Your browser does not fully support modern features. Please upgrade for a smoother experience.

Please note this is a comparison between Version 1 by Apichaya Lilavanichakul and Version 2 by Catherine Yang.

Population growth and urbanization in Thailand has generated negative environmental externalities and the underuse of agricultural materials. Plastics from cassava present an alternative that helps reduce the use of non-biodegradable petroleum-based plastics and can reshape a sustainable cassava value chain. The development of cassava-based bioplastic not only positively contributes to economic aspects but also generates beneficial long-term impacts on social and environmental aspects. Considering cassava supply, bioplastic production, and potential consumer acceptance, the development of bioplastics from cassava in Thailand faces several barriers and is growing slowly, but is needed to drive the sustainable cassava value chain.

- cassava

- bioplastic

- BCG economy

- sustainable value chain

1. Introduction

Cassava is one of the carbohydrate crops that accounts for 10% of total carbohydrate crop consumption in the world after maize, wheat, rice, and potato [1]. Cassava has been used for 4F sectors, including food for humans, feed for animals, fuel for renewable energy, and factories using cassava materials [2]. In Thailand, cassava is not only used for food consumption but is also mainly produced as low-value-based products such as dried cassava for animal feeds and cassava starch for industries [3]. Thailand is the world’s largest exporter of cassava, with a market share of 55.53% of the total global cassava export in 2020 [4]. Thailand exports about 73% of the total cassava production, divided into cassava starch (44.1%), cassava chips (28.2%), and cassava pellets (0.3%) [2]. In 2021, Thailand produced 34.1 million tons of fresh cassava roots, with a total production area of 1.59 million hectares [5].

Market volatility, demand shifts, input supply challenges, and changes in climate events can generate shock and instability in the cassava value chain. Price fluctuations and the global market uncertainties of cassava production have led to lower profitability for farmers and a disruption to the flow of suppliers and buyers in the value chain [4]. The price of cassava widely fluctuates over a year depending on various factors, including the price of substitute products, government intervention, technology availability, and agricultural policy from importing countries, especially China [6][7][6,7]. The reduction in the price gap between cassava and other carbohydrate crops and the limitation of value-adding alternatives lead to a lack of competitive advantage in the cassava sector in Thailand.

Facing sustainability and environmental challenges, the bio-based, circular, and green (BCG) economy plan was drawn up to drive policies in the agricultural and industrial sectors. Following the implications of the sustainable development goals (SDGs), Thailand aims to move toward sustainable development coupled with the 20-year national strategy (2018–2037) by exploring value-added agriculture to create new value with the circular economy in agricultural materials and waste, as well as encouraging future industries and services with technology and innovations [8]. The development of the cassava value chain through bioplastic production addresses SDG target 10, where integrating related stakeholders in the value chain gives them an opportunity to participate in income growth, and SDG target 12, where the use of technology moves towards more sustainable patterns of consumption and production (e.g., agricultural waste is perceived as a valuable resource rather than a disposal problem). The circular economy approach seeks to minimize waste and maximize resource efficiency by promoting the reuse, recycling, and repurposing of materials [9][10][9,10]. The by-products of cassava starch production (e.g., cassava pulp and cassava peel) are usually used for animal feeds, compost, and produced biogas.

2. Cassava Sector in Thailand

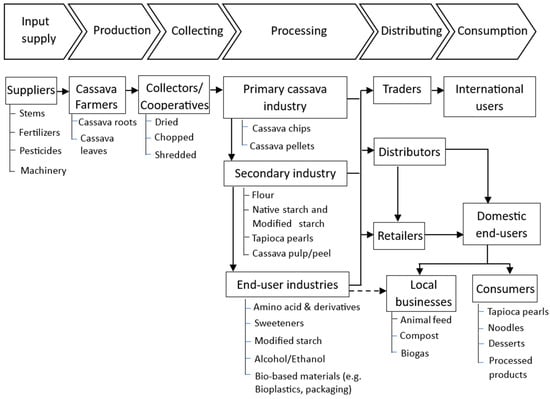

Thailand is the third largest cassava grower in the world, with a total production of more than 30 million tons per year, after Nigeria and Congo. Cassava production is mostly located in Northeastern Thailand. More than 90% of its production takes place on small family farms, averaging 2.56–3.2 ha per household. From 2021 to 2022, the number of cassava farmer families was 738,153 households, with a production cost of 52.24 USD/ton [4]. The exchange rate used when converting the figures is 1 USD to 35.93 THB [11]. Even though cassava can be planted and harvested throughout the year, the major harvesting season in Thailand typically spans from October to March. This leads to the common problem of oversupply in the cassava value chain, giving the lowest cassava prices over the harvesting seasons and farmers suffering from income uncertainty. Although a government policy (e.g., income guarantee and price support) was implemented to guarantee cassava prices and boost farmers’ income, these schemes do not provide sustainable solutions to the stakeholders, especially farmers [12]. Value addition and circular practices can enhance market competitiveness and create additional revenue streams through sustainable development [3][9][3,9]. The BCG economy in Thailand allows new product developments and emerging new production on a number of alternative materials from agricultural resources. The lack of collaboration among cassava industry stakeholders, limited value addition, and constraints in accessing finance and resources can restrict the ability to capture higher prices, increase profitability, and shift to high-value-based products. The cassava value chain refers to the sequence of activities and interactions among different actors involved in the value-added process, from production, processing, distribution, and the final market of cassava and its derived products [7][13][14][15][7,13,14,15]. The cassava value chain in Thailand starts from input supply to consumption and includes various stakeholders and products, as shown in Figure 1. The core actors include input suppliers, producers or farmers, processors, traders, distributors, and end-users [7][16][7,16]. Suppliers provide inputs such as cassava stem cuttings, fertilizers, pesticides, and machinery to cassava farmers. Cassava farmers cultivate and manage cassava crops, including land preparation, planting, crop maintenance, and harvesting. Farmers face some agricultural risks, e.g., extreme temperatures and rainfalls leading to pests, plant diseases, and damage in some cassava production areas [17]. These cause low crop yields, low flour content, and high production costs. Thus, some farmers turned to new varieties that contain greater starch content and gain higher prices [7][17][7,17]. Farmers harvest the roots and distribute them to collectors or primary processors, who carry out activities such as cleaning, sorting, and packaging. After harvesting, the cassava roots must be processed immediately to prevent spoilage and preserve quality. Cassava cultivation practices can vary based on local conditions and infrastructures, climate, and farming systems. Additionally, a proper knowledge of pest and disease management, as well as good agricultural practices, is crucial to ensure successful cassava production and minimize post-harvest losses [18][19][18,19].