpose of green credit policies is not only to increase the proportion of credit for green projects, but also to reduce the loans to “Two High and One Surplus” enterprises. Changing the credit structure of commercial banks is reflected in the proportion of these two types of corporate loans. Financial analysis is the most important link in the loan approval process of commercial banks. According to the financial analysis , it was found that, compared to the “Two High and One Surplus” industries, the environmental protection industry is better, but its financing costs are high (Figures 1-3).

Figure 1. Financial comparison between green industries and the “Two High and One Surplus” industries.

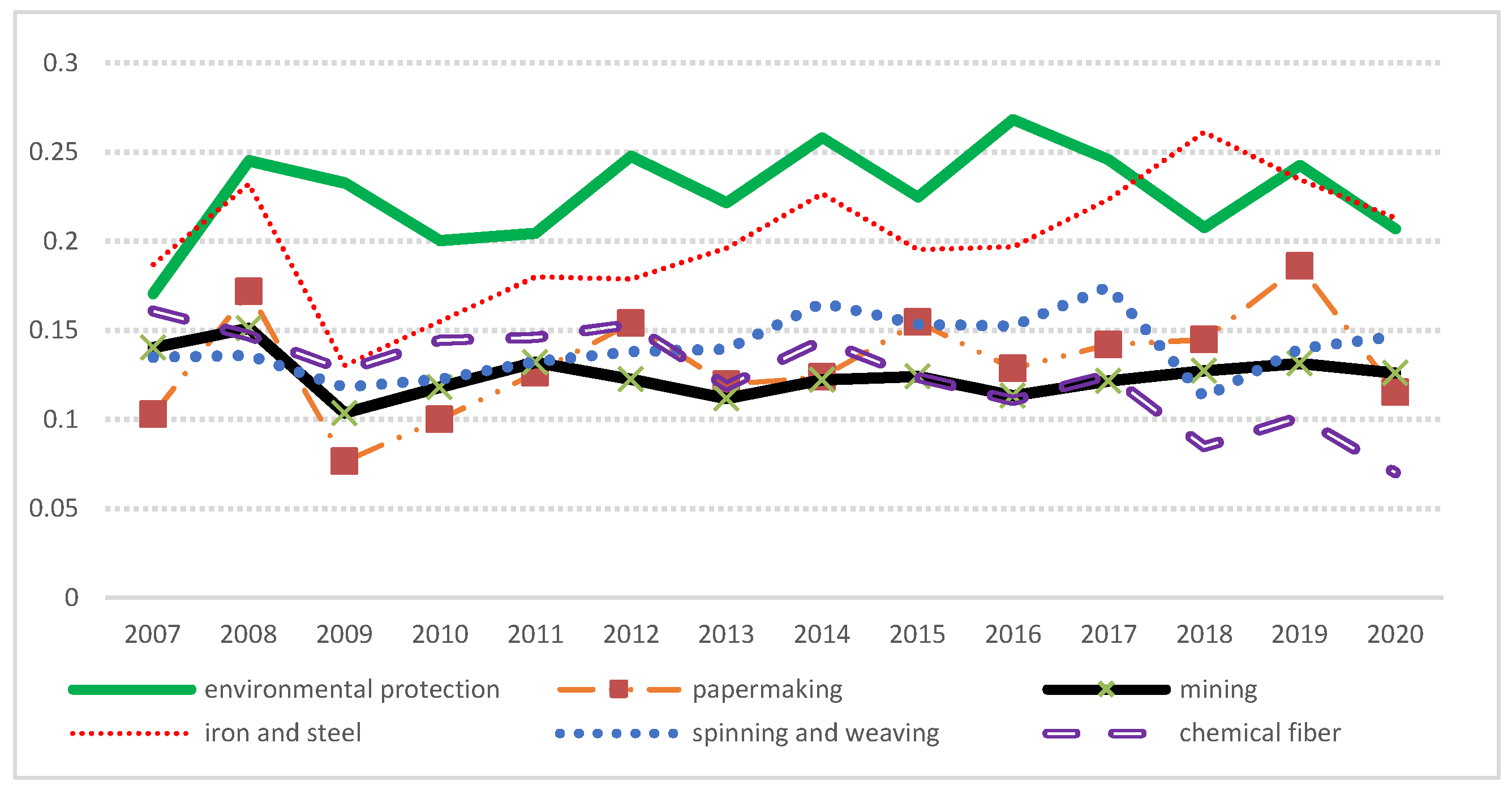

Figure 1. Financial comparison between green industries and the “Two High and One Surplus” industries. Figure 2. Interest-bearing debt interest rate: environmental protection industry and “Two High and One Surplus” industries.

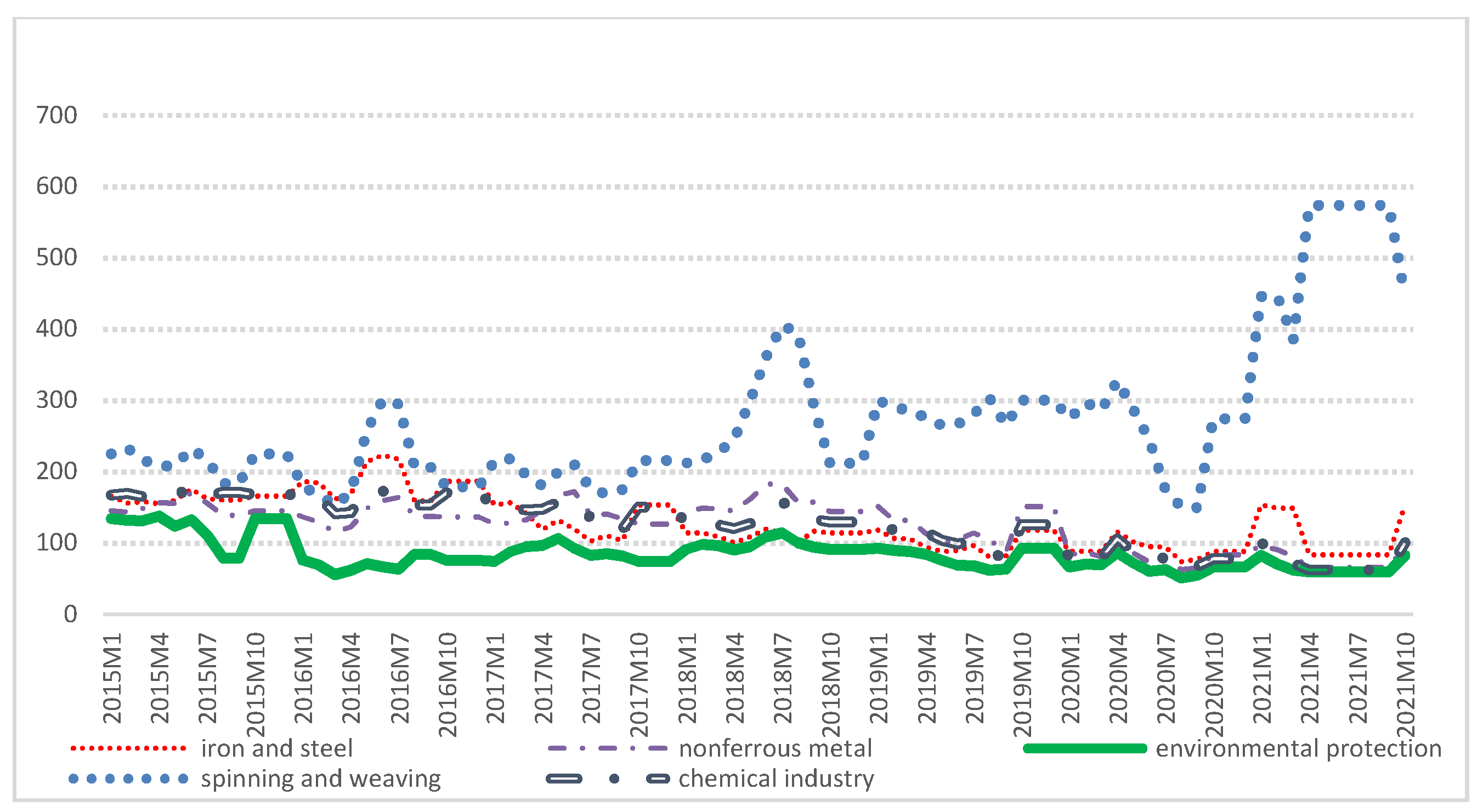

Figure 2. Interest-bearing debt interest rate: environmental protection industry and “Two High and One Surplus” industries. Figure 3. Credit spread (median): industrial debt.

Figure 3. Credit spread (median): industrial debt.4. Do Green Credit Policies Boost Profits?

This section analyzes the influence of green credit ratio on the financial indicators of Chinese commercial banks through regression method. It is pointed out that the differences in conclusions from the literature are due to the selection of model variables. The root cause of these differences may be the rapid expansion of the capital of commercial banks in the sample period, resulting in a decline in the internal factor allocation efficiency. The empirical analysis proves that increasing the green credit ratio can increase the total profits of commercial banks and puts forward that green credit policies can solve the “overcapacity” problems that are experienced by commercial banks to a certain extent.

5. Green Credit and Bank Operating Efficiency

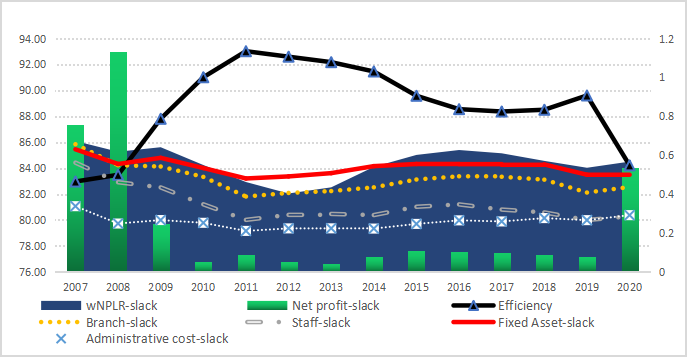

Section 5 analyzes the allocation efficiency of the internal resources of commercial banks from the perspective of input–output efficiency to prepare for the fourth part of the research. In terms of methods, an SBM-DEA model containing undesirable output (the non-performing loan ratio) was established, and the weights of the output variables were innovatively and dynamically coordinated. The results (Figure 4) show that the efficiency measurements for China's commercial banks largely conform to the economic reality, and the analysis of the slack variables effectively revealed the main reasons for the changes in the operating efficiency of commercial banks at various stages.

Figure 4. Average operating efficiency and slack variables.

Through regression analysis, it is found that green credit policies mainly improve the overall operating efficiency of commercial banks from two aspects: (1) it improves the utilization efficiency of various internal resources, and (2) it improves the overall allocation efficiency of resources.

This entry is adapted from the peer-reviewed paper 10.3390/math10091374

References

- BP. Statistical Review of World Energy 2021, 70th ed.; BP: London, UK, 2021.

- Ma, J. The Evolution of and Prospect for Green Finance in China. Comp. Econ. Soc. Syst. 2016, 6, 25–32.

- Sequoiacap. Towards Zero Carbon—A Green Revolution Based on Scientific and Technological Innovation; Sequoiacap: London, UK, 2021.

- Zhou, L.A. The Incentive and Cooperation of Government Officials in the Political Tournaments an Interpretation of the Prolonged Local: Protectionism and Duplicative Investments in China. Econ. Res. J. 2004, 6, 33–40.

- Jiang, F.; Cao, J. Market Failure or Institutional Weakness—The Argument, Defect and New Development in Research of Redundant Construction Formation Mechanism. China Ind. Econ. 2009, 1, 53–64.

- Jiang, F.; Geng, Q.; Lv, D.; Li, X. Mechanism of Excess Capacity Based on China’s Regional Competition and Market Distortion. China Ind. Econ. 2012, 6, 44–56.

- Zhang, J. Research on the formation and resolution of Overcapacity in China from the perspective of industrial policy. Inq. Econ. Issues 2015, 2, 10–14.

- Dong, Q.; Wen, S.; Liu, X. Credit Allocation, Pollution, and Sustainable Growth: Theory and Evidence from China. Emerg. Mark. Financ. Trade 2019, 56, 2793–2811.

- Liu, X.; Wen, S. Should Financial Institutions be Environmentally Responsible in China? Facts, Theory and Evidence. Econ. Res. J. 2019, 54, 38–54.

- Ma, L.; Zhang, X. The Spatial Effect of China’s Haze Pollution and the Impact from Economic Change and Energy Structure. China Ind. Econ. 2014, 4, 19–31.

- Wang, M.; Huang, Y. China’s Environmental Pollution and Economic Growth. China Econ. Q. 2015, 14, 557–578.

- Deng, Y. Build “green Credit” for enterprise energy saving and emission reduction. Shanghai Securities News, 20 July 2007.

- Wang, X.; Wang, Y. Research on the Green Innovation Promoted by Green Credit Policies. Manag. World 2021, 37, 173–188+11.

- United Nations Environment Programme Finance Initiative. UNEP Statement by Financial Institutions on the Environment & Sustainable Development; United Nations Environment Programme Finance Initiative: Geneva, Switzerland, 1997.

- Boyreau-Debray, G.; Wei, S.J. Pitfalls of a State-Dominated Financial System: The Case of China; Social Science Electronic Publishing: New York, NY, USA, 2004.

- Shao, T. Financial mismatch, Ownership structure and Return on capital: A study of Chinese industrial firms from 1999 to 2007. J. Financ. Res. 2010, 9, 51–68.

- Berger, A.N.; Hasan, I.; Zhou, M. Bank ownership and efficiency in China: What will happen in the world’s largest nation? J. Bank. Financ. 2009, 33, 113–130.

- Garcia-Herrero, A.; Gavila, S.; Santabarbara, D. What explains the low profitability of Chinese banks? J. Bank. Financ. 2009, 33, 2080–2092.

- Ma, J.; Wu, B. Floating interest rate policy differential pricing strategy and credit rationing for farmers by financial institutions. J. Financ. Res. 2012, 4, 155–168.

- Zhan, M.; Wang, X.; Ying, C. Interest Rate Regulation, Behavior Distortion of Banks’ Credit Allocation and the Financial Restriction of China’s Listed Companies. China Econ. Q. 2013, 12, 1255–1276.

- Zhang, X.; Ge, J. Green finance policies and optimization of resources allocation efficiency in China. Ind. Econ. Res. 2021, 6, 15–28.

- Wang, L.; Xu, J.; Li, C. The Mechanism and Stage Evolution of Green Financial Policy Promoting Enterprise Innovation. Soft Sci. 2021, 12, 81–87.

- Chen, W.; Hu, D. An Analysis of the Functional Mechanism and Effect of Green Credit on Industrial Upgrading. J. Jiangxi Univ. Financ. Econ. 2011, 4, 12–20.

- Qiang, X.; Fang, S. Does Reform on Security Interests System Affect Corporate Debt Financing? Evidence from a Natural Experiment in China. Econ. Res. J. 2017, 5, 146–160.

- Lu, J.; Yan, Y.; Wang, T. The Microeconomic Effects of Green Credit Policy—From the Perspective of Technological Innovation and Resource Reallocation. China Ind. Econ. 2021, 1, 174–192.

- Sun, J.; Wang, F.; Yin, H.; Zhang, B. Money Talks: The Environmental Impact of China’s Green Credit Policy. J. Policy Anal. Manag. 2019, 38, 653–680.

- Shen, X. The Research on Green-Credit, Green Reputation and Financial Performance of Commercial Banks; Nanjing University of Finance and Economics: Nanjing, China, 2011; p. 47.

- Chami, R.; Cosimano, T.F.; Fullenkamp, C. Managing ethical risk: How investing in ethics adds value. J. Bank. Financ. 2002, 26, 1697–1718.

- Thompson, P.; Cowton, C.J. Bringing the environment into bank lending: Implications for environmental reporting. Br. Account. Rev. 2004, 36, 197–218.

- Aintablian, S.; Mcgraw, P.A.; Roberts, G.S. Bank monitoring and environmental risk. J. Bus. Financ. Account. 2007, 34, 389–401.

- Zhou, Y.; Luo, Y. Financial ecological environment, green reputation and credit financing: An empirical study of A-share heavily polluting listed companies. South China Financ. 2017, 8, 21–32.

- The Study Group of Green Finance, ICBC. A Study of ESG Green Rating and Green Index. Financ. Forum 2017, 22, 3–14.

- Guo, W.; Liu, Y. Green Credit, Cost-Benefit Effect and Profitability of Commercial Banks. South China Financ. 2019, 9, 40–50.

- Zhang, L.; Lian, Y. How Does Green Credit Affect the Financial Performance of Commercial Banks? From the Perspective of Income Structure Decomposition of Banks. South China Financ. 2020, 2, 45–56.

- Tong, M. Early Warning Research on Carbon Emission Reduction Credit Risk of Industrial Enterprises Based on FM Model. J. Quant. Tech. Econ. 2021, 38, 147–165.

- He, L.; Wu, C.; Zhong, Z.; Zhu, J. Green Credit, Internal and External Policies, and the Competitiveness of Commercial Banks: An Empirical Study of Nine Listed Commercial Banks. Financ. Econ. Res. 2018, 33, 91–103.

- Gao, X.; Gao, G. A Study on the Relation between the Scale of Green Credit and the Competitiveness of Commercial Banks. Econ. Probl. 2018, 7, 15–21.

- Ma, Y.; Du, C. Are Equator Principles Conductive to the Operational Efficiency of China’s commercial Banks? With Industrial Bank as a Case. Contemp. Financ. Econ. 2015, 7, 57–65.

- Liao, J.; Hu, W.; Yang, D. Dynamic Analysis of the Effect of Green Credit on Bank Operating Efficiency—Based on Panel VAR Model. Collect. Essays Financ. Econ. 2019, 2, 57–64.