Your browser does not fully support modern features. Please upgrade for a smoother experience.

Please note this is a comparison between Version 2 by Bruce Ren and Version 1 by Yongshun Xie.

Since the new century, countries in Africa have started a new round of rail network planning and construction which brings the completed different features together with the spatial organization of the railway network during the colonial period. Along with the strategic layout of “going out” with China’s railways, the organizational structure of the African railway network will make a tremendous change for the construction market, network organization, and gauge structure of the African railways.

- railway network

- evolution

- construction pattern

- market differentiation

- Africa

1. Introduction

As an important infrastructure, railway has an important impact on the change of regional space-time relationships and the integration of social and economic resources. From the global perspective and historical dimension, behind its transportation attribute, the railway contains a variety of deep connotations such as national defense, military, geographical competition and even political rule, which are not limited to the technical and physical attributes of transportation facilities [1]. In the African continent, railways are endowed with more complex attributes and characteristics. Historically, the railway construction, route layout and technical standards in Africa have a profound colonial color, and different spatial organization modes have been formed in geographical space. In 1851, Britain built the first railway in Egypt, which became the starting point of transportation facilities construction in Africa. By the beginning of the 20th century, many African countries had built railways and formed networks in some areas. At present, the railways built in Africa during the colonial period have problems such as unbalanced distribution, disordered technical standards and low level of operation and maintenance, which restrict the social and economic development. In recent years, in order to improve the backward railway construction and the shortage of transportation services, African countries have successively formulated railway network planning, including a series of major railway projects such as the African transnational railway, the North-South corridor railway, the West Africa railway and the Central Africa railway. These blueprints and new railways will gradually change the long-standing railway network pattern, layout modes and technical systems in Africa, and will change the interconnection and integration level of various countries.

However, few scholars pay attention to the geographical research of African railway networks, and the research on the past and future changes of African railway network patterns, organization models and technical systems is even less. Based on historical geography, Jean [2] made a geographical explanation of the construction of railway network in West Africa from the relationship between regional scales, power and networks. Wang [3] and Wang [4], respectively, took Mombasa-Nairobi Railway and Addis Ababa-Djibouti Railway as cases to discuss the institutional, cultural and technical differences in railway construction in Africa. The former believes that the localized management of technical standards, management mode and industrial chain will contribute to the success of China’s railway overseas construction projects and operations. The latter puts forward the evolutionary framework of railway-institution-economy-culture system, which believes that the leapfrog technology transfer will be inappropriate.

For a long time, scholars have focused on the spatial and temporal convergence effect on railway networks [5] and investigated the relationship mechanisms between railway and regional development [6]. These studies mainly describe the evolution of railway accessibility at different scales [7[7][8],8], analyze its impact mechanisms such as spatio-temporal convergence, factor flow and transportation efficiency [9[9][10],10], and evaluate the spatial effects such as travel cost reduction [11[11][12][13],12,13], economic connection strengthening [14[14][15],15], urban system reconstruction [16,17][16][17] and industrial structure adjustment [18]. Nevertheless, the railway network pattern and spatial organization model have not been paid enough attention, and only a few scholars have involved this topic in the correlation research. Jin [19] analyzed the evolution of the high-speed railway in East Asia and considered that its distribution pattern evolved from “North-South linearity” to “Networking”. Wang [20] discussed the development process and mode of China’s high-speed railway network, and believed that its expansion evolved from “core-core” mode to “core-network” mode, but the discussion was simple.

There is relatively little research on African Railways. The existing research focuses on the field of construction engineering, and the research on its geographical problems is only slightly involved in some books. Under the background of rapid railway construction in Africa, enterprises from China, France, Turkey and other countries have entered the African railway construction market, and Chinese enterprises have an especially high market share [21]. These countries have different railway technical standards and experience bases, and implement different technology transmission paths and market expansion modes in Africa, which has a great impact on the spatial pattern and technical connectivity of African railway networks. Therefore, it is urgent to study the evolution of its spatial pattern and construction market pattern. However, few scholars have studied the market pattern of railway construction in Africa. Only international organizations such as the International Monetary Fund, the United Nations Industrial Development Organization, the African Union and the African Development Bank have made statistics on the results of railway construction in Africa. On the one hand, the research on construction cooperation between China and Africa on the railway is attached to the comprehensive discussion on China’s and Africa’s infrastructure construction. For example, Wang [22] explored the impact of road network improvement brought by the entry of Chinese enterprises when combing African infrastructure construction, and Zheng [23] discussed China’s railway construction market potential when analyzing African infrastructure financing. On the other hand, a few scholars introduced some railway construction cases in Africa and investigated the current situation, problems and countermeasures, such as the Tanzania–Zambia Railway [24,25][24][25], the Addis Ababa–Djibouti Railway [26], the Mombasa–Nairobi Railway [27], and the Angola Railway [28].

2. Differentiation of Railway Construction in Africa

The basic feature of railway construction in Africa is “undertaken by other countries”, and therefore different technical standards have been disseminated. “Technology implantation” has become an obvious feature of railway construction in African countries. Through the above analysis, the researchers can know that there are still great prospects for railway construction in Africa. However, which countries and enterprises undertake the construction of railways in Africa? What are the roles of these countries and enterprises? These problems need further analysis and investigation.

2.1. Contractor Country

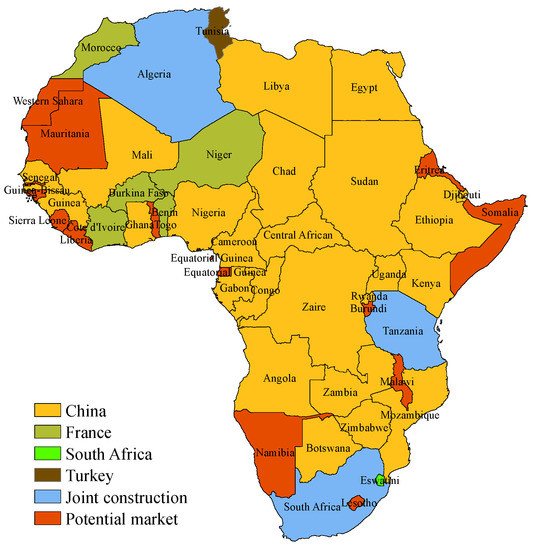

In the future, the construction of African Railways will be mainly undertaken by other countries (Figure 1). Railway construction in African countries is mainly undertaken by China, France, Turkey, Portugal, South Africa and other countries. Most of them are countries outside the continent, and only South Africa is an African country. Countries outside the continent can be divided into “African cooperative countries in the new era” and “former colonial suzerain countries”. Among them, China and Turkey are African cooperative countries, and Portugal and France are former colonial suzerain countries.

Figure 1. The differentiation of African railways contractor countries.

China has undertaken railway construction in 27 African countries, which is the largest among all contractor countries. Among these, 22 countries were completely undertaken by China alone, and five countries were jointly undertaken by China and other countries. China’s contracted market covers 80.1% of the area of the African continent, showing an all-round expansion in space, involving northern, western, eastern, central and southern regions of Africa. Turkey has undertaken railway construction in three African countries. Among them, Tunisia is the only country that has been completely undertaken by Turkey, and Algeria and Ethiopia are jointly undertaken by Turkey and other countries. France has undertaken railway construction in five African countries, including Côte d’Ivoire, Burkina Faso, Benin, Nigeria and Morocco, which are mainly former French colonies. The natural connection between suzerain and colony is still working. In terms of space, the countries with railway construction undertaken by France are mainly concentrated in western Africa. In addition, South Africa’s railway construction is mainly undertaken by its own country; Portugal participated in the joint construction of Tanzania’s railway.

The basic strategies adopted by African countries in railway construction can be divided into two types: one is the mode of independent construction, and the other is the mode of joint construction. As shown in Figure 1, most countries have formed a model of independent construction, covering 24 countries, accounting for 50% of the sample countries. A few countries have adopted the model of joint construction by two or more countries. There are 10 countries, including Algeria, Chad, Cameroon, Tanzania and South Africa, accounting for 20.8% of the sample countries. Due to its own economic, political, planning and other factors, there are still 14 countries whose railway construction has not been clearly undertaken. These countries are potential markets for railway construction in Africa in the future.

2.2. Contractor Enterprise

The above analysis is carried out from the perspective of countries. However, enterprises are the accounting subject of interests and the executive subject of railway construction. They play a main role in the African railway construction market. Therefore, they need to be further analyzed from the perspective of enterprises. The researchers analyzed the distribution and association of contractor enterprise of planned railways in Africa, as shown in Figure 2 and Figure 3. The main features are as follows.

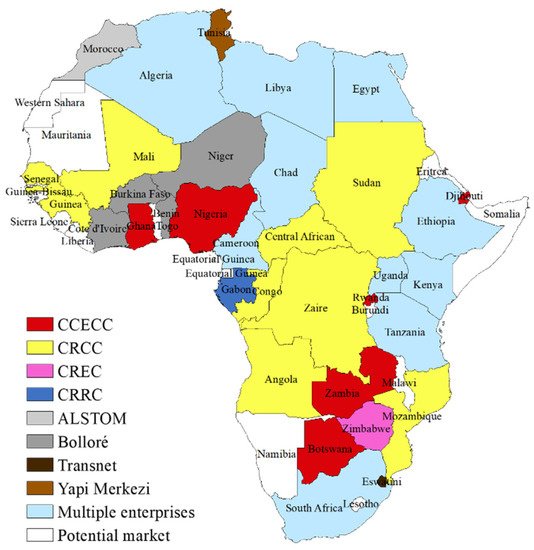

Figure 2. The spatial distribution of contractor enterprises.

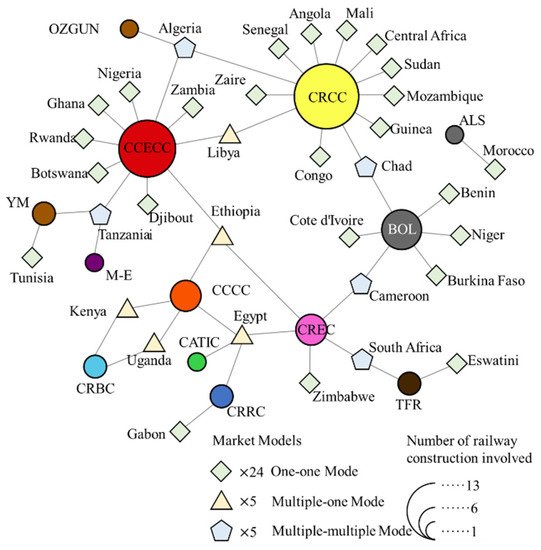

Figure 3. The composition and contact of contractor enterprises.

There are 13 enterprises in the African railway construction market, of which seven are Chinese enterprises and the remaining six are French, Portuguese, Turkish and South African enterprises, respectively. It is obvious that Africa has formed a railway construction market dominated by Chinese enterprises. Among them, China Civil Engineering Construction Corporation (CCECC) group and China Railway Construction Corporation (CRCC) are the two largest construction enterprises, involving railway construction in 10 and 13 countries, respectively. China Railway Group Limited (CREC) and China Communications Construction Company (CCCC) involve four countries, respectively, CRRC Corporation (CRRC) and China Road and Bridge Corporation (CRBC) involve two countries, respectively, and AVIC International Holding Corporation (AVIC) participates one country’s railway construction as a cooperative enterprise. The Bolloré Group (BOL) is the third largest enterprise in the African railway construction market, involving railway construction in six countries. In addition, Yapi Merkezi (YM) of Turkey and Transnet (TFR) of South Africa participated in the railway construction of two countries, respectively, Alstom Group (ALS) of France, Ozgun Makine (OM) of Turkey and Mota-Engil Group (M-E) of Portugal participated in the railway construction of one country, respectively.

It can be seen that the construction market of some enterprises presents obvious regional characteristics. The practice of “starting in one country–expanding to neighboring countries” has become the development model of most enterprises. The construction market of CCECC is concentrated in West and Central Africa, CRCC is concentrated in East and Northeast Africa, and BOL is concentrated in West Africa.

Enterprises adopt different organizational models in the railway construction market. While OM, AVIC and CCCC mainly adopt the mode of “Cooperative Construction”, ALS adopts the mode of “Independent Construction”. Other enterprises adopt both models, but show different preferences. CREC mainly adopts the “Cooperative Construction” mode, supplemented by the “Independent Construction” mode. CRRC, YM and TFR pay equal attention to the two modes. CCECC, CRCC and BOL mainly adopts the “Independent Construction” mode, supplemented by the “Cooperative Construction” mode.

The interaction between the contractor country, the contractor enterprise and the local country promote the formation of different market models for railway construction in Africa. The composition of contractor enterprises of different railway lines in the local country has made the market modes more complex. The construction modes can be divided into three types.

- (1)

-

One-one ModeRailway Construction in most African countries are undertaken by one enterprise in one country (One-one Mode). This mode is easy to unify the railway technical standards within the country, and the market entry of the contractor enterprise is exclusive. There are 24 countries have adopted this mode, accounting for 50% of the total.

- (2)

-

Multiple-one ModeRailway construction of a few countries are undertaken by multiple enterprises in one country (Multiple-one Mode). This mode reflects that the market entry of the contractor country is exclusive. There are 5 countries have adopted this mode, including Ethiopia, Libya, Uganda, Kenya and Egypt. According to the specific situation, the mode can be further divided into cooperation mode and competition mode: The suburban railway in Egypt is constructed by a consortium composed of CRCC and AVIC; Kenya’s East Africa railway is jointly constructed by CCCC and CRBC; these belong to the cooperation mode. Libya’s coastal line and west line are constructed by CRCC and CCECC, respectively; Ethiopia’s Addis Ababa–Djibouti railway and Weldia–Mekele railway are constructed by CCCC and CCECC, respectively; these belong to the competition mode.

- (3)

-

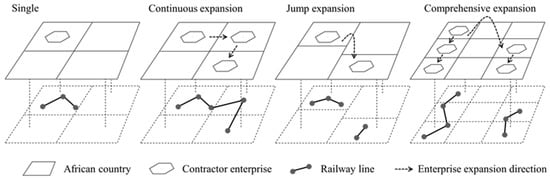

Multiple-multiple ModeRailway construction of a few countries are undertaken by multiple enterprises in multiple countries (Multiple-multiple Mode). There are five countries that have adopted this mode, including Algeria, Chad, Tanzania, Cameroon and South Africa. This mode can also be subdivided into competition mode and cooperation mode: Algeria’s 55km railway is constructed by a consortium composed of CCECC and OM; the Dazhi–Morogoro Central railway in Tanzania is jointly constructed by YM and M-E; these belong to the cooperation mode. CREC and BOL, respectively, undertake railway construction in Cameroon; CRCC and BOL, respectively, undertake railway construction in Chad; these belong to the competition mode.In terms of the distribution of enterprises, the contractor enterprises form four market expansion modes: single, continuous expansion, jump expansion and comprehensive expansion (Figure 4). Different modes have different spatial expansion laws. The single mode means that the enterprise focuses on one country’s railway construction. ALS, OM, M-E, CRRC, CRBC and AVIC are such distribution mode. The continuous expansion mode mainly refers to the enterprise constructing railways in multiple countries, which are continuously distributed in space. BOL and CCCC are such distribution mode. The jump expansion mode is mainly that the market countries of the contractor enterprises are discontinuous and are not limited by geographical proximity factors. CREC, TFR and YM are such distribution mode. The comprehensive expansion mode refers to that the market countries of the contractor enterprises have both continuous distribution and jump distribution. CCECC and CRCC are such distribution mode.

Figure 4. The spatial distribution pattern of contractor enterprises.

Figure 4. The spatial distribution pattern of contractor enterprises.

References

- Jin, F.; Wang, C.; Li, X.; Wang, J. China’s regional transport dominance: Density, proximity, and accessibility. J. Geogr. Sci. 2010, 20, 295–309.

- Debrie, J. From colonization to national territories in continental West Africa: The historical geography of a transport infrastructure network. J. Transp. Geogr. 2010, 18, 292–300.

- Wang, J.; Du, F.; Wu, M.; Liu, W. Embedded technology transfer from an institution and culture nexus perspective: Experiences from the Mombasa-Nairobi Standard-Gauge Railway. J. Geogr. Sci. 2021, 31, 681–698.

- Wang, C.; Xie, Y.; Chen, P. Institutional-economic-cultural adaptability of overseas railway construction: A case study of Addis Ababa-Djibouti Railway. Acta Geogr. Sin. 2020, 75, 1170–1184.

- Lin, G.C.S. Transportation and metropolitan development in China’s Pearl River Delta: The experience of Panyu. Habitat Int. 1999, 23, 249–270.

- Linneker, B.; Spence, N. Road transport infrastructure and regional economic development: The regional development effects of the M25 London orbital motorway. J. Transp. Geogr. 1996, 4, 77–92.

- Zhong, Y.; Wang, X.; Fu, Y. Regional development imbalance of the “Min-Xin Axis Belt”. Econ. Geogr. 2018, 38, 22–29.

- Feng, C.; Feng, X.; Liu, S.J. Effects of high speed railway network on the inter-provincial accessibilities in China. Prog. Geogr. 2013, 32, 1187–1194.

- Liu, B.; Wu, W.; Su, Q. Spatio-temporal evolution characteristics and mechanism of railway efficiency in China. Geogr. Res. 2018, 37, 512–526.

- Chen, C.L. Reshaping Chinese space-economy through high-speed trains: Opportunities and challenges. J. Transp. Geogr. 2012, 22, 312–316.

- Preston, J. High speed rail in Britain: About time or a waste of time? J. Transp. Geogr. 2012, 22, 308–311.

- Shaw, S.L.; Fang, Z.; Lu, S.; Tao, R. Impacts of high speed rail on railroad network accessibility in China. J. Transp. Geogr. 2014, 40, 112–122.

- Jiang, H.B.; Zhang, W.Z.; Qi, Y.; Jiang, J. The land accessibility influenced by China’s high-speed rail network and travel cost. Geogr. Res. 2015, 34, 1015–1028.

- Liwen, L.; Ming, Z. The impacts of high speed rail on regional and spatial economy abroad and the enlightenment to China. Urban Plan. Int. 2018, 33, 95–100.

- Haibing, J.; Yi, Q.; Chuanwu, L. China’s city high-speed rail (HSR) passenger spatial linkage pattern and its influence factors. Econ. Geogr. 2018, 38, 26–33.

- Jiao, J.; Wang, J.; Jin, F.; Wang, H. Impact of high-speed rail on inter-city network based on the passenger train network in China, 2003–2013. Acta Geogr. Sin. 2016, 71, 265–280.

- Liu, C.; Xu, J.; Guo, Q. Spatial pattern of urban centrality on railway hub in China’s mainland. Econ. Geogr. 2019, 39, 57–66.

- Jiang, H.; Cai, H.; Meng, X. The structural impact of high speed rail upon urban industries in China. Hum. Geogr. 2017, 32, 132–138.

- Jin, F.; Jiao, J.; Qi, Y.; Yang, Y. Evolution and geographic effects of high-speed rail in East Asia: An accessibility approach. J. Geogr. Sci. 2017, 27, 515–532.

- Wang, J.; Jiao, J. Development process, spatial pattern and effects of high-speed rail network in China. Trop. Geogr. 2014, 34, 275–282.

- Ministry of Foreign Affairs of the People’s Republic of China. China-Africa Poverty Reduction and Development Cooperation. 2017. Available online: www.fmprc.gov.cn/mfa_eng/ (accessed on 1 October 2021).

- Wang, W. Analysis of China-Africa infrastructure construction cooperation. Int. Proj. Contracting Labour Serv. 2016, 11, 51–52.

- Zheng, Y. Prospect of infrastructure construction in Africa and analysis of Chinese factors. J. Int. Econ. Coop. 2014, 6, 71–74.

- Shen, X. China’s Aid to Tan-Zan Railway: Its Consideration, Building Progress and Impacts; East China Normal University: Shanghai, China, 2009.

- Hu, Z. The past, present and future of Tan-Zan railway. Railw. Econ. Res. 2000, 2, 46–47.

- Zhang, L. Innovation of internationalized business model of enterprises from the experience of Ya-Ji Railway. Int. Proj. Contracting Labour Serv. 2019, 3, 47–50.

- Wei, X. Study of Risk Management of Africa Area Railway EPC Project: Take Kenny Mombasa-Nairobi Railway EPC Project for Example; Beijing University of Posts and Telecommunications: Beijing, China, 2013.

- Liu, D. The Research of “Angola Model”; Shanghai Normal University: Shanghai, China, 2016.

More