Your browser does not fully support modern features. Please upgrade for a smoother experience.

Please note this is a comparison between Version 2 by Amina Yu and Version 1 by Svetlana V. Lobova.

The Sustainable Development Goals (SDGs) are a unique collective agreement of the modern time, which was concluded between government, society, and business at a global scale and which ensures outstanding progress in sustainable development. Society is the direct beneficiary of the SDGs, but bears the lowest expenditures for their implementation and, thus, supports them. The government protects society’s interests, and implementation of the SDGs is among its main responsibilities. Participation of business in the achievement of the SDGs is complex and contradictory, deserving special attention. It is no coincidence that the necessity for the integration of the SDGs into corporate strategies is a part of the agenda in the Decade of Action.

- corporate social responsibility (CSR)

- integration of the SDGs into corporate strategies

1. Introduction

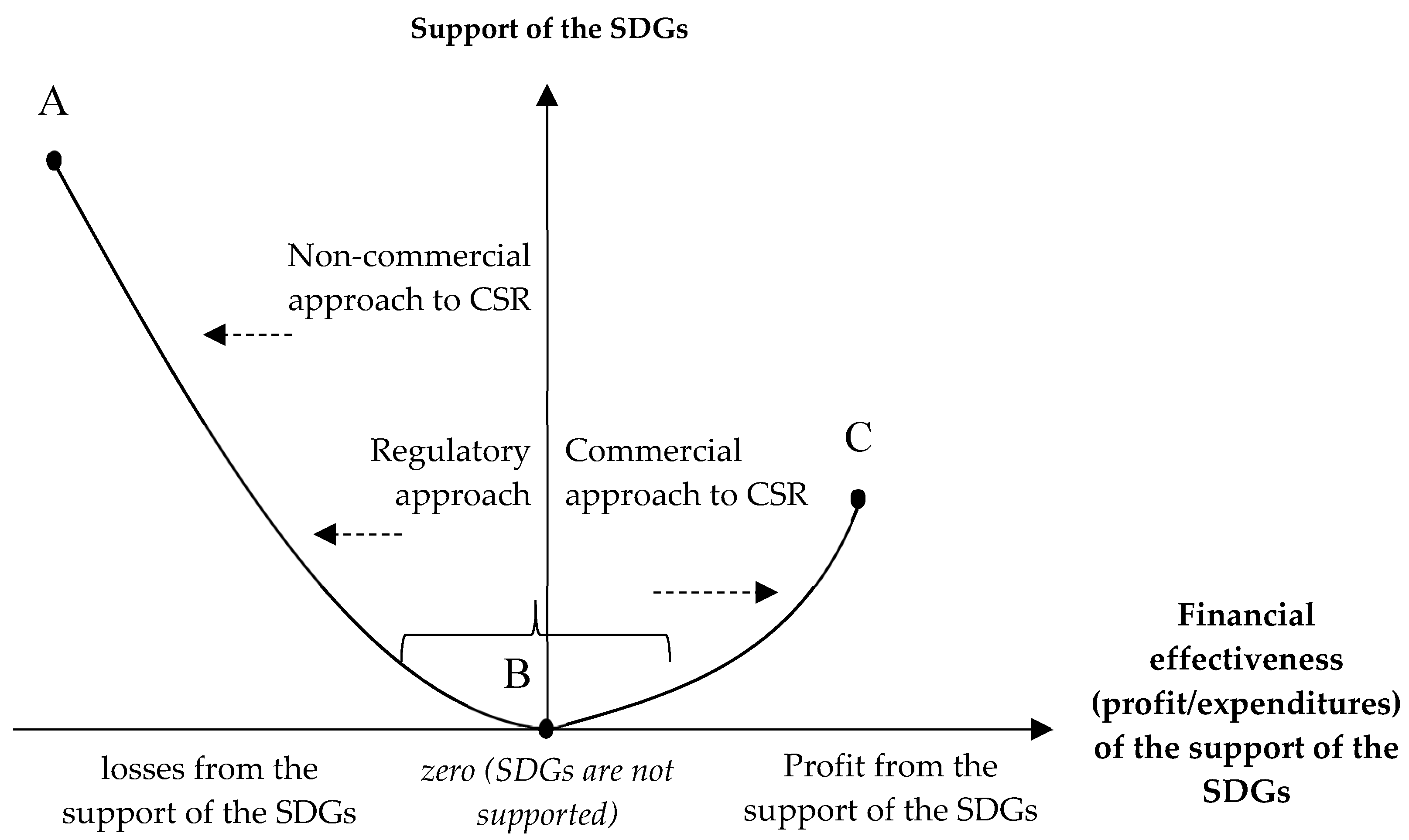

In most csituasetions, support of the SDGs ustainable Development Goals (SDGs) means losses for business (including a shortfall in profits—alternative costs), i.e., contradicts its financial interests. The existing scientific literatureresearch distinguishes three approaches to the integration of the SDGs into corporate strategies. The 1st—regulatory—approach is based on companies’ unpreparedness for voluntary losses, so the implementation of the SDGs is a “market gap”. That is the reason why the government does not provide companies with the choice and opportunity to voluntarily support the SDGs (expecting that this will not take place at the required scale). Instead of this, the government adopts and controls the observation of labour and ecological standards, as well as standards of corporate financial reporting (Batóg and Batóg 2021). On the one hand, this ensures wide support of the SDGs by entrepreneurship, but, on the other hand, government interference with the natural processes distorts the effect of the market mechanism and decreases the effectiveness of entrepreneurship (Hamed et al. 2022; Liu 2021).

The other two approaches are based on corporate social responsibility and are widely studied in the existing literature. A lot of scientific publications are devoted to the research of the interconnection between corporate social responsibility and the indicators of a company’s activity (Fontana 2017; Jaisinghani and Sekhon 2022; Kaul and Luo 2018; Schramm-Klein 2015).

A lot of restudies earches are undertook the testing of the interconnection between corporate social responsibility and the indicators of a company’s activity, including profitability, firm risk, stock liquidity, etc and so on. (Akbar et al. 2021; Gennaro 2021; Zhang et al. 2021; Bednarczyk et al. 2021). Using the existing litonerature, the following two approaches are differentiated by the criterion of the risks of corporate social responsibility for profit.

The 2nd—non-commercial—approach to corporate social responsibility implies that companies have to voluntarily refuse their financial interests in favour of implementing the SDGs and accept high risks for profit. According to this approach, corporate social responsibility is associated with charity. As a matter of act, charity events, volunteering, and companies’ donations allow accelerating the progress in the achievement of the SDGs.

Many studiares (in particular, Kuzey et al. 2022; Loor-Zambrano et al. 2022; Bu et al. 2022) provided with arguments in favour of the idea that companies can “do well by doing good”. In other words, a company must experience a loss when it contributes to CSR, especially when stakeholders in the company appreciate the CSR practices.

However, in the background of non-profit activities lie commercial profits, while the widespread deprivation of companies of the principal opportunity to make a profit would lead to their bankruptcy (Chu and Fang 2021). Only the most successful and stable companies can accept large risks for profit. That is why the non-commercial approach to corporate social responsibility cannot be extended to entrepreneurship, on the whole, i.e., it has limited capabilities for scaling the practices of integrating the SDGs into corporate strategies (Jackson 2021).

The 3rd—commercial—approach to corporate social responsibility means that, during its implementation, companies are guided by their main goal, which is connected to making a profit, and the achievement of the SDGs is the priority. This ensures low risks of corporate social responsibility for companies’ profit. This approach fits the nature of entrepreneurship in the market economy in the best way and thus has potential for wide practical use since it ensures the largest systemic profit for all interested parties in the long term (Ang et al. 2022; Song and Tao 2022; Xie et al. 2022; Zhang et al. 2022).

2. Corporate Social Responsibility Based on Integrating the SDGs into Corporate Strategies

The theory of integration of the SDGs into corporate strategies, which describes and characterises in detail all three existing approaches to this integration. Their comparative analysis is given in Table 1.Table 1.

Comparative analysis of the existing approaches to the integration of the SDGs into corporate strategies.

| Criterion of Comparison | Approach to Integrating the SDGs into Corporate Strategies | ||

|---|---|---|---|

| Regulatory Approach | Non-Commercial Approach to CSR * | Commercial Approach to CSR * | |

| Mechanism of integrating the SDGs into corporate strategies | State regulation | Corporate social responsibility | |

| Support of the SDGs | Yes, forced | Yes, voluntary | |

| Market consequences of integrating the SDGs into corporate strategies | Slowdown of economic growth, development of the shadow economy | Slowdown of economic growth, interruption of the market mechanism | Support of the SDGs becomes a new form of “healthy” competition |

| Risks of support of the SDGs for profit | High | Low | |

| Existing literature in which the approach is presented | (Pizzi et al. 2021; Rahman 2021; Raithatha and Shaw 2021). | (Akopova et al. 2020; Mochales and Blanch 2022; Shayan et al. 2022; Sinkovics et al. 2021; Waheed and Zhang 2022; Wang et al. 2022). | (Medentseva 2017; Muhmad and Muhamad 2021; Petrovskaya et al. 2022; Roy et al. 2022; Vagin et al. 2022). |

Figure 1. Bi-directional vector scale of the integration of the SDGs into corporate strategies from the positions of risk for profit in various distinguished approaches. Source: authorscontributors.

Table 2.

Detailed characteristics of the integration of the SDGs into corporate strategies during the alternative approaches.

| Direction of CSR | Indicator of the UN (2021) | Symbol | Supported SDGs—UN Standards | CSR Measures to Support the SDGs |

|---|---|---|---|---|

| Responsible HRM * | Gender gap in time spent doing unpaid work (minutes/day) | SRSDG(1) | SDG5, SDG8 | Provision of gender-neutral jobs and fair wages |

| Unemployment rate (% of the total labour force) | SRSDG(2) | SDG8 | Keeping a stable number of jobs or increasing it to support employment | |

| Fundamental labour rights are effectively guaranteed (worst 0–1 best) | SRSDG(3) | SDG8 | Guarantee of labour rights (official employment) | |

| Fatal work-related accidents embodied in imports (per 100,000 population) | SRSDG(4) | SDG8 | Provision of occupational safety and health | |

| Responsible production (corporate environmental responsibility) | Production-based SO2 emissions (kg/capita) | SRSDG(5) | SDG13 | Improvement of treatment systems to reduce environmental pollution |

| Production-based nitrogen emissions (kg/capita) | SRSDG(6) | SDG13 | ||

| Carbon Pricing Score at EUR60/tCO2 (%, worst 0–100 best) | SRSDG(7) | SDG13 | Refusal to include environmental costs in the price | |

| Responsible finance | Corruption Perception Index (worst 0–100 best) | SRSDG(8) | SDG16 | Business’s fight against corruption |

| Corporate Tax Haven Score (best 0–100 worst) | SRSDG(9) | SDG16 | Full-scale payment of taxes (official business) |

- −

-

Stability or increase in jobs to support employment (Zhao et al. 2021). Using this measure, the CSR practices in support of the SDGs imply the refusal of personnel cuts even amid a crisis, the formation of a personnel reserve for continuous filling of jobs, and the creation of additional jobs, apart from the satisfaction of the company’s main needs for personnel in the striving for the growth of the intensity of business processes in the connection to human resources.

- −

-

Guarantee of labour rights (official employment) (Chanda and Goyal 2020; Ramos-González et al. 2021). Using this measure, the CSR practices in support of the SDGs imply providing employees with an expanded spectrum of social labour guarantees, which covers the basic obligations of employers, dictated by the labour law.

- −

-

Provision of production safety (Rawshdeh et al. 2019). Using this measure, the CSR practices in support of the SDGs imply accelerated automatisation of the types of labour activities that are potentially dangerous for life and health and employees, with the preservation of jobs (employees perform the function of remote control over automatised business processes).

- −

-

Improving treatment systems for reducing environmental pollution (Han and Cao 2021). Using this measure, the CSR practices in support of the SDGs imply a voluntary transition of companies to higher environmental standards of their activities and issued products (for example, automobile manufacturing) and implementation of ecological innovations.

- −

-

Refusal to include ecological costs in the price (Setyowati et al. 2021). Using this measure, the CSR practices in support of the SDGs imply a voluntary refusal of companies of a part of the profit in favour of an increase in environmental friendliness of their activities.

- −

-

Business’s fight against corruption (Dela Cruz et al. 2020). Using this measure, the CSR practices in support of the SDGs imply the companies’ refusal to participate in corruption schemes and disclosure of these schemes.

- −

-

Full-scale payment of taxes (official business) (Panos and Wilson 2020). Using this measure, the CSR practices in support of the SDGs imply companies’ refusal to participate in the schemes of tax evasion.

- (1)

-

Which SDGs (UN standards) are supported by companies in different regions of the world (research gap No. 1)?

- (2)

-

Which (of the list given in Table 2) measures of corporate social responsibility to support the SDGs are implemented in the practice of companies in different regions of the world (research gap No. 2)?

- (3)

-

Which approach is used? What are the risks of support of the SDGs (UN standards) with the help of corporate social responsibility for profit (research gap No. 3)?

References

- Batóg, Barbara, and Jacek Batóg. 2021. Regional government revenue forecasting: Risk factors of investment financing. Risks 9: 210.

- Hamed, Ruba Subhi, Basiem Khalil Al-Shattarat, Wasim Khalil Al-Shattarat, and Khaled Hussainey. 2022. The impact of introducing new regulations on the quality of CSR reporting: Evidence from the UK. Journal of International Accounting, Auditing and Taxation 46: 100444.

- Liu, Jingshan. 2021. Impact of uncertainty on foreign exchange market stability: Based on the LT-TVP-VAR model. China Finance Review International 11: 53–72.

- Fontana, Enrico. 2017. Strategic CSR: A panacea for profit and altruism: An empirical study among executives in the Bangladeshi RMG supply chain. European Business Review 29: 304–19.

- Jaisinghani, Dinesh, and Amritjot Kaur Sekhon. 2022. CSR disclosures and profit persistence: Evidence from India. International Journal of Emerging Markets 17: 705–14.

- Kaul, Aseem, and Jiao Luo. 2018. An economic case for CSR: The comparative efficiency of for-profit firms in meeting consumer demand for social goods. Strategic Management Journal 39: 1650–77.

- Schramm-Klein, Hanna, Dirk Morschett, and Bernhard Swoboda. 2015. Retailer corporate social responsibility: Shedding light on CSR’s impact on profit of intermediaries in marketing channels. International Journal of Retail and Distribution Management 43: 403–31.

- Akbar, Ahsan, Minhas Akbar, Marina Nazir, Petra Poulova, and Samrat Ray. 2021. Does working capital management influence operating and market risk of firms? Risks 9: 201.

- Gennaro, Alessandro. 2021. Insolvency risk and value maximization: A convergence between financial management and risk management. Risks 9: 105.

- Zhang, Shuang, Song Xi Chen, and Lei Lu. 2021. Inference for variance risk premium. China Finance Review International 11: 26–52.

- Bednarczyk, Teresa H., Ilona Skibińska-Fabrowska, and Anna Szymańska. 2021. An empirical study on the financial preparation for retirement of the independent workers for profit in Poland. Risks 9: 160.

- Kuzey, Cemil, Morgane M. C. Fritz, Ali Uyar, and Abdullah S. Karaman. 2022. Board gender diversity, CSR strategy, and eco-friendly initiatives in the transportation and logistics sector. International Journal of Production Economics 247: 108436.

- Loor-Zambrano, Halder Yandry, Luna Santos-Roldán, and Beatriz Palacios-Florencio. 2022. Relationship CSR and employee commitment: Mediating effects of internal motivation and trust. European Research on Management and Business Economics 28: 100185.

- Bu, Xuelin, Jacob Cherian, Heesup Han, Ubaldo Comite, Felipe Hernández-Perlines, and Antonio Ariza-Montes. 2022. Proposing Employee Level CSR as an Enabler for Economic Performance: The Role of Work Engagement and Quality of Work-Life. Sustainability 14: 1354.

- Chu, Jian, and Junxiong Fang. 2021. Economic policy uncertainty and firms’ labour investment decision. China Finance Review International 11: 73–91.

- Jackson, Susan T. 2021. Risking sustainability: Political risk culture as inhibiting ecology-centered sustainability. Risks 9: 186.

- Ang, Rui, Zhen Shao, Chen Liu, Changhui Yang, and Qingru Zheng. 2022. The relationship between CSR and financial performance and the moderating effect of ownership structure: Evidence from Chinese heavily polluting listed enterprises. Sustainable Production and Consumption 30: 117–29.

- Song, Baobao, and Weiting Tao. 2022. Unpack the relational and behavioral outcomes of internal CSR: Highlighting dialogic communication and managerial facilitation. Public Relations Review 48: 102153.

- Xie, Kefan, Shufan Zhu, and Ping Gui. 2022. A Game-Theoretic Approach for CSR Emergency Medical Supply Chain during COVID-19 Crisis. Sustainability 14: 1315.

- Zhang, Qian, Bee Lan Oo, and Benson Teck Heng Lim. 2022. Linking corporate social responsibility (CSR) practices and organizational performance in the construction industry: A resource collabouration network. Resources, Conservation and Recycling 179: 106113.

- Pizzi, Simone, Francesco Rosati, and Andrea Venturelli. 2021. The determinants of business contribution to the 2030 Agenda: Introducing the SDG Reporting Score. Business Strategy and the Environment 30: 404–21.

- Rahman, Md. Lutfur. 2021. Institutional ownership and violations of mandatory CSR regulation. Economics Letters 206: 109967.

- Raithatha, Mehul, and Tara Shankar Shaw. 2021. Firm’s tax aggressiveness under mandatory CSR regime: Evidence after mandatory CSR regulation of India. International Review of Finance 22: 286–94.

- Akopova, Elena S., Natalia V. Przhedetskaya, Yuri V. Przhedetsky, and Ksenia V. Borzenko, eds. 2020. Marketing of Nonprofit Organizations in Business-Oriented Economy: New Challenges and Priorities. Marketing of Healthcare Organizations: Technologies of Public-Private Partnership. Charlotte: Information Age Publishing.

- Mochales, Gerardo, and Javier Blanch. 2022. Unlocking the potential of CSR: An explanatory model to determine the strategic character of CSR activities. Journal of Business Research 140: 310–23.

- Shayan, Niloufar Fallah, Nasrin Mohabbati-Kalejahi, Sepideh Alavi, and Mohammad Ali Zahed. 2022. Sustainable Development Goals (SDGs) as a Framework for Corporate Social Responsibility (CSR). Sustainability 14: 1222.

- Sinkovics, Noemi, Rudolf R. Sinkovics, and Jason Archie-Acheampong. 2021. The business responsibility matrix: A diagnostic tool to aid the design of better interventions for achieving the SDGs. Multinational Business Review 29: 1–20.

- Waheed, Abdul, and Qingyu Zhang. 2022. Effect of CSR and Ethical Practices on Sustainable Competitive Performance: A Case of Emerging Markets from Stakeholder Theory Perspective. Journal of Business Ethics 175: 837–55.

- Wang, Yizhi, Brian Lucey, Samuel Alexandre Vigne, and Larisa Yarovaya. 2022. An index of cryptocurrency environmental attention (ICEA). China Finance Review International. ahead-of-print.

- Medentseva, Evgenia V. 2017. The Legal Forms of Economic Relations and Their Transformation in the Modern Economic Conditions: Part Two: Legal Foundations of Corporate Control over the Financial and Economic Activities of Commercial Organizations in the Modern Economic Conditions. Economic and Legal Foundations of Modern Russian Society. Charlotte: Information Age Publishing.

- Muhmad, Siti Nurain, and Rusnah Muhamad. 2021. Sustainable business practices and financial performance during pre- and post-SDG adoption periods: A systematic review. Journal of Sustainable Finance and Investment 11: 291–309.

- Petrovskaya, Maria V., Vladimir Z. Chaplyuk, Raju Mohammad Kamrul Alam, Md. Nazmul Hossain, and Ahmad S. Al Humssi. 2022. COVID 19 and Global Economic Outlook. Current Problems of the World Economy and International Trade. Bingley: Emerald Publishing Limited, vol. 42.

- Roy, Partha P., Sandeep Rao, and Min Zhu. 2022. Mandatory CSR expenditure and stock market liquidity. Journal of Corporate Finance 72: 102158.

- Vagin, Sergei G., Elena I. Kostyukova, Natalia E. Spiridonova, and Tatiana M. Vorozheykina. 2022. Financial Risk Management Based on Corporate Social Responsibility in the Interests of Sustainable Development. Risks 10: 35.

- Kornieieva, Yuliia. 2020. Non-financial reporting challenges in monitoring SDG’s achievement: Investment aspects for transition economy. International Journal of Economics and Business Administration 8: 62–71.

- Lassala, Carlos, Maria Orero-Blat, and Samuel Ribeiro-Navarrete. 2021. The financial performance of listed companies in pursuit of the Sustainable Development Goals (SDG). Economic Research-Ekonomska Istrazivanja 34: 427–49.

- Martí-Ballester, Carmen-Pilar. 2020. Financial performance of SDG mutual funds focused on biotechnology and healthcare sectors. Sustainability 12: 2032.

- Battisti, Enrico, Niccolò Nirino, Erasmia Leonidou, and Alkis Thrassou. 2022. Corporate venture capital and CSR performance: An extended resource based view’s perspective. Journal of Business Research 139: 1058–66.

- Kong, Gaowen. 2022. Causal effects of corporate taxes on private firms’ earnings management: A regression discontinuity analysis. China Finance Review International. ahead-of-print.

- Quang, Phung Thanh, Ehsan Rasoulinezhad, Nguyen Nhat Linh, and Doan Phuong Thao. 2022. Investigating the determining factors of sustainable FDI in Vietnam. China Finance Review International.

- Wentzel, Lance, Julius Ayodeji Fapohunda, and Rainer Haldenwang. 2022. The Relationship between the Integration of CSR and Sustainable Business Performance: Perceptions of SMEs in the South African Construction Industry. Sustainability 14: 1049.

- UN. 2021. The Sustainable Development Report 2021 and Supplementary Materials: Database. Available online: https://dashboards.sdgindex.org/downloads (accessed on 19 April 2022).

- He, Junqian, and Hyosun Kim. 2021. The effect of socially responsible HRM on organizational citizenship behavior for the environment: A proactive motivation model. Sustainability 13: 7958.

- Hirsu, Lavinia, Zenaida Quezada-Reyes, and Lamiah Hashemi. 2021. Moving SDG5 forward: Women’s public engagement activities in higher education. Higher Education 81: 51–67.

- Zhao, Hongdan, Qiongyao Zhou, Peixu He, and Cuiling Jiang. 2021. How and When Does Socially Responsible HRM Affect Employees’ Organizational Citizenship Behaviors Toward the Environment? Journal of Business Ethics 169: 371–85.

- Chanda, Udayan, and Praveen Goyal. 2020. A Bayesian network model on the interlinkage between Socially Responsible HRM, employee satisfaction, employee commitment and organizational performance. Journal of Management Analytics 7: 105–38.

- Ramos-González, María del Mar, Mercedes Rubio-Andrés, and Miguel Ángel Sastre-Castillo. 2021. Effects of Socially Responsible Human Resource Management (SR-HRM) on Innovation and Reputation in Entrepreneurial SMEs. Available online: https://link.springer.com/article/10.1007/s11365-020-00720-8 (accessed on 22 May 2022).

- Rawshdeh, Zainab Ali, Zafir Khan Mohamed Makhbul, Najeeb Ullah Shah, and Perengki Susanto. 2019. Impact of perceived socially responsible-hrm practices on employee deviance behavior. International Journal of Business and Management Science 9: 447–66.

- Han, Xiuyan, and Tianyi Cao. 2021. Study on corporate environmental responsibility measurement method of energy consumption and pollution discharge and its application in industrial parks. Journal of Cleaner Production 326: 129359.

- Setyowati, Arum, Nasyiah Hasanah Purnomowati, Dinar Sari, and Endan Ramadhan. 2021. Does corporate environmental responsibility affect investor future goal in the energy sector firms? IOP Conference Series: Earth and Environmental Science 905: 012140.

- Dela Cruz, Aeson Luiz, Chris Patel, Sammy Ying, and Peipei Pan. 2020. The relevance of professional skepticism to finance professionals’ Socially Responsible Investing decisions. Journal of Behavioral and Experimental Finance 26: 100299.

- Panos, Georgios A., and John O. S. Wilson. 2020. Financial literacy and responsible finance in the FinTech era: Capabilities and challenges. European Journal of Finance 26: 297–301.

More