Your browser does not fully support modern features. Please upgrade for a smoother experience.

Please note this is a comparison between Version 2 by Rita Xu and Version 1 by Valentina LAGASIO.

Environmental, Social and Governance (ESG) is currently one of the main focus areas for policy makers worldwide.

- European Union

- corporate governance

- sustainable finance

- Environmental

- ESG

- Environmental Social Governance

1. Introduction

In December 2016, the European Commission formed a high-level expert group (HLEG) to develop an overarching and detailed EU sustainable finance strategy. On 31 January 2018, the HLEG released its final report [1]. This report presented an holistic view of European sustainable finance and established two financial system imperatives. The first is to increase finance’s commitment to long-term, inclusive development. The second goal is to improve financial stability by fostering the awareness about environmental, social and governance (ESG) issues while making investment decisions. The United Nations-backed Principles for Responsible Investment Directive 2016/234 incorporates ESG considerations into the EU legislative framework. The increased attention by policy makers toward this topic has also been followed by an improved appetite of financial investors for ESG funds. According to the ECB’s Financial Stability Review, the Asset Under Management (AUM) of these funds has increased by 170%, soaring from 500 billion USD in 2015 to more than 1.3 trillion USD in 2020 [2].

As suggested by the United Nations Environment Programme (UNEP) Inquiry and the Principles for Responsible Investment (PRI), we can refer to ESG as the following: (i) Environmental (E) issues are related to the natural environment and natural systems; (ii) Social (S) issues refer to the rights of people and communities; and (iii) Governance (G) issues pertain to corporate governance of firms.

2. Current European Regulatory Framework for Banking Institutions with Reference to the ESG Principles

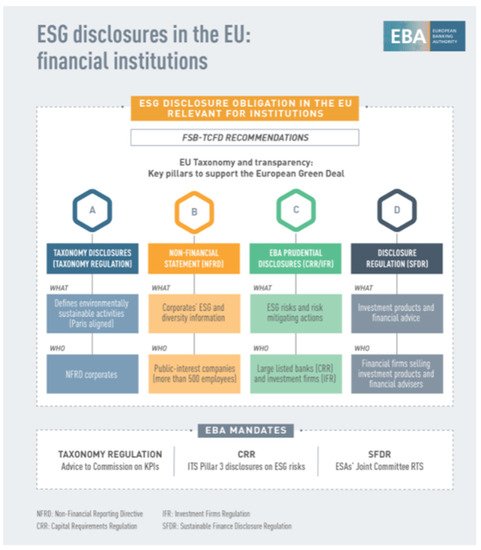

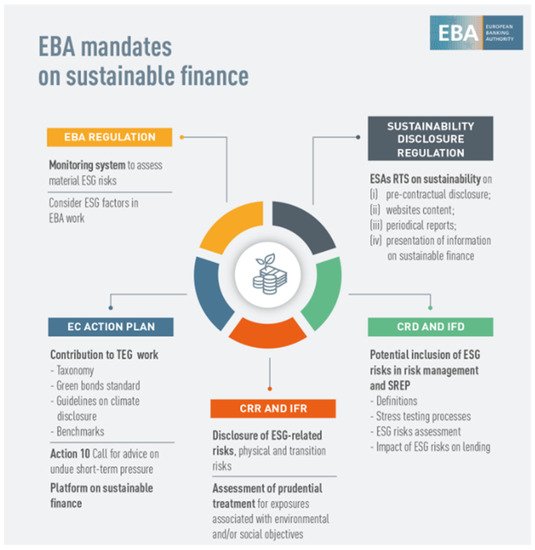

Specific disclosure requirements have been introduced in the current European regulatory framework for industrial companies and for banks alike in order to support the implementation of the so-called European Green Deal [20][3]. Figure 1 summarises the disclosure requirements for banks under the current European regulatory framework. As shown in Figure 1, the Taxonomy Regulation, that came into force in 2020, introduces some criteria for the classification of the activities performed by industrial companies based on their environmental sustainability (in line with the provisions of the Paris Climate Agreement). The definition of specific criteria for the classification of the activities performed by industrial companies provides more clarity regarding the environmental sustainability of the firms’ businesses. The Non-Financial Reporting Directive (NFRD) imposes additional disclosure requirements on listed industrial companies with more than 500 employees. The aim of this directive is to improve the quality of data available to banks and investors to direct financial resources toward sustainable investments. Furthermore, following the introduction of the so-called CRR2 (i.e., Capital Requirements Regulation) the European significant banks are expected to disclose in the information provided to investors the risks related to ESG factors to which they are exposed, and the related mitigating actions being undertaken to reduce their severity. Finally, in 2021, the Financial Services Sustainability Disclosure Regulation (SFDR) also came into force. This regulation introduces a new set of rules that is aimed at making the sustainability profile of funds and financial products more comparable and easier for investors to understand. The new rules will lead to the classification of financial products in specific types by including metrics to assess their environmental, social and governance (ESG) impacts. It has also been noticed that the EBA has been given three specific mandates to further enforce the introduction of the ESG principles in the European banking regulation. Under the taxonomy regulation, the EBA has been requested to propose to the European Commission a number of key performance indicators (KPIs), together with the related methodology for the disclosure by credit institutions and by investment firms, on how and to what extent their activities qualify as environmentally sustainable. In its opinion released in March 2021 [22][5], the EBA underlined the importance of the green asset ratio (GAR) as a key means to understand how institutions are financing sustainable activities and meeting the Paris agreement targets. In March 2021, the EBA also published a consultation paper on draft implementing technical standard (ITS) [23][6] on Pillar 3 disclosures on environmental, social and governance risks as a response to the second mandate highlighted in Figure 1. In line with the requirements laid down in the Capital Requirements Regulation (CRR), the draft ITS proposes comparable quantitative disclosures on climate-change related transition and physical risks, including information on exposures towards carbon related assets and assets subject to chronic and acute climate change events. They also include quantitative disclosures on institutions’ mitigating actions supporting their counterparties in the transition to a carbon neutral economy and in the adaptation to climate change. In addition, they request significant banks to disclose their GAR. The green asset GAR identifies the institutions’ assets financing activities that are environmentally sustainable according to the EU taxonomy, such as those consistent with the European Green Deal and the Paris agreement goals. Finally, the draft ITS provides qualitative information on how institutions are embedding ESG considerations in their governance, business model and strategy and risk management framework. The new banking regulation package, CRR2 and CRDV (i.e., Capital Requirements Directive), has also provided a number of mandates to the European Banking Authority (EBA) to issue specific regulations and guidelines for banks and supervisory authorities with regards to the sustainable finance. Figure 2 summarises the main mandates that have been provided to the EBA through the new banking regulatory package.

References

- European Commission. Financing a Sustainable Economy. Final Report by the High-Level Expert Group on Sustainable Finance; European Commission: Brussels, Belgium, 2018; pp. 6–8.

- European Central Bank. Financial Stability Review; European Central Bank: Frankfurt am Main, Germany, 2020; p. 94.

- A European Green Deal. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal_en (accessed on 14 October 2021).

- EBA. EBA Acknowledges Adoption by the European Commission of Standards on Institutions’ Public Disclosures. Available online: https://www.eba.europa.eu/eba-acknowledges-adoption-european-commission-standards-institutions%E2%80%99-public-disclosures (accessed on 14 October 2021).

- EBA. Call for Advice to the European Supervisory Authorities on Key Performance Indicators and Methodology on the Disclosure of How and to What Extent the Activities of Undertakings under the NFRD Qualify as Environmentally Sustainable as Per the EU Taxonomy. Available online: https://www.eba.europa.eu/sites/default/documents/files/document_library/About%20Us/Missions%20and%20tasks/Call%20for%20Advice/2021/CfA%20on%20KPIs%20and%20methodology%20for%20disclosures%20under%20Article%208%20of%20the%20Taxonomy%20Regulation/963620/Letter%20to%20EC%20-%20CfA%20Article%208%20Taxonomy%20Regulation.pdf (accessed on 14 October 2021).

- Consultation Paper on Draft ITS on Pillar 3 Disclosures on ESG Risks. Available online: https://www.eba.europa.eu/sites/default/documents/files/document_library/Publications/Consultations/2021/Consultation%20on%20draft%20ITS%20on%20Pillar%20disclosures%20on%20ESG%20risk/963621/Consultation%20paper%20on%20draft%20ITS%20on%20Pillar%203%20disclosures%20on%20ESG%20risks.pdf (accessed on 14 October 2021).

- Sustainable Finance. Available online: https://www.eba.europa.eu/financial-innovation-and-fintech/sustainable-finance (accessed on 14 October 2021).

- JC 2021 03-Joint ESAs Final Report on RTS under SFDR. Available online: https://www.eba.europa.eu/sites/default/documents/files/document_library/Publications/Draft%20Technical%20Standards/2021/962778/JC%202021%2003%20-%20Joint%20ESAs%20Final%20Report%20on%20RTS%20under%20SFDR.pdf (accessed on 14 October 2021).

- 2020-10-15 BoS-ESG report MASTER FILEcl. Available online: https://www.eba.europa.eu/sites/default/documents/files/document_library/Publications/Discussions/2021/Discussion%20Paper%20on%20management%20and%20supervision%20of%20ESG%20risks%20for%20credit%20institutions%20and%20investment%20firms/935496/2020-11-02%20%20ESG%20Discussion%20Paper.pdf (accessed on 14 October 2021).

- Guidelines on Loan Origination and Monitoring. Available online: https://www.eba.europa.eu/regulation-and-policy/credit-risk/guidelines-on-loan-origination-and-monitoring (accessed on 14 October 2021).

- ECB. ECB Publishes Final Guide on Climate-Related and Environmental Risks for Banks. Available online: https://www.bankingsupervision.europa.eu/press/pr/date/2020/html/ssm.pr201127~5642b6e68d.en.html (accessed on 14 October 2021).

More