Your browser does not fully support modern features. Please upgrade for a smoother experience.

Please note this is an old version of this entry, which may differ significantly from the current revision.

Subjects:

Green & Sustainable Science & Technology

The current study investigates the impact of decarbonisation policies on the EU’s building stock, with a specific focus on Minimum Energy Performance Standards (MEPS), the new Emissions Trading System (ETS2) for buildings, and the phase-out of fossil heating systems.

- energy policy

- EU Emissions Trading System

- fossil fuel boiler phase-out

1. Introduction

Europe’s most important and threatening crisis is climate change affecting different sectors in different ways, posing uncertainties regarding the continent’s future. The reduction in greenhouse gas (GHG) emissions simultaneously requires higher implementation of renewable energy sources (RES) and an improvement in energy efficiency. Buildings account for more than 40% of final energy consumption and at least 36% of energy-related GHG emissions [1]. Therefore, there is a need for renewable and less polluting energy systems for domestic and public buildings. This will result not only in the reduction in GHG emissions but also in the promotion of energy saving, tackling energy poverty, improving health and well-being, as well as creating new opportunities for growth and work. Most EU countries present low levels of energy efficiency in the residential sector due to the ageing of the buildings and the lack of renovation strategies in the last years. Hence, measures promoting the energy efficiency of dwellings in the residential sector must be advanced. This is also illustrated by the Energy Efficiency First (EE1st) principle, part of Article 3 of the new Energy Efficiency Directive (EED) recast proposal, and it “means taking utmost account of cost-efficient energy efficiency measures in shaping energy policy and making relevant investment decisions” [2]. In practice, the EE1st principle balances demand and supply options in order to prioritise the least expensive investments for the energy system from a societal perspective.

2. Household Energy Efficiency, Energy Poverty and the Relation of These to Low-Income Groups

As recognised in the European Green Deal, 50 million citizens across the European Union (EU) do not have access to indoor thermal comfort [3]. Bouzarovski (2018) [4] (p. 1) defines energy poverty as a situation which “occurs when a household is unable to secure a level and quality of domestic energy services–space cooling and heating, cooking, appliances, information technology–sufficient for its social and material needs”. Nonetheless, various definitions of energy poverty can be found throughout the literature. This can be traced back to its multifaceted nature, as energy poverty is a socioeconomic issue that presents many ramifications. For this reason, definitions vary also across countries, dictated by national socioeconomic conditions which play an important role in defining energy poverty. Within the EU, not all nations present an official, legally recognised definition. Additionally, energy poverty is unevenly distributed across Europe, with eastern and southern regions presenting higher prominence of the latter [5]. This is also due to the environmental and geographical factors of one location which will inevitably affect its vulnerability to energy poverty [4]. Nonetheless, it is agreed within the literature that this intricate phenomenon will always include both economic components, such as the fuel prices, and energy components, such as the energy performance of the dwelling where one household lives, and all the socioeconomic interactions that can result, such as the inability to keep the home adequately warm. The importance of energy performance is enhanced trough regulation and existing building codes [6]. However, this phenomenon does not have only socioeconomic ramifications but, for example, also environmental ones. Indeed, households in a situation of energy poverty will utilise more outdated forms of technology for energy consumption, resulting in more environmental harm.

Energy poverty is closely related to household energy efficiency [7], with the latter being defined as the needed energy to power one household to generate a certain energy output [8]. Improving energy efficiency in general is one of the main objectives of the European Green Deal, with a set target of achieving at least 36% in energy efficiency by 2030 [9]. Energy refurbishments of buildings could reduce energy poverty and concurrently increase household energy efficiency [10]. In fact, measures aimed at tackling energy poverty from the demand side have the potential to alleviate energy poverty while providing direct and tangible benefits to the residents [11]. In addition, greenhouse gas emissions, total energy consumption, and consequently energy expenditures could be lessened [10]. Nations that present a higher range of low-quality and energy-inefficient dwellings tend to present higher levels of energy poverty (and vice versa) [12]. In fact, higher expenditures will result from more inefficient buildings (e.g., low thermal insulation). Another correlation that is found is that residents living in energy inefficient households present below-average disposable incomes [12]. In a similar way, low-income groups are more probable to become energy poor [13] to the extent that the gravity of one household’s energy burden is often considered as a solid predictor of which groups will be affected by energy poverty [11]. For this reason, this particular segment of society was the focus of the present study.

An extensive array of studies has been undertaken to thoroughly examine the multifaceted factors that contribute to the pervasive issue of energy poverty. These meticulous investigations delve into crucial aspects such as financial market participation, energy efficiency, and the significance of human capital. By delving into these critical dimensions, these studies provide invaluable policy insights that not only shed light on the root causes of energy poverty but also offer practical recommendations to address and overcome this pressing challenge.

Among these studies, Cheng et al. [14] conducted an insightful investigation on the impact of financial market participation on household energy poverty. Using data from the 2015 Chinese General Social Survey, their findings suggest that engaging in financial markets significantly reduces energy poverty, primarily through the mediation of future expectations. However, the study also reveals that higher financial risk weakens the effect of future expectations on energy poverty by destabilising household finances. Consequently, promoting financial market participation emerges as a potential avenue for alleviating household energy poverty.

Another noteworthy study by Moteng et al. [15] explores the mechanisms through which sanctions affect energy poverty, highlighting the significance of factors such as human capital, energy efficiency, income inequality, and economic growth. By identifying these interconnected mechanisms, the study offers valuable policy insights that can inform policymakers in designing effective strategies and interventions to tackle energy poverty.

Collectively, these studies contribute to a robust foundation of knowledge for policymakers, enabling them to devise and implement targeted strategies, programs, and interventions that can effectively alleviate energy poverty and improve the overall well-being of affected communities.

3. Delineation, Explanation, and Selection of the Case Studies

The present research analyses seven countries from central and southern Eastern Europe, as these two regions were found to be particularly characterised by energy poverty. Eastern European states are additionally affected by a late liberalisation of the energy market, a historically unstable energy supply mix, and inefficient thermal insulation of buildings [5]. The countries analysed include Bulgaria, Czechia, Greece, Hungary, Poland, Romania, and Slovakia. As most EU member states, they opted to alleviate the higher burden of energy costs with price regulations, energy bill assistance, as well as tax reductions on the energy bills. Nevertheless, these are not considered as structural measures for the low-income groups and thus should be combined with energy efficiency upgrades and measures for decarbonising the space heating facilities. Moreover, the higher upfront costs of energy efficiency investments combined with the well-known and documented structural barriers do not make energy efficiency a key priority of low- and middle-income groups, notwithstanding the shortened payback period of these investments due to the higher energy prices. The households’ reduced disposable income (due to the higher energy prices) is hampering the possibility of investment in refurbishments and clean heating solutions, while the incumbent fossil fuel subsidies further delay such investments. Therefore, if the available funding, such as subsidies on energy efficiency and heat pumps, is not increased for the low-income households, the energy crisis and inflation may even delay energy efficiency investments to remove fossil-fuel-heating in such households. Hence, to counter such trend, a complementary package of supporting measures which includes financial, informational, and technical measures from the national and local authorities is needed to help accelerate energy efficiency investments and finally switch to clean and sustainable space heating.

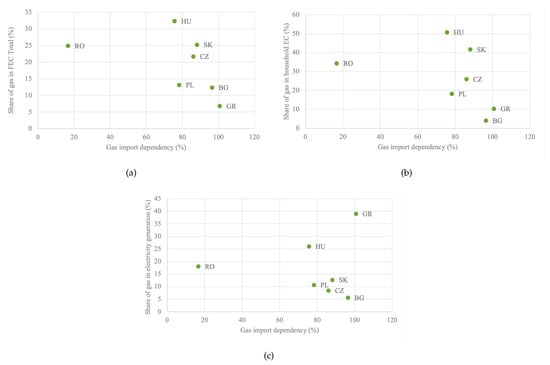

An interesting aspect to consider is the country’s dependence on imported gas and the share it has in its final energy consumption and other energy end-uses. The dependence on imported gas influences the energy price, and with it, the member states’ new expenditures to cover the energy costs of households via bill aid. Various figures related to gas utilisation in the considered countries are presented in Table 1. In addition to the analysed countries, France and Germany, Europe’s richest countries, are also presented in this table. This is done to see the extent to which economic and geographic indicators play a role. It can be seen how Romania presents the lowest dependency on Russian gas (even lower than France and Germany). Interestingly, Bulgaria is the only country presenting a lower gas share when considering only household energy consumption rather than the total final energy consumption. This table shows how every country’s data in relation to natural gas is unique and how data cannot be easily generalised. With regards to electricity generation, Greece stands out with almost 40% of gas share in its electricity production. Stemming from this data, various scatterplots relating to general gas import dependency and the different gas shares per end-use were delineated for the analysed countries (Figure 1).

Figure 1. Comparing graphically the dependence on gas per energy end-use per country compared to its gas import dependency. (a) Share of gas in final energy consumption compared to gas import dependency. (b) Share of gas in household energy consumption compared to gas import dependency. (c) Share of gas in electricity generation compared to gas import dependency.

Table 1. Comparing graphically the dependence on gas per energy end-use per country compared to its gas import dependency.

| Countries | Bulgaria | Czechia | Greece | Hungary | Poland | Romania | Slovakia | France | Germany |

|---|---|---|---|---|---|---|---|---|---|

| Dependency on Russian gas [16] | 77% | 92% | 40% | 64% | 48% | 22% | 65% | 24% | 60% |

| General gas import dependency [17] | 96% | 86% | 100% | 76% | 78% | 17% | 88% | 95% | 89% |

| Gas share in FEC [18] | 12% | 22% | 7% | 32% | 13% | 25% | 25% | 21% | 27% |

| Gas share in household EC [19] | 4% | 26% | 10% | 51% | 18% | 34% | 42% | 28% | 38% |

| Gas share in electricity generation [20] | 6% | 8% | 39% | 26% | 11% | 18% | 13% | 6% | 16% |

The scatterplots illustrate how big of a role gas plays in the energy consumption of the analysed countries and how dependent the latter are from gas-exporting partner countries. Firstly, it can be noticed how Romania can “afford” to have rather high gas consumption patterns as it imports a rather small percentage of its consumed gas. On the other hand, the country presenting the highest gas import dependency, Greece, is particularly reliant on partner countries as it produces a high proportion of its electricity from gas. Thus, even though Greece has rather low consumption patterns of gas, it is still the most gas-reliant of the analysed countries due to its high share of gas in electricity generation. Bulgaria also presents high gas import dependency; nonetheless, unlike Greece, it utilises a very small percentage of gas, and thus is not deemed as a very gas-reliant country. Poland is also another country not too reliant on gas, however on a minor scale. The other analysed countries, and in particular Hungary, can all be defined as gas-reliant.

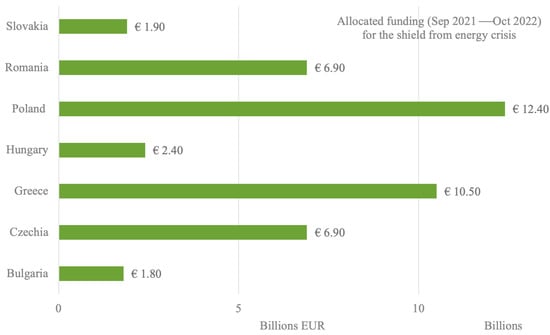

On another note, Figure 2 shows the allocated funding (in billion EUR) in each country for tackling the energy crisis between September 2021 and October 2022. The burden on state budgets will strongly affect the possibility of member states implementing low-carbon policies. Therefore, strategic planning to develop complementary policies is of the highest relevance. Poland presents the highest budget, as expected from the largest of analysed countries both demographically and economically. Surprising is perhaps Greece, which presents the second highest budget even though having a lower economic force compared to other countries. The rest of the analysed countries seem to have an allocated budget that reflects their socioeconomic conditions.

Figure 2. Governments earmarked and allocated funding (September 2021–October 2022) to shield households and businesses from the energy crisis [21].

The presented data aimed to reflect that each country presents unique gas-related characteristics with different allocated budgets. A generalisation of such starting characteristics for central and southern Eastern European nations is thus not possible. Hence, each country will be analysed on its own and only once national results are obtained will these be analysed together, considering the hereby described national characteristics.

4. European Energy Policy Framework

The EU aims to be the first continent with neutral carbon emissions by 2050 and has been at the forefront of the promotion and implementation of decarbonisation policy measures [9]. As part of this effort is the European Green Deal, which “aims to transform the EU into a fair and prosperous society, with a modern, resource-efficient and competitive economy where there are no net emissions of greenhouse gases in 2050 and where economic growth is decoupled from resource use” [3] (p. 2). The proposed policy mix focuses on three key principles related to energy. Firstly, to ensure an affordable, clean, and secure EU energy supply. Secondly, to prioritise the renovation and improvement of buildings in a resource and energy-efficient way. Thirdly, to develop a fully digitalised, and interconnected EU energy market, promoting circular economy [3].

Part of the European Green Deal is the “Fit for 55” package. This set of policy proposals also includes revisions of previous directives, such as the EED and Energy Performance of Buildings Directive (EPBD). The name of the package stems from the EU’s objective of reducing by 55% its net greenhouse gas (GHG) emissions by the year 2030 compared to its 1990 levels. To ensure, a competitive and just energy transition by 2030, the package offers a careful combination of pricing, standards, support measures, and targets. Following the breakout of the war in Ukraine, the European Commission fastened its process of independence from Russian fossil fuels and thus, on 18 May 2022, presented the “REPower EU Plan” [22]. The latter foresees reducing dependence on Russian fossil fuel by further increasing some of the objectives set in the Fit for 55 package and fast-forwarding the sustainable transition. For example, the target for the renewable energy share in 2030 was increased from 40% to 45%, envisioning a doubled installation rate of heat pumps [22]. For the present research, three specific policy measures (present in the Fit for 55 package) were chosen to be analysed, simulated, and discussed. These will be further described in the following paragraphs.

4.1. Extension of the EU Emissions Trading System to the Residential Sector

The European Commission developed and put in force the new emission trading system (ETS2 here), which puts numbers on the fossil fuel emissions in buildings and transport sectors. It is a cap-and-trade kind of system like the ongoing ETS. It is regulated upstream, it does not directly involve buildings or vehicles but fuel suppliers, and will begin in 2026. These sectors will still be covered by the Effort Sharing Regulation, meaning member states’ policies will continue to contribute to reducing emissions in the sectors. Carbon pricing is the measure that creates the market for new innovations, but the degree of this depends on (a) energy price elasticities and (b) cross-price elasticities. The impacts of the ETS price in these sectors could however generate higher costs to households, hence leading to higher energy poverty, in central and southern Eastern Europe.

4.2. Phasing out of Fossil Fuel Boilers

To enable the decarbonisation of space heating and cooling in the households, the installation or sale of new fossil fuel boilers is to be phased out by 2030, plus the fossil fuel boiler lifetime. This might create a lock-in effect for households that are in the situation of energy poverty. They will use cheaper technologies due to the fact that more advanced technologies like heat pumps have higher upfront costs, despite their operational and ongoing costs being lower. To secure the avoiding of a lock-in is a policy framework that can give low-income households the possibility to switch to low-carbon heating systems. A revision of the Ecodesign and energy labelling regulation for heaters is going to lead to a downgrading of gas boilers to the low-energy (the two lowest) labels and more interest in the phase-out of the inefficient heating systems. A previous study from [23] announced that governments choose (a) natural gas for space heating, enlarging existing gas pipelines in the domestic sector, and (b) make use of subsidies for fossil fuel heating with the gas boilers, considering it an energy efficiency measure. The phasing out of fossil fuel boilers should indicate a clear timeline to avoid lock-ins and increase the costs of shifting to natural gas boilers.

4.3. Minimum Energy Performance Standards (MEPS)

Minimum Energy Performance Standards (MEPS) target buildings with renovations aimed at improving the energy efficiency in the residential sector reducing energy poverty, taking into account possible socio-economic differences. The EPBD recast [24] announced that the minimum energy performance standards shall at least ensure that all non-residential buildings are below (i) the 15% threshold as of 1 January 2030 and (ii) the 25% threshold as of 1 January 2034. The trajectory is expressed as a decrease in the average primary energy use in kWh/(m2y) of the whole residential building stock over the period from 2025 to 2050. The average primary energy use in kWh/(m2y) of the whole residential building stock needs to be at least equivalent to:

- (a)

-

The D energy performance class level by 2033;

- (b)

-

By 2040, a nationally determined value derived from a gradual decrease in the average primary energy use from 2033 to 2050 in line with the transformation of the residential building stock into a zero-emission building stock. Although evidence of the impacts of MEPS is not yet available, there was an impact assessment of the EPBD with the result that MEPS is a crucial instrument for the final energy savings and for the cost reduction, as well as for generating construction activity. The impact assessment did not isolate the impacts of MEPS on energy poverty nor did it address specificity regarding the central and southern Eastern European regions.

This entry is adapted from the peer-reviewed paper 10.3390/en16145443

This entry is offline, you can click here to edit this entry!