Your browser does not fully support modern features. Please upgrade for a smoother experience.

Please note this is an old version of this entry, which may differ significantly from the current revision.

Subjects:

Computer Science, Information Systems

The energy sector is undergoing a period of technological transformation, driven by the emergence of blockchain and smart contracts. These technologies have the potential to revolutionize energy markets and significantly reduce transaction costs, improve efficiency, and increase transparency. The rising energy prices in recent years have been a cause for global concern. The prospects of incorporating smart contracts and blockchain technology into the energy sector are promising.

- blockchain

- smart contracts

- energy sector

1. Introduction

Rising energy prices in recent years have been a cause for global concern. In 2022, the EU recorded historically high energy prices, according to the EU Council. This price surge is attributed to an increased demand for energy following the COVID-19 pandemic, the war in Ukraine, and the acceleration of climate change. In 2022, Russia’s decision to suspend gas supplies to most EU member states increased gas and electricity prices in the EU. As an example, between January 2021 and January 2023, domestic industrial energy producer prices increased by 127% while consumer prices increased by 63.5%. Considering the high volatility of energy prices, as well as the fact that the energy sector is undergoing a period of digital transformation, blockchain technology and smart contracts potentially offer the ability to revolutionize the energy sector by providing a secure, transparent, and efficient platform for energy transactions. Blockchain is a distributed ledger technology that enables peer-to-peer (P2P) transactions with no central authority or intermediary oversight body [1].

This technology can be used both to support complex energy transactions between consumers and energy producers and to develop new business models such as peer-to-peer energy transactions [2].

The use of blockchain in the energy sector has been gaining momentum in recent years due to its ability to provide secure, transparent, and efficient transactions. Energy companies can reduce costs associated with traditional energy trading processes, such as transaction fees and administrative costs [3]. Furthermore, blockchain technology can help to improve the accuracy and reliability of energy data, which can lead to better decision-making and improved customer service [4].

Blockchain technology can also provide increased security for energy transactions. By using cryptographic algorithms, blockchain technology can ensure that only authorized users have access to energy data and transactions [5]. Consequently, it helps protect against cyber-attacks and other malicious activities by providing an unalterable record of energy transactions, which contributes to fraud and manipulation prevention [6].

Beyond the technological benefits, on a business level, blockchain technology can also enable the development of new business models in the energy sector. For example, it can enable P2P energy trading, that is, the ability for consumers to buy and sell energy directly from and to each other without the need for an intermediary. This could potentially lead to lower energy prices and more efficient energy markets [7].

2. Blockchain Technology

Blockchain technology refers to the sum of emerging techniques, processes, and methods that have revolutionized digital transactions, and are radically transforming not only existing business models but also the way that data, goods, and services are exchanged. It is a distributed ledger technology that captures and stores data in a decentralized and immutable format, secured using cryptographic algorithms [8].

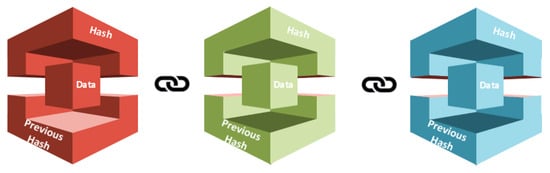

The birth of blockchain technology can be traced back to Satoshi Nakamoto’s 2008 white paper [9] which proposed a decentralized digital currency system using a peer-to-peer network to record and verify transactions. Valid or verified transactions are stored as blocks or lists of transactions linked to the previous transaction. When a new block is created, the hash value of the previous block is inserted into it (Figure 1). In this way, any changes to a previous block result in a different hash code in the immediately following block and are therefore immediately visible to all participants in the chain.

Figure 1. Blockchain with random numbers of blocks.

This property is referred to in the literature as data file immutability, where the recorded data cannot be modified after being accepted by the blockchain network [10]. Due to these characteristics, blockchain technology has become the underlying technology for many digital transactions, including cryptocurrencies and smart contracts [11].

3. Smart Contracts

A smart contract is a digital protocol intended to make it easier to verify or enforce the negotiation or execution of a contract. Smart contracts enable reliable transactions to be executed without the involvement of third parties. These transactions are traceable and irreversible. According to Szabo [12], “a smart contract is a set of promises specified in digital form, including the protocols within which the parties execute those promises”.

It is usually encoded in a language based on Blockchain technology, such as Solidity https://soliditylang.org/ (accessed on 23 November 2023), Vyper https://docs.vyperlang.org/en/stable/ (accessed on 23 November 2023), Cairo https://www.cairo-lang.org/ (accessed on 23 November 2023), Rust https://www.rust-lang.org/ (accessed on 23 November 2023), etc., and stored and replicated in a distributed ledger system. The basic structure of a smart contract consists of an initiation event and a set of rules or terms of the contract. The initiating event is the action or event that triggers the smart contract, such as the arrival of a specific date or an incoming payment. Conditions are the requirements that must be met for the smart contract to be executed [13]. The set of rules or terms of the contract are the instructions to be followed, such as transferring of assets or the provision of services.

Several blockchain platforms leverage smart contracts to facilitate decentralized and automated processes. Ethereum, a pioneering platform, introduced smart contracts, enabling trustless and transparent execution of code for various applications, from decentralized finance (DeFi) to non-fungible tokens (NFTs). Binance Smart Chain (BSC), an Ethereum-compatible alternative, emphasizes fast and cost-effective transactions, making it popular for DeFi projects. Polkadot, a multi-chain network, employs smart contracts through its parachain structure, fostering interoperability and scalability. Tezos stands out for its self-amending blockchain and on-chain governance, providing a platform for smart contract deployment. Cardano incorporates smart contracts for secure and scalable decentralized applications. Solana focuses on high-performance blockchain, utilizing smart contracts for decentralized applications with low transaction costs. These platforms showcase the diverse landscape of technologies utilizing smart contracts, each contributing unique features to the broader blockchain ecosystem. Some use cases of smart contracts are automated insurance claims [14], supply chain management [15], real estate transactions [16], voting and election system [17], crowdfunding [18], cloud storage [19], healthcare records [20], copyright protection [21], online purchases [22], loan management [23], and energy trading [24], where smart contracts can be used to automate the energy trading process and ensure that all parties adhere to the terms of the agreement.

This entry is adapted from the peer-reviewed paper 10.3390/app14010253

This entry is offline, you can click here to edit this entry!