In 2020, Lithium has been included in the list for Critical global elements critical metal, and will be one of the drivers of the fourth industrial revolution. Lithium company stocks on the worldwide exchanges have rallied from the end of 2020 and through 2021 with many Lithium Explorers/Developers/Producer miners' share prices' rising 1000% to 6000% within 12 months on the ASX: the Australian Securities Stock Exchange. Stocks are expected to continue to rally as a shortfall deficit of Lithium supply world-wide is expected from beginning of 2022. The Battery-grade Lithium deficit is expected to persist to an incredible 2030, as there are not enough mines coming online to supply the demand in EV Batteries & Energy Storage systems to 2030. This makes Lithium a highly lucrative commodity to invest into, the term entered a "Lithium commodities Super-cycle" has been used by industry commentators during 2021 to describe the event, also the term "A Once in a Century" event is occurring in 2021 and will persist till new Energy technologies come online to replace Lithium Batteries, this is not expected till after 2040 as there are no technologies that will be suitable for the diversity of applications for Lithium Energy storage systems. Lithium carbonate prices have made a resurgence from 2019-2020 all time lows, rising some 500% as of 21/11/2021 trading at US$29,000/tonne, Lithium Carbonate/Lithium Hydroxide is a Lithium chemical compound also known as LCE(Lithium Carbonate Equivalent) and is used as a Precursor in the manufacture of Cathode Cells for electric vehicle (EV) batteries. As a result and along with major Governmental new energy policies in 2020, in preparation to the fazing out of fossil fuels & reductions in carbon emissions vehicles & coal power, has kick-started a flurry of renewed investments & Joint Ventures/acquisitions between Miners & Strategic major investor companies throughout the world. Recently the world saw the COP26: Climate Change Summit for Action in Glasgow during November 2021. The agreements signed by all countries involved, has accelerated the action towards renewables adoption & the reforestation among other items & actions. Lithium will play a key & critical role towards the reduction of Carbon emissions, "1.5ToStayAlive" "1.5toSurvive" slogans for maintaining the critical 1.5 degrees & the storage of renewables clean green energy, harnessed from the sustainable wind, solar & hydropower, also tidal. Also big on the COP26 agenda was the fazing out of coal all-together. Lithium is an essential mineral that goes into the manufacture of electric batteries (Lithium-ion battery: portable electronics, EV and renewable ESS). Lithium supply is expected to fall short of the demand for this metal by 2022. Demand/supply discrepancy "the Great divide" ratio has been witnessed in July 2021 when the BMX Spot price Platform went live and the price for Lithium Spodumene Concentrate 6% (SC6) reached a record price of US$1,400/tonne, rising from its lowest of US$395/tonne in September 2020. Today SC6 price(21 November 2021) trades at US$2,550/tonne, Australia's Pilbara Minerals, the company that developed the BMX Spot Sales Platform are commended for this initiative with Ken Brinson, CEO, saying the price for Spodumene Concentrate 6% is now transparent to the market making it a fairer playing field for the Miners and the Chemical Converter Customers. Governments are adopting the New Energy Lithium Technology rapidly as the pressure to meet the Paris Agreement CO2 Carbon emissions reductions. Major Car Manufacturers are planning on a large line-up of new Electric Vehicles by 2025, in what's called the "EV Revolution". The growing adoption of electric vehicles (EVs) is driving the increasing demand for lithium, significant amounts of lithium supply will need to be brought online to meet this demand growth to 2030 and beyond. The situation is seen as critical as the world depends on Lithium. A new technology in the extraction of Lithium from Geothermal brine, the extraction method is called DLE-Direct Lithium Extraction and if/when the technology succeeds in "scale" it will be celebrated as it will help alleviate the pressure on the tight Lithium supply, the technology is not expected for another 4-5 yrs(2025/26) if not longer. See Start-ups Vulcan Energies(ASX:VUL) & Lilac Solutions(USA) for their efforts in DLE. Pond evaporation extraction Technology is considered old & expected to be obsolete as it conflicts with a world turning towards ESG(Environmental Social & Governance) compliance in mining/extractive practices. Products that reduce carbon emissions, including electric batteries, are globally expected to create a $23 Trillion market over the next decade to 2030. Lithium is considered a superior lightweight metal element for its electrochemical properties as a charge carrier in the electric battery, currently there is no known replacement element to achieve such effective performance for automotive battery applications. According to Volkswagen, in the near future lithium will be one of the most sought-after raw metals on earth. Forecasted EV battery demand growth is driving the need to significantly increase battery production globally. Major battery manufacturers have already committed $175Billion by the start of 2021. Even though a significant amount of capital has already been committed, further investment is expected, to satisfy the forecasted growing supply chain demand of batteries to 2030. There has been a trend already with lithium chemicals compounds producing companies, battery manufacturer companies and even major car manufacturers investing or partnering with raw material suppliers/miners. Large investments are flowing into the lithium supply chain from established majors. Companies with partnerships or joint ventures will be more resilient in the long run. Major car manufacturers' plans to spend over $300 billion are being invested and forecasted over the next 4 (2025) to 10 years (2030) during the adoption of electric vehicles (EV). Automakers’ plans to spend at least $300 billion on EVs are driven largely by environmental concerns and government policy for GHG reduction and supported by rapid technological advances that have improved battery cost, range and charging time. Since 2018, we have seen an accelerated rate of industry spending especially through 2020. Most importantly, with the global push for sustainable and low carbon footprint mining, processing and manufacturing, where will the lithium that is ESG sustainably sourced with a GHG low-carbon footprint come from. Necessary to feed the burgeoning energy storage needs for the growing transport and military sector; electronic consumer requirements; and in particular the domestic & commercial automotive supply chain where investment spending and forecasts are $US400 to $US500 billion . Both the drive to decarbonize and the 4IR depend on critical minerals like lithium. The Fourth Industrial Revolution (4IR or Industry 4.0) has been defined as technological developments in cyber-physical systems such as high capacity connectivity; new human-machine interaction modes such as touch interfaces and virtual reality systems; and improvements in transferring digital instructions to the physical world including robotics and 3D printing (additive manufacturing); the Internet of Things (IoT); “big data” and cloud computing; artificial intelligence-based systems; improvements to and the uptake of Off-Grid / Stand-Alone Renewable Energy Systems: solar, wind, wave, hydroelectric and the Lithium-ion electric batteries (for renewable ESS and EV). Speculation in lithium compounds used as feedstocks for major applications. The main intermediates are lithium hydroxide and lithium carbonate, and these are the commodities that the LME has chosen as the most appropriate to establish reference pricing. Speculators hope to make a viable play on a perceived growth in demand for lithium metal due to the widespread adoption of lithium batteries in emerging technologies. Lithium batteries have become a preferred power source for energy-hungry devices such as cell phones because they are more efficient and scalable than previous-generation nickel-metal hydride batteries thus they are in high demand in support of automobile and electronics manufacturing. Factors that could result in limitations affecting overall lithium supply are seen by some as prescient; with predicted supply chain volatility potentially overpowering other market factors and becoming the primary price driver, essentially resulting in a seller's market and thereby making the metal a profitable investment.

- supply chain volatility

- automotive supply chain

- virtual reality

1. Uses of Lithium

Lithium metal is an extremely soft, highly reactive, and flammable element. It is most frequently found in deposits such as spodumene and pegmatite minerals,[1] with larger resources in the Democratic Republic of Congo, U.S., Canada, Australia, China, Zimbabwe, and Russia. Lithium possesses a unique chemical profile making it the lightest metal in the periodic table and the least dense solid element. Its atomic number is 3 (right behind helium at 2 and hydrogen at 1), and its density is just 0.53 kg/L.

This alkali metal is probably best known for its wide use in lithium batteries common in all sorts of electronics devices. Other industrial applications include manufacturing heat-resistant glass and ceramics, high-performance alloys used in aircraft, and lubricating greases.[2] Lithium deuteride is used in staged thermonuclear weapons as a fusion fuel. Compounds of lithium are also used as mood stabilizing drugs in psychiatry. The breakdown of the global end-use lithium markets is estimated as follows: ceramics and glass, 31%; batteries, 23%; lubricating greases, 9%; air treatment, 6%; primary aluminum production, 6%; continuous casting, 4%; rubber and thermoplastics, 4%; pharmaceuticals, 2%; and other uses, 15%.[3]

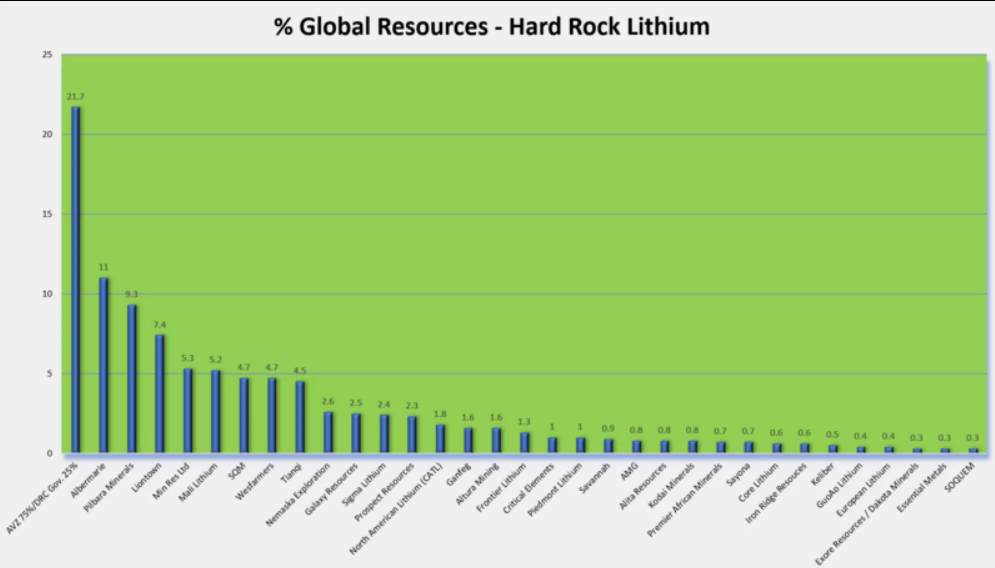

2. Global Resources and Production

The global production of lithium is set to grow five times from 80,000 tons in 2020 to 400,000 tons by 2030. Volkswagen described hard-rock lithium mining as the “future-proof solution, both commercially and in terms of sustainability.” Mining lithium metal is not expensive, especially at high mountain plateaus, where lithium is collected from brine ponds evaporated by the sun. The environmental and social impact has been a contentious issue in northern Chile for a decade from farmers and indigenous groups in certain locations where natural water is scarce in the arid deserts, where these highly lucrative mining exists, prompting a recent study completed by the Chilean government regulator Corfo, which will be released early in 2021.[4] There is a shift towards a preference for spodumene hard rock partly due to the inputs (Lithium Hydroxide chemical) for the production of electric vehicle (EV) battery cells. Favored for newer cathode technologies, specifically higher nickel chemistries to increase battery energy density. In the five years to 2018 the largest increase in world lithium production has come from hard rock mines in Western Australia, with 6 mines now in production.[5]

Identified lithium resources total approximately 80 million tons, lithium has been added to the critical minerals list[6] in 2020. Identified lithium resources for Bolivia and Chile are 9 million tons and in excess of 7.5 million tons, respectively. Identified lithium resources for Democratic Republic of Congo (Manono), Argentina, China, United States and Australia are 6.6 million tons, 6.5 million tons, 5.4 million tons, 5.5 million tons and 1.7 million tons, respectively. Canada, Russia, and Serbia have resources of approximately 1 million tons each. Identified lithium resources for Brazil total 180,000 tons.[7]

The world's top 3 lithium-producing countries from 2016, as reported by the US Geological Survey.[8]

2.1. Democratic Republic of Congo

A new entrant into the lithium market as a developing producer.

Since 2018 the Democratic Republic of Congo (DRC) is known to have the largest lithium spodumene hard rock deposit in the world.[9] The total resource of the deposit located in Manono, central DRC, has the potential to be in the magnitude of 1.5 billion tons of lithium spodumene hard-rock. The two largest pegmatites (known as the Carriere de l'Este Pegmatite and the Roche Dure Pegmatite) are each of similar size or larger than the famous Greenbushes Pegmatite in Western Australia. In 2023, the Democratic Republic of Congo is expected to be a significant supplier of lithium to the world with its high grade and low impurities.

As of 2021, the Australia n company AVZ Minerals[10] is developing the Manono Lithium and Tin project in Manono, DRC and has a resource size of 400 million tonnes of high grade low impurities at 1.65% lithium oxide (Li2O)[11] spodumene hard-rock (this figure is expected to more than triple with further drilling), based on studies and drilling of Roche Dure, one of several pegmatites in the deposit. There is a push globally by the European Union (EU) and major car manufacturers (OEM) for the lithium battery supply chain to produce and source materials sustainably along the entire chain and incumbents practicing Environmental, social and corporate governance (ESG) initiatives and aiming for zero to low carbon footprint.[12] The AVZ Minerals Manono project has completed a GHG greenhouse study in Jan 2021 into its future carbon footprint,[13] showing the project to likely have one of the lowest carbon footprint of all the spodumene hard rock producers by 30% to 40% and some brine producers throughout the world. AVZ Minerals recently signed a long-term offtake partnership with major Ganfeng Lithium, China's largest lithium compounds producer. Importantly, the partnership makes provisions for both parties to focus on environmental, social and governance (ESG) development.

Planned production of battery-grade high-purity primary lithium sulfate (PLS) containing over 80% Lithium,[14] a lithium chemical new to the electric Lithium-ion battery materials supply chain market, PLS is used in the production of lithium hydroxide (a precursor to electric vehicle battery compound production), production is expected to be in the order of 45,600 tonnes per annum, with plans to significantly increase production to satisfy the soaring electric vehicle battery demand from Europe, China, Asia, USA and other new global entrants. AVZ Minerals have a study currently underway to determine the viability of an initial 25Kt/a Hydroxide plant in Europe, increasing this to ≃100Kt/a capacity, including ongoing discussions with key battery industry participants to enter joint ventures with AVZ to build the plants in Europe and elsewhere.

2.2. Europe

Europe has no hard rock / spodumene production as of March 2021. Europe has no LiOH (Lithium Hydroxide) and Li2CO3 (Lithium Carbonate) production as of March 2021.

2.3. Australia

In 2016, Australian companies delivered 14,300 tons of metal, an increase of 1,300 tons from 2014. The country develops the Greenbushes lithium project, which is owned and operated by Talison Lithium. Greenbushes is the world's largest known single lithium reserve and has been operational for over 25 years. The location also provides easy access for Asian electronics companies, which are the global top lithium consumers. All Australian production to date has been in the form of spodumene concentrate containing approximately 6% LCE, all of which was shipped to China for refining. In 2017-18 Australian production had increased to 2.1 million tonnes of spodumene concentrate worth $1.6 billion. Three separate refineries are under construction which will produce lithium hydroxide and lithium carbonate. [15]

2.4. Chile

In 2016, Chilean mines delivered 12,000 tons of lithium, providing the second-highest amount of lithium. Overall, Chile possesses the largest confirmed lithium reserves in the world, with over 7.5 million tons of the element. By that estimate, the country hosts roughly five times more lithium than Australia, which features the second-largest reserves. In particular, the Atacama salt flat is the most significant source of country's massive lithium production, and it has been reported that one project alone encompasses approximately 20% of the world's total lithium. While Australia extracts lithium from traditional hard-rock mines, Chile's lithium is found in brines below the surface of salt flats. These brines are collected and treated in order to separate the element from wastewater.

2.5. Argentina

In 2016, for the first time, Argentina overtook China to become the third largest producer of lithium. Argentina has lithium reserves of 9,000,000 tons and the Salar del Hombre Muerto district is a part of the so-called lithium triangle which is believed to be home to half of the world's land based lithium reserves. Due to increased demand worldwide, lithium mining in the country shows no signs of slowing down with output set to triple by 2019.

2.6. Canada

Canada is a new entrant into lithium market as a potential supplier.

3. The Lithium Triangle

The intersection of Chile , Bolivia, and Northwest Argentina make up the region known as the Lithium Triangle. The Lithium Triangle is known for its high quality salt flats including Bolivia's Salar de Uyuni, Chile's Salar de Atacama, and Argentina's Salar de Arizaro. The Lithium Triangle is believed to contain over 75% of existing known lithium reserves.[16]

4. Investment Vehicles

Currently, there are a number of options available in the marketplace to invest in the metal. While buying physical stock of lithium is hardly possible, investors can buy shares of companies engaged in lithium mining and producing.[17] Also, investors can purchase a dedicated lithium ETF offering exposure to a group of commodity producers. As of October 2020, there lithium hydroxide and carbonate futures are not yet traded, but historical reference prices are being established with a view to doing so.[18]

4.1. Lithium Index

The performance of the global lithium industry is covered by Solactive Global Lithium Index. The index is composed of companies that are primarily engaged in some aspect of the lithium industry such as lithium mining production and lithium-ion battery production.

4.2. Mining companies

There are many companies relying on lithium for a substantial portion of their revenues. Examples include:

- AVZ Minerals Limited is an Australian ASX-listed mineral development company focused on financing & constructing the Manono Lithium & Tin Project, one of the world's largest lithium-rich LCT (lithium, caesium, tantalum) pegmatite deposits.

- Ganfeng Lithium is a Chinese lithium refiner, primarily of spodumene from Mt Marion in WA.

- Advantage Lithium, a Canadian-based lithium explorer with a large-scale development asset located in the Cauchari basin in Argentina, which now is part of Orocobre

- Sociedad Química y Minera, a Chilean producer of specialty plant nutrients and chemicals that runs large-scale lithium production operations. The main production facilities are located in the Atacama Desert.

- Livent Corporation, Formally FMC Lithium Division was spun-off into a dedicated lithium company in Oct 2018

- Albemarle Corporation, an industrial company producing lithium chemicals

- Bearing Resources, a Canadian miner developing a lithium brine project in Chile and the highest-grade undeveloped project

- Bacanora Minerals, a Canadian miner developing a lithium mine in Mexico, Sonora, first to enter in a conditional supply agreement with Tesla

- Lake Resources, an Australia company which holds tenements in Chile and one of the largest lithium tenement packages in Argentina

- Westwater Resources, Inc. has projects in uranium, graphite, lithium, and vanadium. They have two lithium projects in the early stages of development - one in Utah and the other in Nevada.[19]

- Lithium Americas Corp, a Canadian/Argentinian miner, producer and supplier of lithium, with large-scale assets located Argentina and the U.S. state of Nevada

- RB Energy, a Canadian company developing The Quebec Lithium Project, filed for creditor protection in 2014, according to the Financial Post[20]

- MGX Minerals, a diversified Canadian mining company engaged in petrolithium projects in western Canada and the United States[21]

- Kodal Minerals, a small-cap mining and exploration company that currently focuses on its large lithium project in Mali.

- E3 Metals Corp, a lithium developer based in Alberta

- MétAmpère Limited, developing a hard rock lithium mine and processing plant in Cornwall, UK

- Standard Lithium, a Canadian technology company, has developed their own DLE process and is progressing with a lithium extraction project utilizing lithium-bearing brines in Arkansas. They also have a land package in California for expected future development. They recently report progress at the Arkansas site including a USD$100 million investment by Koch Industries.

4.3. Exchange Traded Funds

- Global X Lithium ETF (NYSE: LIT), an ETF trading since 2010 and holding the above listed lithium producers as its top holdings. LIT is a passive ETF seeking to replicate Solactive Global Lithium Index.

4.4. Direct Investment

- HWS AG's German Lithium Participation Program offers the first direct investment opportunity in lithium carbonate. The lithium carbonate is stored in special lithium investment units in secured German warehouses.[22]

The content is sourced from: https://handwiki.org/wiki/Chemistry:Lithium_as_an_investment

References

- "Lithium Deposits: Pegmatite and Sedimentary". Investing News Network. September 29, 2020. https://investingnews.com/daily/resource-investing/battery-metals-investing/lithium-investing/lithium-deposits-pegmatite-and-sedimentary/#:~:text=Lithium%20in%20pegmatites%20is%20most,to%20host%20pegmatite%20lithium%20deposits..

- "How to Invest in Lithium". commodityhq.com. http://commodityhq.com/commodity/rare-earthstrategic-metals/lithium-/.

- "How to Invest in Lithium". elementinvesting.com. http://www.elementinvesting.com/investing_in_lithium.htm.

- "Albemarle slams Chile over 'unjust' withholding of Atacama study". Mining.com, Reuters. March 4, 2021. https://www.mining.com/web/albemarle-slams-chile-over-unjust-withholding-of-atacama-study/.

- "WESTERN AUSTRALIAN MINERAL AND PETROLEUM STATISTICS DIGEST 2017-18". http://www.dmp.wa.gov.au/Documents/About-Us-Careers/Stats_Digest_2017-18.pdf.

- "Critical Minerals". 15 May 2014. https://www.ga.gov.au/about/projects/resources/critical-minerals#heading-3.

- "Lithium Statistics and Information". U.S. Geological Survey. 2011. http://minerals.usgs.gov/minerals/pubs/commodity/lithium/.

- "8 Top Lithium-producing Countries". Commodity.com. December 14, 2017. https://commodity.com/precious-metals/lithium/#The_Top_Lithium_Producing_Countries.

- "This Congo project could supply the world with lithium". MiningDotCom. December 10, 2018. https://www.mining.com/one-congo-project-supply-world-lithium/.

- "AVZ Minerals Limited". https://avzminerals.com.au/.

- "AVZ Minerals Definitive Feasibility Study (DFS - April 2020)". https://avzminerals.com.au/manono-project-definitive-feasibility-review.

- "Green Deal: Sustainable batteries for a circular and climate neutral economy". 10 December 2020. https://ec.europa.eu/commission/presscorner/detail/en/ip_20_2312.

- "AVZ Minerals: Independent Greenhouse Study states Manono Project likely to have one of the lowest carbon footprints of any global hard rock lithium miner". Small Caps. https://smallcaps.com.au/greenhouse-study-avz-minerals-lowest-carbon-footprint-manono-lithium-tin-project/.

- "AVZ Minerals testing confirms primary lithium sulfate is suitable for battery production feedstock". proactive. 13 Jan 2021. https://www.proactiveinvestors.com.au/companies/news/938266/avz-minerals-testing-confirms-primary-lithium-sulphate-is-suitable-for-battery-production-feedstock-938266.html.

- "WESTERN AUSTRALIAN MINERAL AND PETROLEUM STATISTICS DIGEST". WA Government Dept Mining and Petroleum/. 2019. http://www.dmp.wa.gov.au/Documents/About-Us-Careers/Stats_Digest_2017-18.pdf.

- "The Lithium Triangle"http://latintrade.com/the-lithium-triangle/. Latin Trade. Retrieved 2017-8-13.

- "Lithium stocks on the ASX: The Ultimate Guide". Small Caps. February 27, 2019. https://smallcaps.com.au/lithium-stocks-asx-ultimate-guide/.

- "Lithium at the LME". London Metals Exchange. https://www.lme.com/Metals/Minor-metals/Lithium-prices#tabIndex=0.

- Westwater Resources, Inc. (2018-09-26) (in en-US), Westwater Resources - Lithium Market, https://www.westwaterresources.net/minerals-portfolio/the-lithium-market, retrieved 2018-09-26

- "RB Energy meltdown highlights tough times for lithium, rare earth firms". Financialpost (Financial Post). http://business.financialpost.com/news/mining/rb-energy-meltdown-highlights-tough-times-for-lithium-rare-earth-firms.

- "Canada's MGX Minerals hunts battery lithium in oilfields". Reuters. 30 January 2017. https://www.reuters.com/article/mgx-minerals-lithium-idUSL5N1FH5U7.

- "Lithium investment opportunity » German Lithium". https://germanlithium.com/language/en/.