To accomplish the 1.5 °C and 2 °C climate change targets, the European Union (EU) has set up several policy initiatives. Within the EU, the carbon emissions of the road transport sector from the consumption of diesel and gasoline are constantly rising. (1) Background: due to road transport policies, diesel and gasoline use within the EU is increasing the amount of carbon in the atmosphere and adding to climate risks. (2) Methods: sustainability analysis used was based on the method recommended by the Intergovernmental Panel on Climate Change. (3) Results: to meet its road transport requirements, the EU produces an estimated 0.237–0.245 billion tonnes of carbon per year from its total consumption of diesel and gasoline. (4) Conclusion: if there is no significant reduction in diesel and gasoline carbon emissions, there is a real risk that the EU’s carbon budget commitment could lapse and that climate change targets will not be met. Sustainability analysis of energy consumption in road transport sector shows the optimum solution is the direct electrification of road transport.

1. Introduction

Decarbonisation of road transport in response to the climate change challenge is a complex political, economic and technological challenge for all stakeholders in the European Union (EU). To address this challenge, a sustainability study that estimates the greenhouse gas (GHG) emissions and energy consumption from diesel and gasoline consumption within the EU is needed. This paper presents a clear picture of the scale of the challenge and unpacks the complexity associated with the challenge of decarbonisation. Emissions from road transport consumption of diesel and gasoline are classified as downstream emissions. A new conceptual model of sustainability is needed to develop a coherent decarbonisation policy in road transport.

2. Results of GHG and Carbon Emission Estimation

The results are provided in

Table 1 and

Figure 2 below. The complete dataset is given in the

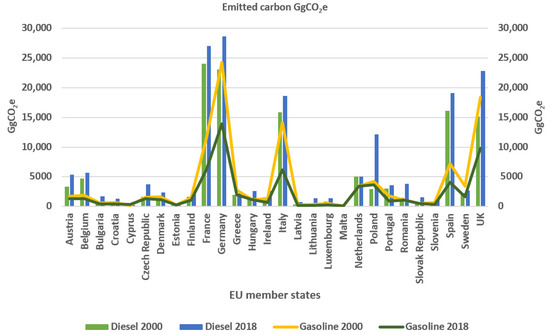

Appendix A. The majority of member states exhibited a consistent pattern of diesel GHG emissions increasing and gasoline GHG emissions decreasing between 2000 and 2018. The total GHG emissions from diesel were highest in Poland, the United Kingdom, Germany, Spain and France and lowest in Cyprus, the Netherlands, Malta, Estonia and Greece. The GHG emissions from gasoline were highest in Germany, the United Kingdom, Italy, France and Spain and lowest in Malta, Hungary, Estonia, Romania and the Slovak Republic. The Netherlands was an exceptional case as its diesel and gasoline road transport emissions remained constant between 2000 and 2018.

Figure 2. Emitted carbon from diesel and gasoline use by EU member states in 2000 and 2018.

Table 1. Diesel and Gasoline carbon emissions in EU 28 (2000 and 2018).

Overall, transport carbon emissions increased between 2000 and 2018, with the EU’s Road transport sector adding 0.23–0.24 Gt of carbon to the atmosphere each year. The approach taken was based on real fuel consumption of diesel and gasoline within the EU. These results show that transport emissions are not necessarily related to the size of the economy and are actually a result of national transport policy. The net amount of diesel- and gasoline-based energy consumed by the EU’s road transport sector was 3335 TWh in 2000 and 3377 TWh in 2018. It is profoundly challenging to permanently substitute these energy requirements with low carbon options, and these results suggest that the total EV charging capacity for Europe needs to exceed 3000 TWh per year if a net zero in road transport is to be accomplished.

These results indicate that over an 18-year period, the energy input in road transport increased by 42 TWh, which is an increase of 2.33 TWh per year. As mentioned previously, the decarbonisation base case study [

19] estimated the EU energy input requirement to be 2800 TWh per year.

3. Critical Analysis of Results and the Sustainability Approach

As mentioned previously, the decarbonisation of transport is a major economic, societal and political challenge for the EU. The underlying cause of the constant increase in diesel consumption is the nature of the fuel market and the fuel taxation system in the EU. As we have seen, gasoline consumption decreased in all member states (expect one) and diesel emissions increased. High duty on gasoline and lower duty on diesel has contributed to a market-based shift in favour of diesel road transport vehicles. Customers choose diesel vehicles as they are considered better value for money in the long term.

This belief in the economy of diesel has led to an increase in diesel emissions. The EU’s fuel duty policy is influenced by the long-term goal of obtaining more mileage from diesel fuel and thereby maximising the purchasers’ advantage in the oil import market. The fuel excise policy is skewed even though diesel has a higher CO2 emissions factor than gasoline: 74,100 KgCO2/TJ for diesel and 69,300 KgCO2/TJ for gasoline. The carbon content of diesel is also higher than that of gasoline, while the net calorific values of diesel and gasoline are similar. The EU does not gain any substantial advantage by consuming more diesel nor does it have any particular incentive to do so.

The results do not take into account the number of diesel and gasoline cars in each EU member state, the number of miles travelled by the cars and the specific economic drivers that lead to the emission of GHGs. The methodology estimates the total amount of energy and emissions to measure GHG emissions. To overcome the climate change challenge, the EU must avoid these emissions, and the prevailing sustainability policy falls short when addressing the climate sustainability challenge. According to the Global Carbon Budget [

27], a reduction of 1–2 GtCO

2 is needed to achieve the goals of the Paris Agreement.

At present, there is a real risk that road transport GHG emissions will consume the majority of the EU’s carbon budget [

8]. One study calculated the EU’s carbon budget for 2010 to 2100 as being 83 Gt and 116 Gt for the 1.5 °C and 2 °C scenarios, respectively [

28]. Another study calculated the EU’s carbon transport budget as being between 10.2 and 12.1 GtCO

2e, which included aviation, rail and navigation emissions [

29]. The results in

Table 1 and the

Appendix A show that the total carbon emissions for road transport in the EU in 2000 and 2018 were 0.23 GtCO

2e and 0.24 GtCO

2e, respectively. These totals do not include aviation, shipping and navigation emissions. This indicates that BAU annual road transport emissions in the EU are in the range of 0.23–0.24 GtCO

2e. It should be noted that these emissions will decrease as the United Kingdom is no longer an EU member state.

The BAU trajectory of road transport carbon emissions in the EU is outlined in Table 2. There are limitations to the BAU scenario, however, as it assumes that long-term carbon emissions will remain at 0.23 or 0.24 GtCO2e per year. In addition, the results shown in Table 1 and Table 2 may vary as default emission factors were used to calculate the CH4 and N2O emissions. If the rate of carbon emissions does not decrease, the EU will have used up its allocated carbon transport budget by the early 2060s. Road transport emissions will consume a significant part of EU’s total carbon budget.

Table 2. BAU road transport emissions and the EU carbon budget for 1.5 °C and 2 °C scenario.

4. Critical Analysis of EU Road Transport Policy and Sustainability

The results revealed a conundrum for EU policy makers: if the EU reduces gasoline GHG emissions, it will have to use more diesel as its main road transport fuel. The results showed a net increase in GHG emissions between 2000 and 2018, and there is evidence to suggest that this was caused by the fuel excise duty of member states. The move from gasoline to diesel was caused by the EU’s policy on fuel excise duty as excise duty on gasoline is higher than that on diesel. To successfully achieve net zero or even a reduction in emissions, a new paradigm is required to reduce transport-based carbon emissions. Europe’s prevalent ‘command and control’ regulatory emission reduction mechanism will lead to a breach of the emission reduction target.

4.1. EU Market Dimensions in Road Transport Policy and Sustainability

The automotive sector contributes 4% to Europe’s GDP [

30], and 12 million people work in this industry. It also contributes 388 billion euros in tax to the EU. Car availability in the EU has increased due to competitive pricing, growth in the second-hand market and the financial relationship between the manufacturers, their dealers and finance companies [

31]. The average engine power in kilowatts (kW) in the EU (here EU refers to the EU-15 and EFTA) increased from 72 to 93 kW between 2000 and 2015. Cars in Luxembourg, Sweden and Germany have an average power of 112 kW, 106 kW and 102 kW, respectively [

32]. The highest percentage of 4×4s in the EU is in Luxembourg (23%) [

33].

Engine displacement and its distribution in the passenger transport fleet also play important roles in determining the emissions of a country. For example, Li et al. [

34] looked at the CO

2 emission factors for gasoline cars in Beijing and found that an engine displacement increase of one level led to an emission factor increase of 56.79 gCO

2/km.

Changes in motorisation patterns can also increase carbon emissions [

35]. Luxembourg has the highest rate of motorisation in the EU, while the largest increases in motorisation between 1980 and 2014 were seen in Romania, Poland, Estonia, Greece, Lithuania and Latvia. In contrast, France showed the smallest increase.

Controlling and managing the complex passenger car market and all the supply chains is challenging as the stakeholders, their finance companies and car retail dealers are important political stakeholders in the EU. For example, 2012 data on the fiscal income from motor vehicles revealed it was 80 billion euros for Germany and 64.8 billion euros for the UK [

36]. Similarly, an income of 71 billion euros each for Italy and France was reported for 2014. The EU’s fuel excise duty is higher for gasoline and lower for diesel in all EU member states except in the United Kingdom [

36].

The most recent White Paper report on CO

2 emissions from passenger cars in the EU, From Laboratory to Road [

37], claimed that the CO

2 emission values of new European passenger cars increased from approximately 9% in 2001 to 42% in 2016.

The European Commission produced major initiatives for road transport sustainability in two White Papers in 2001 and 2011. These White Papers focused on promoting an integrated environmental and transport system across the EU [

38]. Recently, the European Commission [

39] announced its plan to reach a 55% reduction in carbon emissions. This will mean that half of the cars sold in the EU in 2030 will be electric. A road transport emission trading scheme was also announced. These proposals aim to introduce new economic and investment drivers within the EU market. For example, the 2021 Tax Guide [

40] of the European Automobile Manufacturer Association stated that the EU’s annual fiscal income from the motor vehicles industry was 398.4 billion euros.

4.2. Sustainability in Road Transport Emissions for 1.5 °C and 2 °C Scenarios

Decarbonisation will build resilient road transport infrastructure and is an important action for combatting climate change and its impact. Policies to decarbonise transport by improving vehicle efficiency and developing technologies such as hybrid, plug-in hybrid and battery electric vehicles (BEVs) will help achieve the carbon targets of the EU and help meet goals 9 and 13 of the Sustainable Development Goals [

41].

The carbon emissions produced by the consumption of diesel and gasoline could also be temporarily reduced through changes in fuel excise levies. To further reduce emissions, the EU could restrict the engine sizes of vehicles and leverage the fuel tax and engine power of vehicles. It could also promote competition between internal combustion engine (ICE) manufacturers and the BEV car industry. BEVs and adequate renewable charging infrastructure are an effective path to road transport sustainability. It is important to state that studies have shown that the electrofuel supply chain also emits a significant amount of GHGs. For example, a recent paper indicated that blue hydrogen can create 60% more GHG emissions than burning diesel for heating or combustion [

42].

The EU has a fiscal incentive to make the decarbonisation of downstream emissions the main pillar of sustainability. Exposure to international competition from BEV manufacturers will make EU car manufacturers more dependent on financial support from the European Commission. The prevailing fuel excise duty gap between diesel and gasoline will gradually diminish and emission trading will open EU member states to new market influences. The shift to low carbon or net-zero road transport could readily take place within an urban-demographic environment (e.g., in Berlin, Madrid, Paris, Warsaw, Rome and London). In the long-term, the EU could abolish the use of diesel and gasoline ICEs and provide a renewable energy-powered EV or BEV infrastructure.

5. Conclusions

The EU automotive industry creates GHG emissions but also contributes significantly to the fiscal income of the EU. Road transport carbon emissions increased between 2000 and 2018, with fuel excise duty potentially leading to a reduction in gasoline consumption. The sustainability analysis highlights a need to harmonise fuel excise duty across member states. In the short term, the fuel excise duty could be leveraged to initiate emission reductions in the EU. The results suggest that giving a fiscal advantage to EV users could reduce emissions but also lead to lower tax revenue.

At this stage, the optimum solution is the direct electrification of road transport through the use of BEVs and other low carbon options. The most suitable sustainability option involves updating the approach to sustainability by using the constraints of the carbon budget within the EU.

A new set of measures needs to be put in place to give road transport policy a clear direction. The main barrier to carbon emission reduction is the absence of a market that can accelerate change towards a low carbon or a net-zero transport system. At this stage, the EU is making progress but is still heavily dependent on diesel and gasoline. Although Germany, the Netherlands and France are well positioned to reduce road transport carbon emissions, to meet the challenges of the climate change scenarios, the European Commission needs to modernise road transport policy, outperform the BEV competition and overcome the technological barriers in the ICE and EV market within the next decade.

This entry is adapted from the peer-reviewed paper 10.3390/app11167601