Your browser does not fully support modern features. Please upgrade for a smoother experience.

Please note this is a comparison between Version 2 by Catherine Yang and Version 1 by Vladimira Binasova.

In the pursuit of economic survival in the current competitive conditions with the aim of long-term prosperity and sustainability in the market, many companies today approach significant strategic changes in the management of their business. The design of a systematic procedure for implementing strategy changes into internal business processes for a project-oriented production type of organization is of importance.

- advanced industrial engineering

- strategy

- management

- business processes

- business performanc

1. Introduction

Due to the constant growth of input costs (personnel costs, energy, input materials, etc.), many Slovak companies have found themselves in this difficult position, having to wage tough competitive battles both on domestic and global markets. Competitive advantage can be created by free disposable capital, a traditional position on the market, or long-term management experience; above all, you need the ability to use radical innovation of internal processes, tools for managing these processes, and online monitoring of selected parameters as a very effective weapon.

The key to success is not the micro-management of individual operations, but focusing on the main internal processes in the company in such a way that improvements can be achieved in terms of critical weight of performance; these include costs, quality, services, deadline fulfilment, and above all, orientation to the customer and their problems and the challenges it encounters in the implementation of its business models.

The company’s strategy guides all management decisions from the front line. Strategic plans act as a road map that helps businesses achieve the big vision of their owners and top managers in practical ways. A change in an organization’s strategy can change the way an organization operates, changing everything from the organizational structure to the daily routines of employees. When changing the strategy, it is vitally important to realize the individual correlations between the sub-strategies themselves and the internal processes. Not all effects of change are positive. Internal employee resistance can be a ma-jor obstacle to effective change implementation, as some people strongly resist any kind of change to the status quo or daily routine. There is also always the possibility of failure in new initiatives, leaving the company in a worse position than it was before the change.

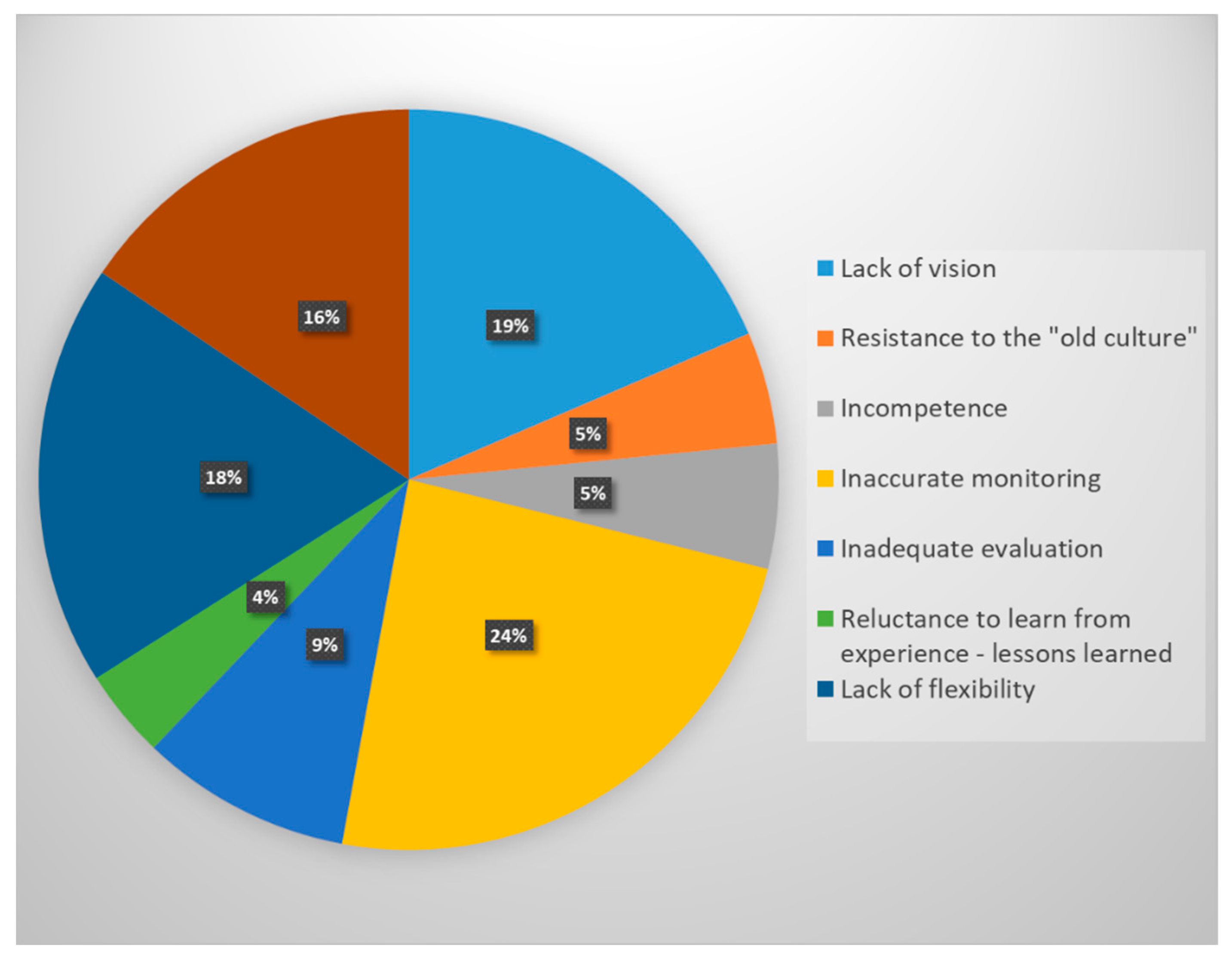

Fundamental factors that fatally affect the success of implementing strategy changes into internal company processes have been identified. A survey of 100 manufacturing companies in the Slovak Republic revealed the following factors (Figure 1).

Figure 1.

The fundamental factors that fatally affect the success of implementing strategy changes into internal company processes.

A project-oriented production organization that pursues a single goal, namely the successful implementation of individual projects in terms of costs, meeting deadlines, covering overheads, and of course, expected profitability. With the successful implementation of individual projects and the non-exceeding of individual budgets in the administration departments, the continuous fulfilment of the relevant business plan of the company in the relevant year is also guaranteed. The preparation process of internal process changes in view of the company’s changing strategy consists of several parts that are essentially independent, but mutually connected (see Figure 2).

Figure 2.

The relationship between strategic plan changes and process change.

A change in a strategic plan is a change that is based on the results of strategic planning, and forecasting is a result of technical forecasts. In this process, the healthy core of the company must be used as a basis for achieving set goals, supporting strategy creation, and defining priority changes in internal processes. The process of changing internal processes due to changes in the company’s strategy is divided into two phases: design of changes (concept, plan); and implementation of changes. The proposal is the beginning of the change process and contains the position of the project in the company, value indicators, and also all managerial, operational, social and technological changes. Implementation is a process in which we develop plans for internal process changes that are gradually implemented, and at the same time they are monitored, evaluated and corrected with appropriate measures.

2. Background

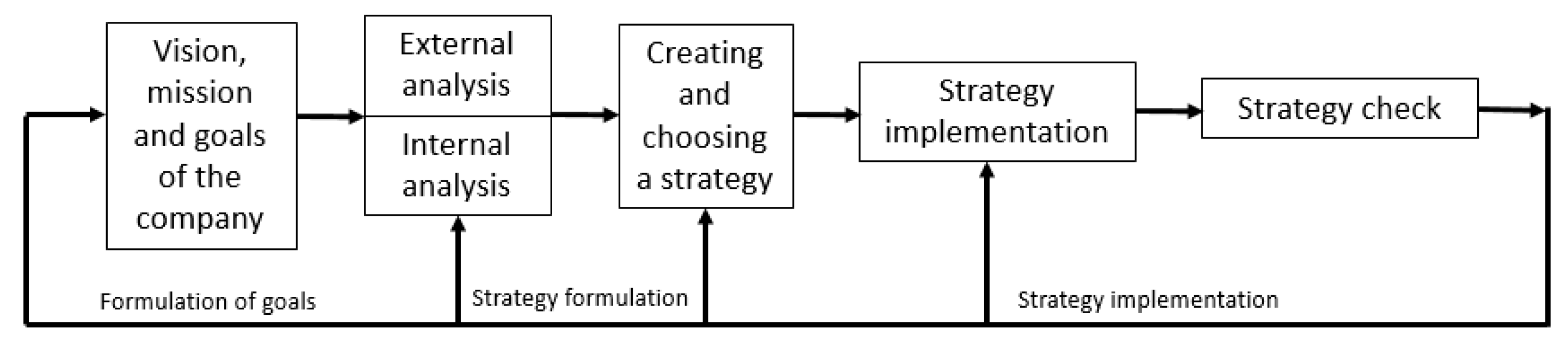

Digital transformation reveals new ways for an organization to stay in touch with customers and consumers and thus create value for them [1]. Most consumers behave subconsciously or unconsciously [2]. Marketers try to understand how individual features of a product contribute to the overall evaluation [3]. Today, most authors and managers consider strategic management to be a complex, internally structured, and continuous process [4,5][4][5]. A simple model of strategic management was presented in his work by [6] considering the continuity of the basic phases. It is possible to state that strategic management is an iterative process, gradually passing through individual phases and their steps; a process that is constantly and continuously ongoing. Automotive and component manufacturing companies form a tandem of recognized prestige in terms of competitiveness and results [7]. Strategic management integrates multiple procedures and analyses which evaluate the organization’s results and adapts them to changes in the external environment. It is a relatively complex process that involves several managers in the organization and affects the actions of all employees [6]. The rapid progression of globalisation has driven companies to search for new approaches to improve their performance by producing products at a much lower cost, timelier and with superior quality [8]. The identification of research gaps from systematic reviews is essential to the practice. It is important to address that business process management will continue to be a crucial tool for any organization that is trying to improve its operations. New technologies will emerge providing new opportunities to obtain automational effects, informational effects, and transformational effects. The key question is: “How will digitisation change jobs and work profiles?” The authors of [9] claim their analysis as follows: The extent of computerisation in the twenty-first century will thus partly depend on innovative approaches to task restructuring. Restructuring tasks, and more broadly operations, are exactly what BPM is concerned with [10] in his study, concluding that business process management is developing a stronger strategical perspective which has the potential to support digital strategies of customer engagement and digitized solutions. Figure 3 below describes the steps of the strategic management process as a continuous process.

Figure 3.

Steps of strategic management.

The Management of Change

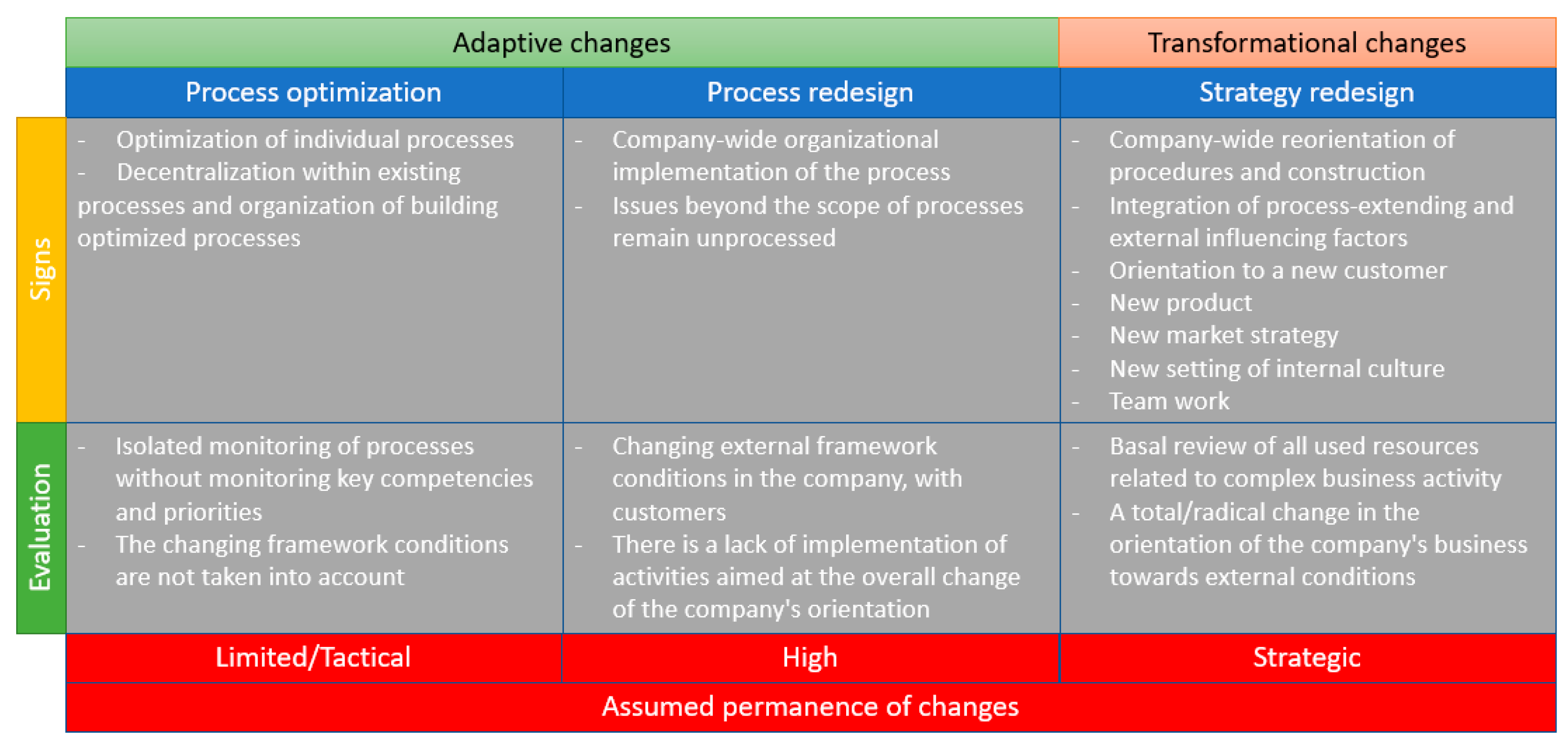

The driving force behind changing a company’s strategy is always the desire to move the company to a higher level or improve its economic results. An important factor is to realize that a change in internal processes caused by a change in strategy is always a relatively large intervention in the internal functioning of any company. Therefore, it is necessary to focus on a correct and meaningful awareness of what changes need to be made and how to understand these changes in the wider context of all processes in the company. Categorization of changes in internal processes caused by a change in the company’s strategy is a process in which changes can be divided into three basic groups (see Figure 4) according to the severity of the influence of depth on process redesign or adjusting the strategy.

Figure 4.

Essential distribution of changes according to the severity of the impact of process changes.

-

Evaluation of the management result through the income statement, or balance sheets;

- Cost indicators: total cost, personal cost.

-

Economic value added—EVA (Economic Value Added);

-

Value added by the market—MVA (Market Value Added);

-

Added value for shareholders—SVA (Shareholder Value Added);

-

Profitability of net assets—RONA (Return of Net Assets) and others.

3. The Impact of Strategy Change on Business Process Management

Modern business organizations face dynamic changes in their management environments, and many firms actively consider adopting information technology (IT) to adapt to these changes [34]. Every company management in this hectic time faces the challenge of maintaining stability and achieving a certain level of predictability of the company’s performance [35,36,37,38,39][35][36][37][38][39]. To meet new challenges and business interests organizations must constantly monitor, evaluate and adjust their strategic initiatives. When a new strategy needs to be implemented [40], it is usually up to managers to ensure its successful implementation. Information on how to successfully implement strategic change into processes usually contains several step-by-step procedures that are very general. The subject of the investigation was the realization of how the change affects the strategy and internal processes of the organization. This is done by describing what change is, discussing categories of change, external drivers of change, and perceptions of change initiatives as negative or positive [30,31][30][31]. The consequences of changes in strategy can take many forms: for example, it brings different challenges to different people depending on their position in the organizational hierarchy. Research on the impact of strategy changes has shown that strategy change is a process that relates to the overarching goals and objectives of a business. Strategic decisions influence which business area the company operates in and for whom it benefits. It is also important how the company functions internally and what factors influence changes in the internal process (Table 1). It is very difficult to predict exactly what will happen when an organization changes its strategy, but companies experience several common positive and negative effects when they undergo a strategic transformation.Table 1.

Factors affecting/not affecting the success of internal process change.

| Factors Affecting the Success of Internal Process Change: | Factors Not Affecting the Success of Internal Process Change: |

|---|---|

|

- ]]

|

- [

- 30]

|

- [

|

- Indicators resulting from the company’s financial statements;

- Activity indicators: inventory turnover time, debt collection time, liability maturity date, total asset turnover;

- Liquidity indicators: immediate liquidity, current liquidity, total liquidity;

-

Indebtedness indicators: total indebtedness, self-financing coefficient, credit indebtedness;

-

Profitability indicators: profitability of total assets (ROA), the profitability of equity (ROE), the profitability of sales, the profitability of costs, return on investment (ROI);

- Market value indicators: profit per share, dividend yield;

Figure 5.

The status of the enterprise and the target state of the change.

References

- Lemon, K.N.; Verhoef, P.C. Understanding Customer Experience throughout the Customer Journey. J. Mark. 2016, 80, 69–96.

- Alsharif, A.H.; Md Salleh, N.Z.; Khraiwish, A. Biomedical Technology in Studying Consumers’ Subconscious Behavior. Int. J. Online Biomed. Eng. 2022, 18, 98–114.

- Mendling, J.; Dumas, M.; La Rosa, M.; Reijers, H.A. Structuring Business Process Management. In The Art of Structuring; Springer: Cham, Switzerland, 2019; pp. 203–211.

- Sakál, P. Strategický Manažment, 1st ed.; Vydavateľstvo STU: Bratislava, Slovakia, 2004; ISBN 80-227-2153-0.

- Slávik, Š. Strategický Manažment; Sprint 2: Bratislava, Slovakia, 2005; ISBN 8089085490.

- Thomas, L.W.; Hunger, J.D. Strategic Management and Business Policy: Toward Global Sustainability; Pearson Learning Solutions: Boston, MA, USA, 2012.

- Miguel PM, D.; De-Pablos-Heredero, C.; Montes, J.L.; García, A. Impact of Dynamic Capabilities on Customer Satisfaction through Digital Transformation in the Automotive Sector. Sustainability 2022, 14, 4772.

- Md Hanafiah, R.; Karim, N.H.; Abdul Rahman NS, F.; Abdul Hamid, S.; Mohammed, A.M. An Innovative Risk Matrix Model for Warehousing Productivity Performance. Sustainability 2022, 14, 4060.

- Frey, C.B.; Osborne, M.A. The future of employment: How susceptible are jobs to computerisation? Technol. Forecast. Soc. Chang. 2017, 114, 254–280.

- Sebastian, I.M.; Ross, J.W.; Beath, C.; Mocker, M.; Moloney, K.G.; Fonstad, N.O. How big old companies navigate digital transformation. In Strategic Information Management; Routledge: London, UK, 2020; pp. 133–150.

- Fotr, J.; Vacík, E.; Souček, I.; Špaček, M.; Hájek, S. Tvorba Stratégie a Strategické Plánování; Grada Publishing: Praha, Czech Republic, 2012; ISBN 978-80-247-3985-4.

- Antošová, M. Strategický Manažment a Rozhodovanie; IURA EDITION: Bratislava, Slovakia, 2012; ISBN 978-80-8078-530-7.

- Quesado, P.; Marques, S.; Silva, R.; Ribeiro, A. The Balanced Scorecard as a Strategic Management Tool in the Textile Sector. Adm. Sci. 2022, 12, 38.

- da Costa Ferreira, A.M.S. How managers use the balanced scorecard to support strategy implementation and formulation processes. Tékhne 2017, 15, 2–15.

- Gomes, P. Tékhne—Review of Applied Management Studies. Tékhne 2012, 10, 1–2.

- Ferreira, A. Sistemas de medição do desempenho e o Balanced Scorecard. Contabilidade e Controlo de Gestão: Teoria, Metodologia e Prática; Escolar Editora: Lisbon, Portugal, 2009; pp. 301–332.

- Yancy, A.A. Who Adopts Balanced Scorecards? An Empirical Study. Int. J. Bus. Account. Financ. 2017, 11, 24–37.

- Asadpourian, Z.; Rahimian, M.; Gholamrezai, S. SWOT-AHP-TOWS Analysis for Sustainable Ecotourism Development in the Best Area in Lorestan Province. Iran. Soc. Indic. Res. 2020, 152, 289–315.

- Kaymaz, C.K.; Birinci, S.; Kizilkan, Y. Sustainable development goals assessment of Erzurum province with SWOT-AHP analysis. Environ. Dev. Sustain. 2022, 24, 2986–3012, Erratum in Environ. Dev. Sustain. 2022, 24, 3013.

- de Alcantara, M.S.N.; de Lucena, R.F.P.; da Cruz, D.D. Toward sustainable production chain by SWOT-AHP analysis: A case study of Fava d’anta (Dimorphandra gardneriana Tulasne) production chain. Environ. Dev. Sustain. 2022, 24, 2056–2078.

- Brunnhofer, M.; Gabriella, N.; Schöggl, J.-P.; Stern, T.; Posch, A. The biorefinery transition in the European pulp and paper industry—A three-phase Delphi study including a SWOT-AHP analysis. For. Policy Econ. 2020, 110, 101882.

- Cui, F.; Lim, H.; Song, J. The Influence of Leadership Style in China SMEs on Enterprise Innovation Performance: The Mediating Roles of Organizational Learning. Sustainability 2022, 14, 3249.

- Dhaifallah, B.; Sofiah, A.; Ruhanita, M. The moderating role of employees’ professionalism on BSC usage and organizational performance relationship. Asian J. Account. Gov. 2018, 10, 135–143.

- Kaplan, S.R.; Norton, D.P. Transforming the balanced scorecard from performance measurement to strategic management: Part 1. Account. Horiz. 2001, 15, 87–104.

- Quesado, P.R.; Guzman, B.A.; Rodrigues, L.L. Determinant Factors of the Implementation of the Balanced Scorecard in Portugal: Empirical Evidence in Public and Private Organizations. Rev. Bras. Gestão Negócios 2014, 6, 199–222.

- Russo, J. Balanced Scorecard Para PME, 2nd ed.; Lidel Edições Técnicas: Lisboa, Portugal, 2006.

- Hugues, J.; Neves, J.; Rodrigues, J. O Controlo de Gestão ao Serviço da Estratégia e dos Gestores, 9th ed.; Áreas Editora: Lisboa, Portugal, 2011.

- Konečný, M.; Gregušová, M. Strategický Management, 1st ed.; VŠB—Technická Univerzita Ostrava: Ostrava, Czech Republic, 2012; 287p, ISBN 978-80-248-2791-9.

- Papula, J.; Papulová, Z.; Paula, J. Strategický Manažment; Wolters Kluwer: Bratislava, Slovakia, 2019; ISBN 978-80-7598-535-4.

- Ohmae, K. The Mind of the Strategist. The Art of Japanese Business; McGraw-HILL: New York, NY, USA, 1982.

- Zikmund, M. Management by Objectives (MBO) Aneb Řiďte své Podřízené Podle Druckera . 2011. Dostupné z. Available online: https://www.2leadership.org/glossary/management-by-objectives/ (accessed on 26 July 2022).

- Grznár, P.; Gregor, M.; Krajčovič, M.; Mozol, Š.; Schickerle, M.; Vavrík, V.; Ďurica, L.; Marschall, M.; Bielik, T. Modeling and simulation of processes in a factory of the future. Appl. Sci. 2020, 10, 4503.

- Donoghue, I.D.; Hannola, L.H.; Papinniemi, J.J. Product lifecycle management framework for business transformation. LogForum 2018, 14, 293–303.

- Park, K.O. The relationship between BPR strategy and change management for the sustainable implementation of ERP: An information orientation perspective. Sustainability 2018, 10, 3080.

- Micieta, B.; Durica, L.; Binasova, V. New Solution of Abstract Architecture for Control and Coordination Decentralized Systems. Teh. Vjesn.-Tech. Gaz. 2018, 25, 135–143.

- Malega, P. Riadenie projektu—strategická cesta. In Proceedings of the 15th International Scientific Conference Trends and Innovative Approaches in Business Processes, Košice, Slovakia, 10–11 December 2012.

- Sanele, V.; Stainbank, L.; Nyide, C. The Adoption of Management Accounting Practices by Small and Medium Clothing and Textile Entities in an Emerging Market. J. Manag. Inf. Decis. Sci. 2020, 23, 376–386.

- Micieta, B.; Staszewska, J.; Kovalsky, M.; Krajcovic, M.; Binasova, V.; Papanek, L.; Antoniuk, I. Innovative System for Scheduling Production Using a Combination of Parametric Simulation Models. Sustainability 2021, 13, 9518.

- Robert, Y. Case Study Research Design and Methods; Sage Publications: Thousand Oaks, CA, USA, 2014.

- Zhang, L.; Qi, Y.; Jin, Z.; Xu, J. Do Intellectual Capital Elements Spur Firm Performance? Evidence from the Textile and Apparel Industry in China. Math. Probl. Eng. 2021, 2021, 7332885.

More