Your browser does not fully support modern features. Please upgrade for a smoother experience.

Submitted Successfully!

+1 credit

+1 credit

Thank you for your contribution! You can also upload a video entry or images related to this topic.

For video creation, please contact our Academic Video Service.

| Version | Summary | Created by | Modification | Content Size | Created at | Operation |

|---|---|---|---|---|---|---|

| 1 | Nanja Kroon | + 2018 word(s) | 2018 | 2021-06-30 08:16:34 | | | |

| 2 | Nanja Kroon | -21 word(s) | 1997 | 2021-06-30 11:48:08 | | | | |

| 3 | Bruce Ren | Meta information modification | 1997 | 2021-07-01 08:08:45 | | |

Video Upload Options

We provide professional Academic Video Service to translate complex research into visually appealing presentations. Would you like to try it?

Cite

If you have any further questions, please contact Encyclopedia Editorial Office.

Kroon, N. Emerging Technologies on Accountants. Encyclopedia. Available online: https://encyclopedia.pub/entry/11527 (accessed on 25 July 2026).

Kroon N. Emerging Technologies on Accountants. Encyclopedia. Available at: https://encyclopedia.pub/entry/11527. Accessed July 25, 2026.

Kroon, Nanja. "Emerging Technologies on Accountants" Encyclopedia, https://encyclopedia.pub/entry/11527 (accessed July 25, 2026).

Kroon, N. (2021, June 30). Emerging Technologies on Accountants. In Encyclopedia. https://encyclopedia.pub/entry/11527

Kroon, Nanja. "Emerging Technologies on Accountants." Encyclopedia. Web. 30 June, 2021.

Copy Citation

This paper reviews the recent accounting literature focusing on emerging technologies’ impacts on accountants’ role and skills. Specifically, it determines what emerging technologies are most studied concerning their impacts on accountants’ role and skills, which research strategies are used in the studies that focus on this theme, and the impacts of the identified emerging technologies on accountants’ skills. It also investigates whether open innovation is an influencing factor in this connection.

accountant

accounting

artificial intelligence

big data

blockchain

emerging technologies

skills

open innovation

1. Introduction

Emerging technologies are transforming the everyday work of accountants, impacting the professional life of millions of people worldwide. This phenomenon is more and more evident with the increasing speed of technological innovations. Changes have been caused by several factors, including rapid technological developments, more globalized and easily facilitated communication via the internet, and legislative and regulatory changes.

Until 2010, information and communication technologies were clearly the most critical factor, continuously improving, and reducing time and distances [1]. These improvements have made it widely possible to share knowledge and ideas in an expanding universe, giving rise to the concept of open innovation [2]. In his seminal work on open innovation, Chesbrough [3] argues that managers must rethink how they seek to create and profit from technological innovation. He contends that “open” innovation is the key to success. It is important to note that emerging technologies bring their own set of challenges that can best be overcome through the notion of open innovation [4]. In reality, current events place a high value on open innovation since the integration of external knowledge is more important than ever to boost innovation within the organization [5].

Technological changes related to accounting have been widely studied recently [6][7][8][9], presenting accounting challenges for which future technological responses are still expected. In the same vein, studies have emerged approaching the new role and skills of accountants, many of them in the blockchain area. Blockchain technology will require a new generation of accounting professionals with skills to operate in the new blockchain environment [10][11]. Auditors’ role will change after blockchain implementation, as internal control will be maintained, although its focus may be different or performed differently [12].

Accountants have always been very open to adopting new technologies [13], yet accounting technologies’ radical potential can only be fully realized with a similarly profound accounting revolution in thought. Emerging technologies may have the potential to dramatically change and disrupt the work of accountants and accounting researchers [14], but it is not enough to evolve new technologies if there is no parallel development of new paradigms that allow the understanding of new data or ways of working [15].

Professional accounting bodies have responded to these challenges by developing competency frameworks [16][17] and reports on future careers in accountancy [18] to cope with these changes, to face predictable difficulties, and to seize presumable opportunities. Accounting work as we know it must be prepared to face an abundance of changes in the coming years due to these emerging technologies, and these changes can be disruptive, but at the same time open up many potential opportunities in the profession [19]. Overall, the main concern is how careers in the profession will adapt and how skills will transform.

The AACSB 2018 accounting accreditation standard A5 expects the development of knowledge and skills related to the integration of information technologies in accounting graduate programs. It specifically mentions “the ability of both faculty and students to adapt to emerging technologies as well as the mastery of current technology” [20] (p. 27). Thus, it becomes clear that technology and emerging technologies are relevant both for (the future of) students and for the accounting profession [21].

Although some recent studies link some sort of (emergent) technology to the accounting profession, there is still a call for further research regarding the impacts of digitalization [10][12][22]. Some related literature reviews have been published, linking digital transformation or specific technologies (blockchain) to the accounting profession [10][22][23][24], or investigating changes in the management accountants’ role, related or not to technology [25][26]. However, to our knowledge, the link between emerging technologies and accountants’ role and skills has not yet been made.

Therore, to ascertain the current research situation, the main objective of this paper is to assess the accounting and information systems literature, focused on four aspects: (1) understanding how emerging technologies are transforming the everyday work of accountants; (2) what this means for today’s accountants’ role; (3) what skills are they expected to have; and (4) what is the connection between open innovation and the transformation mentioned above. Thus, the literature analysis is guided by the broader research question: What are the impacts of emerging technologies on accountants’ role and skills?

In particular, four research sub-questions are addressed:

-

Which emerging technology is most often studied concerning its impacts on accountants’ role and skills?

-

What research strategies are being used to identify emerging technologies’ impacts on accountants’ role or skills?

-

Is open innovation an influencing factor connecting emerging technologies and accountants’ role and skills?

-

What are the most commonly identified impacts of emerging technologies on accountants’ role and skills?

This work will answer these sub-questions by systematically reviewing the recent literature, following the five-step approach of a systematic literature review, as described by Denyer and Tranfield [27]: (1) formulate the research questions; (2) locate studies; (3) select and assess these studies; (4) analyze and synthesize; and (5) report and use the results.

As for delimiting concepts in accounting and emerging technologies, we identified convenient categories as follows, developed largely based on the topical area classifications in Coyne et al. [28]—auditing, financial, managerial, accounting information systems (AIS), tax, and ‘others’. As the categories of AIS and tax did not return a relevant number of articles, these were included in ‘others’.

When approaching emerging technologies, we focus on research that connects the concept of emerging technology with impacts on the accounting profession, which helps us limit our search. Nevertheless, we found a study by Abad-Segura and González-Zamar [29], who analyzed the research on emerging technologies in corporate accounting from 1961–2019. They identified the main terms recently associated with new technology and digitalization related to accounting as big data, blockchain, social media, and artificial intelligence.

2. Discussion of Results and Implications

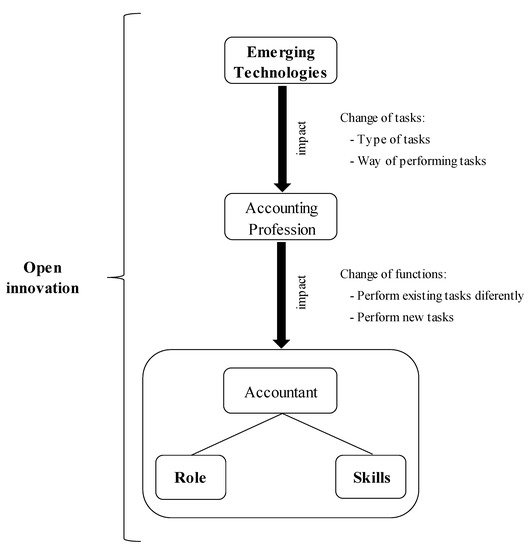

It arises from the analysis of the results that emerging technologies’ impact on the accountants’ role and skills is not direct. Figure 1 represents the way emerging technologies impact the role and skills of accountants.

Figure 1. How do emerging technologies impact accountants’ role and skills?

The first impact on the accounting profession will be changing tasks or the way they are performed. These changes may impact accountants’ functions; they may have to complete existing tasks differently or even perform new tasks. As the accountant’s role is closely related to the tasks performed and the functions assumed, all these changes may ultimately affect the accountant’s role. Similarly, the skills needed by accountants to perform their profession may also be affected.

2.1. Opportunities, Challenges, and Risks

The opportunities created by emerging technologies are immense. As Marrone and Hazelton [16] conclude, “there is much more to be done in exploring both the potential benefits and limitations of new technologies for accounting” (p. 677). Activities commonly performed by accountants, such as conformity assessment, analysis, and presentation of information for decision making and the resolution of problems characteristic of the accountant’s role, can be supported by big data analytics, blockchain technology, and artificial intelligence. While professionals may feel these technologies as a threat, they also create many opportunities.

For example, Marshall and Lambert [30] found that “augmented intelligence provides greater opportunities for accountant-professionals to leverage their knowledge through federation, thereby freeing them to pursue activities that offer more value to the organization” (p. 208).

Liu et al. [31] identify many opportunities related to blockchain technology, including accountants assuming the role of planner and coordinator of potential blockchain participants or even acting as its administrator. Other tasks they identify as opportunities are examining transaction records on the blockchain, developing novel audit processes on blockchain transactions, or verifying the consistency between items on blockchain and the physical world.

When it comes to big data, the auditor’s judgment will assume a much more significant role in the data analysis environment than in the traditional (sample-based) audit due to the potential for evaluating large amounts of anomalies [32]. To take advantage of big data opportunities and, at the same time, avoid pitfalls, companies must bet on individuals who understand data analysis and the business. Accountants are already starting to work with data scientists and understand their business, so “accountants are poised to contribute meaningfully to their firms as part of the big data revolution” [33] (p. 74).

On the other hand, any novelty carries its risks, obstacles, and challenges. One of the risks identified by several authors is the willingness accountants will have to adapt in practice [34][35]. While the first analyzes the impacts of an intelligent virtual assistant, the second approaches big data analytics. Burns and Igou [34] report that “users will have to adapt to a more intimate, habit-forming interface when voice assistants are deployed in accounting workplaces” (p. 85). These interfaces can be felt as intrusive, a threat to privacy, even exceeding some social norms or boundaries, which can make users feel uncomfortable; however, at the same time, they can be addictive in nature. Feung and Thiruchelvam [35] conclude that practitioners must be willing to change and adopt big data analytics aside from the awareness of these upcoming areas. As the real-time business environment primarily propels the need for continuous auditing, practitioners cannot avoid this transition in the future.

An obstacle referred to for both financial accounting and auditing relates to the standards that should be generally applied. According to an interviewee from Al-Htaybat and von Alberti-Alhtaybat [36], “our standards currently do not allow for speculative financial information. Sure, I can include some non-financial predictions, but I could not publish a progressive financial statement in the annual report. For big data to really benefit users of corporate reporting information, we will have to look into this” (pp. 866–867).

Richins et al. [33] state that “auditors’ role in the world of big data analytics will largely depend on the evolution of auditing standards” (p. 75). For big data to fit into the audit of the financial statements, standards must be adjusted or revised, replacing or complementing the traditional way of collecting evidence by these new techniques. Kend and Nguyen [37], in a similar way, obtained evidence that it is necessary to update auditing standards so that automation challenges for auditors and their companies are overcome.

Finally, there is a general concern with the skills and knowledge that accountants should have to keep up with the newest technologies. Earley [32] expresses the concern of regulators that “auditors will lack the requisite skills to apply data analytics techniques properly, and firms will begin expanding advisory services to attract and hire data scientists with data analytics skills” (p. 497). This raises concerns about audit quality, as data scientists have a different mindset than traditional auditors, focusing more on consulting services than on auditing itself.

On the other hand, Al-Htaybat and von Alberti-Alhtaybat [36] mentioned the risks of a lack of knowledge of big data, data analytics, and this field of study, showing that a little bit of knowledge is a dangerous thing. “However, accountants’ tacit knowledge, their approach to decision-making, and their inherent values, such as conservatism, reliability, and risk-adversity, must not be eliminated and replaced by statistical analyses and data scientists’ analytical approaches. Big data needs interpretation and story-telling, which is based on prior knowledge, experience, and theory” [36] (p. 868). Instead, they recommend that multidisciplinary teams of accountants and data scientists are created, which complement and enhance each other’s experience, thereby increasing the accuracy and reliability of corporate reports [36].

Lastly, related to management accounting, Oesterreich and Teuteberg [38] found out that “the supply of business analytics competencies and IT skills in management accountant professional’s profiles tends to decrease with company size. Thus, the assumption is near that in large organizations, management accountants do not need business analytics competencies and advanced IT skills as these skills constitute a significant part of a data scientist’s job profile rather than of a management accountant’s job profile” (p. 318).

References

- Olivier, H. Challenges facing the accountancy profession. Eur. Account. Rev. 2000, 9, 603–624.

- Pazaitis, A. Breaking the Chains of Open Innovation: Post-Blockchain and the Case of Sensorica. Information 2020, 11, 104.

- Chesbrough, H.W. Open Innovation: The New Imperative for Creating and Profiting from Technology; Harvard Business Review Press: Brighton, MA, USA, 2006; p. 272.

- Skordoulis, M.; Ntanos, S.; Kyriakopoulos, G.L.; Arabatzis, G.; Galatsidas, S.; Chalikias, M. Environmental Innovation, Open Innovation Dynamics and Competitive Advantage of Medium and Large-Sized Firms. J. Open Innov. Technol. Mark. Complex. 2020, 6, 195.

- Fayyaz, A.; Chaudhry, B.N.; Fiaz, M. Upholding Knowledge Sharing for Organization Innovation Efficiency in Pakistan. J. Open Innov. Technol. Mark. Complex. 2020, 7, 4.

- Belfo, F.P.; Trigo, A. Accounting Information Systems: Tradition and Future Directions. Procedia Technol. 2013, 9, 536–546.

- Arnold, V. The changing technological environment and the future of behavioural research in accounting. Account. Financ. 2018, 58, 315–339.

- Dos Santos, B.L.; Suave, R.; Ferreira, M.M.; Altoé, S.M.L. Profissão contábil em tempos de mudança: Implicações do avanço tecnológico nas atividades em um escritório de contabilidade. Rev. Contab. Control. 2020, 11.

- Taipaleenmäki, J.; Ikäheimo, S. On the convergence of management accounting and financial accounting—the role of information technology in accounting change. Int. J. Account. Inf. Syst. 2013, 14, 321–348.

- Schmitz, J.; Leoni, G. Accounting and Auditing at the Time of Blockchain Technology: A Research Agenda. Aust. Account. Rev. 2019, 29, 331–342.

- Secinaro, S.; Calandra, D.; Biancone, P. Blockchain, trust, and trust accounting: Can blockchain technology substitute trust created by intermediaries in trust accounting? A theoretical examination. Int. J. Manag. Pract. 2021, 14, 129–145.

- George, K.; Patatoukas, P.N. The Blockchain Evolution and Revolution of Accounting. 2020. Available online: (accessed on 7 July 2020).

- Carlin, T. Blockchain and the Journey Beyond Double Entry. Aust. Account. Rev. 2019, 29, 305–311.

- Moll, J.; Yigitbasioglu, O. The role of internet-related technologies in shaping the work of accountants: New directions for accounting research. Br. Account. Rev. 2019, 51, 100833.

- Marrone, M.; Hazelton, J. The disruptive and transformative potential of new technologies for accounting, accountants and accountability: A review of current literature and call for further research. Med. Account. Res. 2019, 27, 677–694.

- International Federation of Accountants; Association of Accounting Tecnicians. An Illustrative Competency Framework for Accounting Technicians; International Federation of Accountants: New York, NY, USA; Association of Accounting Tecnicians: London, UK, 2019; pp. 1–92.

- Institute of Management Accounting. IMA Management Accounting Competency Framework; Institute of Management Accounting: Buffalo, NY, USA, 2019; pp. 1–48.

- Association of Chartered Certified Accountants. Future Ready: Accountancy Careers in the 2020s; Association of Chartered Certified Accountants: London, UK, 2020; pp. 1–72.

- Demirkan, S.; Demirkan, I.; McKee, A. Blockchain technology in the future of business cyber security and accounting. J. Manag. Anal. 2020, 7, 189–208.

- The Association to Advance Collegiate Schools of Business-International. 2018 Eligibility Procedures and Accreditation Standards for Accounting Accreditation; The Association to Advance Collegiate Schools of Business: Tampa, FL, USA, 2018; pp. 1–35.

- Chiu, V.; Liu, Q.; Muehlmann, B.; Baldwin, A.A. A bibliometric analysis of accounting information systems journals and their emerging technologies contributions. Int. J. Account. Inf. Syst. 2019, 32, 24–43.

- Fullana, O.; Ruiz, J. Accounting Information Systems in the Blockchain Era. 2020. Available online: (accessed on 7 July 2020).

- Lombardi, R.; Secundo, G. The digital transformation of corporate reporting—A systematic literature review and avenues for future research. Med. Account. Res. 2020.

- Lamboglia, R.; Lavorato, D.; Scornavacca, E.; Za, S. Exploring the relationship between audit and technology. A bibliometric analysis. Med. Account. Res. 2020.

- Wolf, T.; Kuttner, M.; Feldbauer-Durstmüller, B.; Mitter, C. What we know about management accountants’ changing identities and roles—A systematic literature review. J. Account. Organ. Chang. 2020, 16, 311–347.

- Saputro, V.S.; Ritchi, H.; Handoyo, S. Blockchain Disruption on Management Accountant’s Role: Systematic Literature Review. J. Account. Audit. Bus. 2021, 4, 1–13.

- Denyer, D.; Tranfield, D. Producing a systematic review. In The Sage Handbook of Organizational Research Methods; Buchanan, D.A., Bryman, B.A., Eds.; Sage Publications Ltd.: Thousand Oaks, CA, USA, 2009; pp. 671–689.

- Coyne, J.G.; Summers, S.L.; Williams, B.; Wood, D.A. Accounting Program Research Rankings by Topical Area and Methodology. Issues Account. Educ. 2010, 25, 631–654.

- Abad-Segura, E.; González-Zamar, M.-D. Research Analysis on Emerging Technologies in Corporate Accounting. Mathematics 2020, 8, 1589.

- Marshall, T.E.; Lambert, S.L. Cloud-Based Intelligent Accounting Applications: Accounting Task Automation Using IBM Watson Cognitive Computing. J. Emerg. Technol. Account. 2018, 15, 199–215.

- Liu, M.; Wu, K.; Xu, J.J. How Will Blockchain Technology Impact Auditing and Accounting: Permissionless versus Permissioned Blockchain. Curr. Issues Audit. 2019, 13, A19–A29.

- Earley, C. Data analytics in auditing: Opportunities and challenges. Bus. Horiz. 2015, 58, 493–500.

- Richins, G.; Stapleton, A.; Stratopoulos, T.; Wong, C. Big Data Analytics: Opportunity or Threat for the Accounting Profession? J. Inf. Syst. 2017, 31, 63–79.

- Burns, M.B.; Igou, A. “Alexa, Write an Audit Opinion”: Adopting Intelligent Virtual Assistants in Accounting Workplaces. J. Emerg. Technol. Account. 2019, 16, 81–92.

- Feung, J.L.C.; Thiruchelvam, I.V. A framework model for continuous auditing in financial statement audits using big data analytics. Int. J. Sci. Technol. Res. 2020, 9, 3416–3434.

- Al-Htaybat, K.; Von Alberti-Alhtaybat, L. Big Data and corporate reporting: Impacts and paradoxes. Account. Audit. Account. J. 2017, 30, 850–873.

- Kend, M.; Nguyen, L.A. Big Data Analytics and Other Emerging Technologies: The Impact on the Australian Audit and Assurance Profession. Aust. Account. Rev. 2020, 30, 269–282.

- Oesterreich, T.D.; Teuteberg, F. The role of business analytics in the controllers and management accountants’ competence profiles: An exploratory study on individual-level data. J. Account. Organ. Chang. 2019, 15, 330–356.

More

Information

Subjects:

Others

Contributor

MDPI registered users' name will be linked to their SciProfiles pages. To register with us, please refer to https://encyclopedia.pub/register

:

View Times:

3.6K

Revisions:

3 times

(View History)

Update Date:

01 Jul 2021

Table of Contents

Notice

You are not a member of the advisory board for this topic. If you want to update advisory board member profile, please contact office@encyclopedia.pub.

OK

Confirm

Only members of the Encyclopedia advisory board for this topic are allowed to note entries. Would you like to become an advisory board member of the Encyclopedia?

Yes

No

${ textCharacter }/${ maxCharacter }

Submit

Cancel

Back

Comments

${ item }

|

${ item.createdUser.fullName }

${ item.createdAt }

${ item.vote }

${ item.reply }

Delete

${ reply.createdUser.fullName }

${ reply.createdAt }

${ reply.vote }

Delete

There is no reply to this comment~

${ item.replyTextCharacter }/${ item.replyMaxCharacter }

Submit

Cancel

More

No more~

There is no comment~

${ textCharacter }/${ maxCharacter }

Submit

Cancel

${ selectedItem.replyTextCharacter }/${ selectedItem.replyMaxCharacter }

Submit

Cancel

Confirm

Are you sure to Delete?

Yes

No