Rapid population growth and urbanization have led to an increase in Construction and Demolition (C&D) waste, prompting government and industry bodies to develop better waste management practices. Waste trading has emerged as a targeted intervention to divert waste from landfill sites and create a second life for waste material. This paper examines key barriers and enablers influencing the creation of a marketplace for waste trading. A systematic literature review was undertaken to examine global efforts in creating a marketplace for C&D waste. A framework on enablers and barriers for developing a marketplace for C&D waste emerged from the review, based on market-based, operational, and governance factors. References demonstrated that markets for materials such as glass and metals have already been established, but there are increasing marketplace opportunities for other recycled materials. Technology-based market applications are emerging as targeted interventions to facilitate online trading, which will provide a more accessible and user-friendly marketplace for sellers and buyers. Further research should test the complex interactions between people and technology associated with online waste trading platforms, as well as help develop the business case for a C&D waste marketplace.

- construction and demolition waste

- marketplace

- waste management

- barriers

- enablers

1. Introduction

While commerce, households, construction and other industries contribute to 7–10 billion tons of global waste generation, nearly 85% of this solid waste is deposited in landfills which are costly to run and diminishing in availability [1]. Within this context, the construction industry is responsible for generating a substantial amount of solid waste and accounts for two-fifths of the world’s energy and materials flow [1]. The Construction and Demolition (C&D) waste contribution to the global solid waste streams varies across different countries and regions: for example, Europe 25–30% in 2016 [2], United Arab Emirates (UAE) 80% in 2010 [3] and Hong Kong 23% in 2014 [4]. Between 2008 and 2009, 19.0 million tonnes (Mt) C&D waste were produced in Australia, of which 8.5 Mt were landfilled and 10.5 Mt were recovered and recycled [5]. This highlights the significant need for better waste management strategies that reuse and recycle C&D waste [6].

C&D waste generally comprises of materials such as timber, concrete, plastics, wood, metals, cardboard, asphalt, and mixed site debris such as soil and rocks [5]. Generally, most C&D waste is sent to landfill sites while the rest is recycled, reused or stockpiled [7]. With the rapid growth of the construction industry, many countries impose levies [8][9] and create jurisdictions to increase waste recovery rates [9][10]. However, evidence suggests certain limitations in levies and calls for more targeted market-based instruments to create conducive conditions for market innovation [11].

This study aims to assess global efforts for creating a marketplace for C&D waste, and to examine enablers and barriers for developing a marketplace. The authors conducted a systematic literature review of references from the last two decades [12] and build on a short conference paper presented at the 1st Asia Pacific Conference on Sustainable Development of Energy, Water, and Environmental Systems [13]. This study was motivated by the following research questions: “What are the enablers for creating a marketplace for construction and demolition waste?”, and “What are the barriers hindering C&D waste management practices?” Sections 2 and 3 outline the theoretical and research approaches. Section 4 provides the descriptive findings followed by the thematic analysis and findings in Section 5. The thematic findings of the structured literature review were categorized under key themes of: (1) What? (properties of C&D waste and targeted waste management methods), (2) Who? (waste composition and points of generation), (3) Why? (benefits of C&D waste management through waste trading) (4) How? (closing the loop through recycled waste trading, barriers for C&D waste management). Finally, the conclusions are presented in Section 6.

2. Theoretical Background

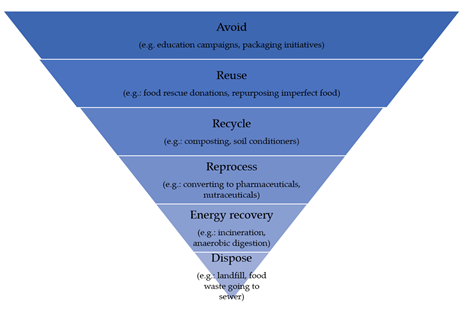

Reflecting on past urban contexts, waste management has generally been focused on eliminating hazardous substances that pose a risk to humans [14]. However, with such unsustainable management approaches, social and financial implications have become a major challenge for many communities, prompting a major shift to more sustainable and holistic management of waste [15][16]. Within C&D waste management there is more emphasis on the premise that ‘waste’ can be considered as a ‘resource’ [17] and that material can have second or a third life, enabling resources to be in the loop for a longer period of time [18]. The well-known waste hierarchy (Figure 1) describes the order of preference for options—from avoiding, to reusing, recovering, treating, and disposing of waste.

Figure 1. Waste hierarchy (adapted from [19]).

Within this hierarchical framework, the authors have turned to the key concepts of cleaner production, construction and demolition waste management, and circular economy to use as a theoretical foundation for the review [20]. With increasing attention on sustainable construction, the use of eco-material [21] and innovative technologies have emerged as targeted practices to lower production of byproduct waste. Cleaner production methodologies also describe efforts to prevent and minimise C&D waste generation [22]. While the authors acknowledge these upstream strategies, this review focuses on the residual C&D waste (waste that cannot be avoided) that arises from the industry. This residual waste can be treated and re-integrated to industrial processes through internal recycling and external recycling [23]. Many industries have also been prompted to engage in sustainable business processes with the use of the European Waste Catalogue (EWC). This has enabled the discovery of industrial symbiosis opportunities for many business entities [24].

While humans are typically engaged in linear economic practices (take-use-dispose) there is an increasing scope on circular economy [25] to longer product usage through reuse, repair, recondition, and upgrade, or a combination of those [26]. Specifically, two key strategies have been established for resource cycling. These include slowing resource loops and closing resource loops [27][28]. Slowing resource loops is defined as “product planning and design aim at a long product lifetime; this extension of product use results in the deceleration of resource flow” [29], p.309]. Closing resource loops is defined as “the periods of production and post-use stand as a closed loop, supporting circular resource flows” [29]. Creating a marketplace for reusing and recycling C&D waste will require a substantial amount of time and experience to fully develop into a reliable, skilful, marketable, and sustainable industry [30][31]. While there are difficulties identified in commercialising waste materials [32] there are many global efforts to venture into the reuse and recycling market [33] and contribute to a circular economy system. Building on this previous research, the authors carry out a systematic literature review on creating a marketplace for construction and demolition waste while appreciating the theoretical foundations elicited from circular economic principles [34].[36][37][38][39][40][41][42]

3. Descriptive Findings

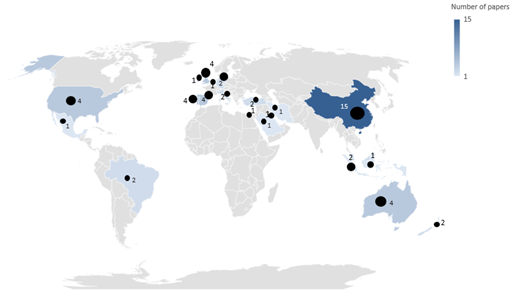

This section describes the research context, types of data, methods, types of C&D waste, and geographic distribution of the 55 academic literature sources from the Scopus, Web of Science, and ProQuest databases. Over the period of 1999–2020 there was an increase in the number of papers on C&D waste research from around one relevant paper per year in the initial years up to 26 papers over the last four complete calendar years (2016–2019). This highlights the comparatively new and emerging nature of this field of research. Figure 2 shows the geographical distribution and number of articles by the first authors. Even though some articles disclosed the exact location of the case study, some studies gave a more generic name to the case study. The first author’s country was used as the geographical location of the publication. Of the 55 papers analysed, 15 papers were recorded in China while the second-highest number of papers (n = 4) was recorded in Spain, UK, and Australia . Overall, there is a good geographical spread of case study areas and countries where the first authors are based.

Figure 2. Geographical distribution of construction and demolition (C&D) waste research.

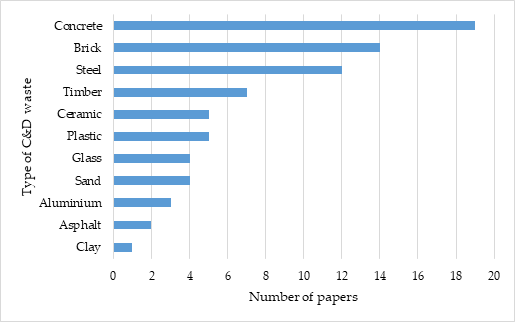

Figure 3 shows that most papers specifically discussed concrete (n = 19), brick (n = 14), steel (n =12), and timber (n = 7). These materials typically have the most demand for a second life [35].

Figure 3. Types of C&D waste.

Figure 4 shows that most papers specifically discussed concrete (n = 19), brick (n = 14), steel (n =12), and timber (n = 7). These materials typically have the most demand for a second life [35].

Figure 4. Types of C&D waste.

In terms of research approaches adopted, whilst most papers (30 publications) included analysis of secondary data in the form of literature review or content analysis of documents, a sizeable number (over 10 in each case) incorporate primary data in the form of surveys and interviews. Most of the publications (41 out of 55 publications) adopted mixed methods. The two most popular academic journals represented in the sample are Resource, Conservation, and Recycling (n = 16), and the Journal of Cleaner Production (n = 10).

4. Thematic Findings and Discussion

As the next step, the articles were coded and categorised into four key themes which are described in detail below. The thematic findings of the structured literature review were categorized under key themes: (1) Properties of C&D waste and targeted waste management methods [What]; (2) Waste composition and points of generation [Who]; (3) Benefits of C&D waste management through waste trading [Why]; and (4) Models for creating an online marketplace for connecting sellers and buyers [How]; and, (5) Enablers and barriers for creating a marketplace for C&D waste [How]. These themes are discussed in detail in the following sections.

4.1. Properties of C&D Waste and Targeted Waste Management Methods

The discourse on C&D waste management has evolved over the last two decades with a range of definitions and classifications. The nuances focus on the points of waste generation, transportation, chemical properties and management method. Table 1 provides a summary of the definitions elicited from the reviewed articles.

The authors have reconceptualized the C&D waste definition to be “A resource material after construction, renovation and demolition activities, which needs to be transported from the site and has the potential to be repurposed through downcycling or upcycling”. This shift of interpreting waste material as a resource is critical for the advancement of the waste industry.

Table 1. Definitions of C&D waste with the relevant sources.

|

Definitions |

Reference |

|

“A material, other than the material of the earth, that is transported to another place on the project site or used on the project site and does not conform to the specifications of the project because it is damaged, excess and unused/unusable or a production of the construction process that is not according to plan”. |

[36][48] P654 |

|

“Waste arising from the construction and demolition of concrete structures, masonry, roadbeds and asphalt pavements”.

|

[37][49] P3 |

|

“The waste generated by the economic activities involving the construction, maintenance, demolition and deconstruction of buildings and civil works” |

[38][50] P167 |

|

“The waste materials generated in the process of construction, remodelling, or demolition of structures (both buildings and roads). Moreover, it includes the materials produced due to natural disasters.” |

[39][51] P1363 |

|

“A material which needed to be transported elsewhere from the construction site or used on the site itself other than the intended specific purpose of the project due to damage, excess or non-use or which cannot be used due to non-compliance with the specifications, or which is a by-product of the construction process” |

[40][52] P1145 |

|

“Waste which arises from construction, renovation and demolition activities including land excavation or formation, civil and building construction, site clearance, demolition activities, roadwork, and building renovation.” |

[41][53] P224 |

|

“The surplus materials arising from any land excavation or formation, civil or building construction, roadwork, building renovation or demolition activities”

|

[42][54] P8 |

Furthermore, C&D waste has been classified as either inert or non-inert depending on whether it has stable chemical properties or not. The European Waste Catalogue classifies C&D waste into eight categories including concrete, bricks, tiles, metals, ceramics, wood, glass, and plastic. Inert materials, including soil, slurry, rocks, and broken concrete account for almost all C&D waste. Non-inert C&D waste generally comprise of metal, bamboo, paper, and timber [10].

4.2. Waste Composition and Points of Generation

C&D waste typically consists of material such as timber, concrete, asphalt, plasterboard, steel, brick, ceramic and clay, aluminium, glass, and plastic. Generally, most C&D waste is sent to landfill sites while there are limited attempts to recycle and reuse. It is critical to investigate the waste compositions and the purity of waste material to select the appropriate waste management technique.

When considering the demands for recycled material, it is evident that the market for materials such as glass and metals have already been established. Metals have the highest recycling rates among the materials recovered from C&D sites due to their value, magnetic properties, and forms. Most C&D waste generated in construction and demolition sites consists of concrete, bricks, and blocks; these are typically landfilled due to limited market demand for their recycled form. Recycled ceramics have a very limited market value at the moment, creating an opportunity for recyclers and producers to procure ceramic waste free of charge [43][55]. However, recent research shows there are increasing opportunities for concrete and bricks materials to be crushed, repurposed for recycled aggregate applications for road base and sub-base construction [44][56].

4.3. Benefits of C&D Waste Management through Waste Trading

With an increasing volume of C&D waste going into landfill sites, there are urgent calls for industrial practitioners to take immediate measures to divert waste from the landfill. The creation of markets for recycled C&D waste is thus seen as a solution that benefits both society and industry. These benefits include lower disposal costs for the waste producer and the aggregate user, together with lower environmental costs for the society. The market for trading recycled construction material is still in its infancy and creating an industrial chain requires deliberate consideration of economic parameters and market conditions [43][55]. This is due to its requirement of a high level of planning, investments, and resources [10]. Furthermore, trading C&D waste across different jurisdictions is an innovative institutional arrangement to reuse or recycle the materials, and contributes to the achievement of “cleaner production” in the construction sector [45][57].

The cost-benefit analysis is a critical economic evaluation technique to evaluate the economic feasibility of creating a marketplace for C&D waste [46][58]. Previous research provides evidence for recycling markets’ ability to rapidly grow with the increasing supply of C&D waste material indicating the opportunities to reduce the cost of recycling leveraging economies of scale. More waste also means a need for more infrastructure for waste processing. These market conditions could also be further influenced by post-disaster phases. For example, after the earthquake in Christchurch, the demand for waste concrete went from a cost negative (NZD20 per tonne disposal fee for waste concrete) to a cost positive (NZD2 per tonne payment for waste concrete) [46][58]. Therefore, the geographical spread of the damage (and waste) will also affect the feasibility of recycling.

As mentioned above, cost minimization is a critical factor that could enable the formation of markets for recycled C&D waste. However, it is important to note that the quality requirements need to be fulfilled to attract buyers who were originally purchasing natural raw material. Furthermore, it is important to make the clients more aware of the recycled C&D waste and encourage them to choose recycling aggregates. Within this context, transport and additional cost for using the material are also key considerations for buyers. Subsidies play a significant role in making recycled C&D waste more economically viable as it reduces the cost of using the recycling centre and the cost of the use of recycled aggregates. This gives more market power to the recycling centres to make a profit by charging a price to C&D waste makers and to users of aggregates additional to the cost of recycling [56].

4.4. Models for Creating an Online Marketplace for Connecting Sellers and Buyers

In the construction industry e-commerce is growing rapidly, and it adds value to waste trading related business processes along with targeted business models. E-commerce systems can be clustered into three types including (1) business to business model, (2) business-to-customer model, (3) combinatory model. Within this context, business-to-business models have gained popularity in the construction industry considering its viable and competitive nature. Its ability to create e-commerce systems have enabled large numbers of architects, designers, and contractors to conduct more business over the Internet. The marketplace, for example, is a business platform for integrative business courses, offering decision-making material that covers marketing, product development, sales force management, financial analysis, accounting, manufacturing, and quality control [47][59].

This section specifically considers global and local examples of online marketplaces created for trading C&D waste. Relevant examples of business-to-business models, business-to-customer models, and combinatory models were obtained. Each example was assessed on its key features, type of e-commerce model, and its implications on closing the loop. The coalescence of advancements of digital technologies in marketing and business presents a unique opportunity to achieve an accessible interface to connect seller and buyers.

Through a review of these local and global precedents, several criteria were developed to compare the examples and examine the platform, material, and cost related to these online marketplaces for sellers and buyers. Table 3 provides a matrix showing the availability of these features in the local and global examples. Table 3 presents a suite of ten features related to material types, nature of the platform, and associated costs related to the selected examples of online waste trading platform.

According to the above matrix, most of the platforms offered a wide range of C&D material and mixed products to sell and buy through combinatory platforms. Of the total 13 reviewed platforms, 7 have easily accessible platforms where navigation was intuitive and user-friendly for sellers and buyers. Of the total 13 online marketplaces, 7 platforms offer free searching options and 6 platforms offer free registration and advertising for sellers enabling more contractors and recyclers to sell C&D material without an advertising fee. According to the above review, it was evident that there were 7 combinatory models available in the market under comparison and 6 business-to-business models leveraging the easier accessibility, connections and collaborative network of businesses, organizations, entrepreneurs and buyers. Many of these businesses acknowledged that in addition to diverting waste from landfills, these recovery activities generate significant cost savings, energy savings, and create new jobs and business opportunities. In addition to these marketplace functions, there is a need for holistic models with multi-user platforms encompassing technical standards, environmental laws, tools to assess environmental impacts and circularity, and interactive maps with geolocations. Such a platform, named DECORUM, has been developed in Italy with the aim of improving resource efficiency in the construction sector as a whole [48][73].

Furthermore, clear benefits for local community and government authorities were highlighted. These include improved education and awareness of waste/by-product resources, contribution to social enterprise activities across the state/nation, possible amalgamation of resources and new business opportunities, and provision of value-add services to the business community. These online business networks facilitate economic development practices through their tailored solutions to end-users. Facilitating the reuse of materials and cross-sectoral synergies is central to success in scaling up the transition to a circular economy. Existing marketplaces contribute to decreasing the demand for virgin materials and energy, highlighting the critical need for mainstreaming these practices.

4.5. Closing the Loop through Waste Recycling: Enablers and Barriers for Creating a Marketplace for C&D Waste

Circular economy incorporates a variety of strategies to take control of the end-of-life scenario, with specific focus on being regenerative and restorative by design [49][74]. There is an emerging consensus on considering ‘buildings as material banks’, and actively managing accounts of the materials deposited within them through material passports, building information modelling (BIM), and Internet of Things (IoT) devices [50][75]. While BIM has the ability to create designs using data related to geometry, relations, and attributes, BIM-aided construction demonstrates the ability to reduce waste across design activities and contributes to designers and architects in their decision-making [[51]76],[52][77]. IoT standards enable smooth information flow throughout the construction project and beyond, through evaluating proof of concept and associated frameworks [53][78].

Circular economy models are yet to have mainstream application and require more innovative procurement models through Public Private Partnership [10], closed loop supply chains [47], and closed cycle construction principles [54][79]. When reflecting on global practices, the UK has demonstrated best practices around guiding construction actors/stakeholders across materials’ life cycles to reduce waste generation and carbon emissions. These initiatives includes improving resource efficiency in construction, minimize waste and to maximize reuse and develop products from waste material (i.e.: downcycling and upcycling), . This approach has successfully diverted five million tonnes of waste annually from going into landfills [52]. The above-mentioned practices improve the capacity for innovation throughout the chain of production, consumption, distribution and recovery of materials and energy, enabling practitioners to achieve a cradle-to-cradle vision [55][80].

Creating a marketplace for C&D waste trading would create a second life for waste material and connect producers and buyers who would benefit from lowering their disposal and purchasing costs. In order to create a viable marketplace, there are several factors to be noted which influence the supply chain, including material procurement, recycling process, plant management and market promotions. It is critical to have government intervention through market-based policy instruments to encourage uptake of the circular economy by boosting C&D waste recovery and management [56][81]. It is also important to establish institutions to prevent corruption and opportunistic behaviours that could take place during negotiating, contracting, and operating [10]. “Walking the talk” is a key highlight of inducing positive behaviour in the market and [57][82] claims that when the government provides adequate information about the quality and benefits of C&D recycled materials and uses these in its own projects, more efforts will be made to take up this practice.

An appropriate market is required to connect sellers and buyers through easily accessible user-friendly platforms. Online platforms have been identified as a potential marketplace due to their versatility and accessibility. With the increasing growth of e-commerce there is more opportunity for digital techniques to add value to waste trading related business processes. E-commerce systems can be clustered into three types of models: (1) business to business model; (2) business-to-customer model; and (3) combinatory model [59]. Attempts have been made to map the process flow of waste exchange processes with options for sellers and buyers to connect through a digital interface [58][83]. Within this context Table 2 provides a summary of enablers under the three key themes of governance, operations, and market enablers. Enablers were elicited from key literature on measures for implementing supportive legislation and policies, identifying critical success factors such as on-site sorting, factors affecting the management of supply chains, requirements for material recycling, and strategies for engaging key stakeholders.

Table 2. A summary of key enablers for effective C&D waste management and market creation elicited from the literature.

|

Types of enablers |

Sub-Enablers |

|

Governance enablers |

(1) Increased targeting of design stages in policies and extension of sustainable design appraisal systems, (2) increased stringency of legislative measures, fiscal policies, (3) corroboration of policy requirements with enablers and facilitators [82], (4) taxing virgin aggregates, recyclable materials that are landfilled [11], (5) subsidizing C&D waste recycling businesses[59][60]. [55,84,85]. |

|

Operational enablers |

(1) Reliable recycling technology, and infrastructure [86], [61], (2) continuous supply of contamination-free material, [62], (3) organized transportation [63], (4) responsible workforce, (5) effective communication and stakeholder engagement.(2) continuous supply of contamination-free material, [87], (3) organized transportation [88], (4) responsible workforce, (5) effective communication and stakeholder engagement [11]. |

|

Market enablers |

(1) Increasing client awareness of the short- and long-term benefits of reusing, (2) presence of a market for different types of products from demolition, (3) standardization for the quality of recycled material, (3) supportive insurance, legal advice and accounting services, (4) commercial/marketing expenses, (5) creation of ongoing demand for recycled material [64][55,89] |

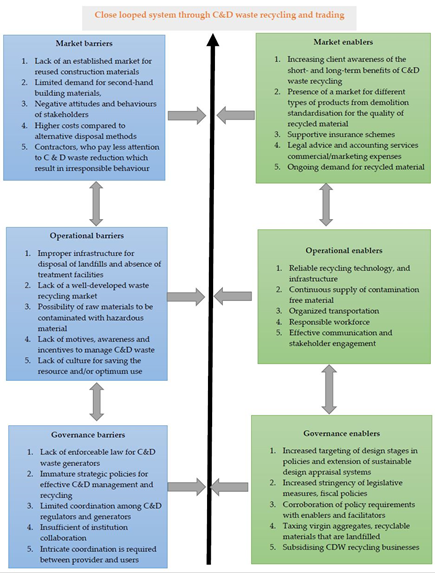

Governance enablers comprise all processes including laws, norms, and rules to facilitate C&D waste trading. Five key governance sub-enablers comprise of: (1) increased targeting of design stages in policies and extension of sustainable design appraisal systems, (2) increased stringency of legislative measures, fiscal policies, (3) corroboration of policy requirements with enablers and facilitators [82], (4) taxing virgin aggregates, recyclable materials that are landfilled [11], (5) subsidising C&D waste recycling businesses [55,84,85].

Operational enablers comprise of all technical processes and necessary human resources to manage material supply chains, sorting facilities, waste segregation, and recycling operations. Five operational sub-enablers consist of: (1) reliable recycling technology, and infrastructure [86], (2) continuous supply of contamination-free material, [87], (3) organized transportation [88], (4) responsible workforce, (5) effective communication and stakeholder engagement [11]. Market enablers comprise creating conducive market conditions to sustain the demand for C&D waste and supply of material.

Five market sub-enablers are: (1) increasing client awareness of the short- and long-term benefits of reusing, (2) presence of a market for different types of products from demolition, (3) standardisation for the quality of recycled material, (3) supportive insurance, legal advice and accounting services, (4) commercial/marketing expenses, (5) creation of ongoing demand for recycled material [55,89].

This section analyses barriers and challenges for C&D waste management, particularly focussing on C&D waste recycling and creating a marketplace for secondary material. Barriers related to availability, economics, and acceptability were considered as three overarching categories [50]. These categories were then divided into three themes—governance, operational, and market—to align with the enablers described above. Table 3 provides a summary of the key barriers affecting the uptake of C&D waste management practices.

Table 3. A summary of key barriers affecting the uptake of C&D waste management practices.

|

Types of Barriers |

Sub-Barriers |

|

Governance barriers |

(1) Lacking enforceable law for C&D waste generators, (2) immature strategic policies for effective C&D management and recycling [65][66], (3) limited coordination among C&D regulators and generators, (4) lack of institution collaboration, (5) intricate coordination is required between provider and users [65].[53,90,91], (3) limited coordination among C&D regulators and generators, (4) lack of institution collaboration, (5) intricate coordination is required between provider and users [90]. |

|

Operational barriers |

(1) Improper infrastructure for disposal of landfills and absence of treatment facilities, (2) lack of a well-developed waste recycling market, (3) possibility of raw materials being contaminated with hazardous material such as heavy metals and other pollutants, including asbestos, originating in building products [53,92], (4) [67], (4) lack of motives, awareness, and incentives to manage C&D waste, (5) lack of culture for saving the resource and/or optimum use [65].lack of motives, awareness, and incentives to manage C&D waste, (5) lack of culture for saving the resource and/or optimum use [53,90]. |

|

Market barriers |

(1) Lack of an established market for reused construction materials, (2) limited demand for second-hand building materials, (3) negative attitudes and behaviors of stakeholders [11], (4) higher costs compared to alternative disposal methods [92], (5) contractors who [67], (5) contractors who pay less attention to C&D waste reduction which results in irresponsible behavior.pay less attention to C&D waste reduction which results in irresponsible behavior [11]. |

If the waste producers and buyers are to engage in effective C&D waste management practice, it is critical that they understand what enables such practice and possible barriers that might arise. The authors present the three key barrier types supported by 15 sub-barriers and three key enabler types. This is supported by 15 sub-enablers for developing a marketplace for C&D waste. Industrial practitioners could use these aspects as a guide to engagement in C&D waste trading practices within the construction industry and contribute to the circular economy. Governance barriers comprise of all limitations in structures, policies, and legislation that hinder C&D waste trading efforts. Five key governance sub-barriers comprise of: (1) lacking enforceable law for C&D waste generators, (2) immature strategic policies for effective C&D management and recycling [53,90,91], (3) limited coordination among C&D regulators and generators, (4) lack of institutional collaboration, (5) intricate coordination required between provider and users [90]. Previous research has highlighted that some incentives for C&D waste recycling plants provided by government are insufficient to sustain the economic viability of these recycling plants especially because the costs of recycled products are particularly high compared to those made from virgin material [68][93]. Operational barriers comprise of all limitations, technical processes, and human resources that obstruct the management of material supply chains, sorting facilities, waste segregation, and recycling operations.

Five operational sub-barriers consist of: (1) improper infrastructure for disposal of landfills and absence of treatment facilities, (2) lack of a well-developed waste recycling market, (3) possibility of raw materials being contaminated with hazardous materials such as heavy metals and other pollutants, including asbestos, originating in building products [53,92], (4) lack of motives, awareness and incentives to manage C&D waste, (5) lack of culture for saving the resource and/or optimum use [53,90]. Hazardous waste pollutants such as asbestos can be released during the demolition or renovation of existing structures [52]. Removing this type of pollutant is critical as the contaminated material will be rejected for re-use or recycling during inspection [55]. This also means there are additional costs for contractors and waste handlers in terms of testing for asbestos [69][94]. Especially when the separation is done off-site, there is an additional risk of asbestos being mixed with general debris. Particularly, when natural disasters such as earthquakes occur, it can lead to collapsed building material being mixed with contaminated matter. For example, collapsed buildings in Christchurch were contaminated with asbestos and the building material could not be recycled [92]. Therefore, careful measures should be taken to identify, test, and remove hazardous material from C&D waste.

Market barriers comprise market, environmental, and financial conditions impeding the supply and demand of C&D waste material. Five market sub-barriers are: (1) lack of an established market for reused construction materials, (2) limited demand for second-hand building materials, (3) negative attitudes and behaviours of stakeholders [11], (4) higher costs compared to alternative disposal methods, (5) contractors who pay less attention to C&D waste reduction which results in irresponsible behaviour [11].

4.6. Emergent Framework on Enabling a Marketplace for C&D Waste

Based on these findings the authors present an emergent, novel framework of enablers and barriers that can guide practitioners and government policymakers in creating waste trading platforms. Figure 4 presents these six key categories of enablers and barriers along with sub-categories derived from Tables 4 and 5. Through this analysis it was evident that market-based policy instruments could be developed through taxes, subsidies and other incentives, to encourage waste diversion from landfills, and recycle and create another life for waste material. To market the recycled material as a substitute for natural raw materials, it is important to increase awareness and carry out promotional activities. A continuous supply of clean waste streams is necessary to produce high-quality recycled materials that satisfy the given technical specifications and can be economically competitive. Finally, an appropriate market is required to connect sellers and buyers through easily accessible user-friendly platforms. Online platforms have been identified as a potential marketplace due to their versatility and accessibility.

Figure 4. Emergent framework on enablers and barriers for developing a marketplace for C&D waste.

References

- Turkyilmaz, A.; Guney, M.; Karaca, F.; Bagdatkyzy, Z.; Sandybayeva, A.; Sirenova, G. A Comprehensive Construction and Demolition Waste Management Model using PESTEL and 3R for Construction Companies Operating in Central Asia. Sustainability 2019, 11, 1593.

- European Commission. Construction and Demolition Waste (CDW). Availabe online: https://ec.europa.eu/environment/waste/construction_demolition.htm (accessed on 20 June 2020).

- Rogers, S. Battling construction waste and winning: Lessons from UAE. In Proceedings of the Institution of Civil Engineers-Civil Engineering;London, UK: 2011; pp. 41–48.

- Unit, E.S. Monitoring of Solid Waste in Hong Kong—Waste Statistics for 2014; Environmental Protection Department: Hong Kong, China, 2015.

- McCabe, B.; Clarke, W. Explainer: How much landfill does Australia have. Conversat. Aust. 2017. Availabe online: https://theconversation.com/explainer-how-much-landfill-does-australia-have-78404#:~:text=Surprisingly%2C%20we%20don't%20know,ones%2C%20most%20of%20them%20small. (accessed on 25 May 2020)

- Chen, J.; Hua, C.; Liu, C. Considerations for better construction and demolition waste management: Identifying the decision behaviors of contractors and government departments through a game theory decision-making model. J. Clean. Prod. 2019, 212, 190–199.

- Rao, A.; Jha, K.N.; Misra, S. Use of aggregates from recycled construction and demolition waste in concrete. Resour. Conserv. Recycl. 2007, 50, 71–81.

- Nikmehr, B.; Hosseini, M.R.; Rameezdeen, R.; Chileshe, N.; Ghoddousi, P.; Arashpour, M. An integrated model for factors affecting construction and demolition waste management in Iran. Eng. Constr. Arch. Manag. 2017, 24, 1246–1268, doi:10.1108/ECAM-01-2016-0015.

- Shooshtarian, S.; Maqsood, T.; Khalfan, M.; Yang, R.J.; Wong, P. Landfill Levy Imposition on Construction and Demolition Waste: Australian Stakeholders’ Perceptions. Sustainability 2020, 12, 4496.

- Bao, Z.; Lu, W.; Chi, B.; Yuan, H.; Hao, J. Procurement innovation for a circular economy of construction and demolition waste: Lessons learnt from Suzhou, China. Waste Manag. 2019, 99, 12–21.

- Park, J.; Tucker, R. Overcoming barriers to the reuse of construction waste material in Australia: A review of the literature. Int. J. Constr. Manag. 2017, 17, 228–237.

- Denyer, D.; Tranfield, D. Producing a systematic review. In The Sage Handbook of Organizational Research Methods; Bryman, D.A.B.A., Ed.; Sage Publications Ltd: Thousand Oaks, CA, USA, 2009; pp. 671–689.

- Caldera, S.; Ryley, T.; Zatyko, N. Developing a marketplace for construction and demolition waste based on a systematic quantitative literature review. In Proceedings of the 1 st Asia Pacific Sustainable Development of Energy Water and Environment Systems, Gold Coast, Australia: 6–9 April 2020.

- Wilson, D.C.; Rodic, L.; Modak, P.; Soos, R.; Carpintero, A.; Velis, K.; Iyer, M.; Simonett, O. Global Waste Management Outlook; UNEP: London, UK: 2015.

- Papargyropoulou, E.; Lozano, R.; Steinberger, J.K.; Wright, N.; bin Ujang, Z. The food waste hierarchy as a framework for the management of food surplus and food waste. J. Clean. Prod. 2014, 76, 106–115.

- Caldera, H.T.S.; Desha, C.; Dawes, L. Transforming manufacturing to be ‘good for planet and people’, through enabling lean and green thinking in small and medium-sized enterprises. Sustain. Earth 2019, 2, 4, doi:10.1186/s42055-019-0011-z.

- Bringezu, S.; Bleischwitz, R. Sustainable Resource Management: Global Trends, Visions and Policies; Routledge: New York, NY, USA, 2017.

- Galvín, A.P.; Ayuso, J.; García, I.; Jiménez, J.R.; Gutiérrez, F. The effect of compaction on the leaching and pollutant emission time of recycled aggregates from construction and demolition waste. J. Clean. Prod. 2014, 83, 294–304.

- Australia Government. National Food Waste Strategy: Halving Australia’s food waste by 2030, Commonwealth of Australia 2017. Availabe online: https://www.environment.gov.au/system/files/resources/4683826b-5d9f-4e65-9344-a900060915b1/files/national-food-waste-strategy.pdf (accessed on 13 November).

- Mahpour, A. Prioritizing barriers to adopt circular economy in construction and demolition waste management. Resour. Conserv. Recycl 2018, 134, 216–227.

- Garg, C.; Jain, A. Green concrete: Efficient & eco-friendly construction materials. Int. J. Res. Eng. Technol. 2014, 2, 259–264.

- Wang, N.; Ma, M.; Wu, G.; Liu, Y.; Gong, Z.; Chen, X. Conflicts concerning construction projects under the challenge of cleaner production–case study on government funded projects. J. Clean. Prod. 2019, 225, 664–674.

- Pimenta, H.D.; Gouvinhas, R.; Evans, S. Cleaner Production as a Corporate Sustainable Tool: A Study of Companies from Rio Grande do Norte State, Brazil. In Sustainable Manufacturing; Springer: Berlin, Heidelberg, Germany: 2012; pp. 23–31.

- van Capelleveen, G.; Amrit, C.; Zijm, H.; Yazan, D.M.; Abdi, A. Toward building recommender systems for the circular economy: Exploring the perils of the European Waste Catalogue. J. Environ. Manag 2020, 277, 111430.

- Leising, E.; Quist, J.; Bocken, N. Circular Economy in the building sector: Three cases and a collaboration tool. J. Clean. Prod. 2018, 176, 976–989.

- Esposito, M.; Tse, T.; Soufani, K. Is the circular economy a new fast‐expanding market? Thunderbird Int. Bus. Rev. 2017, 59, 9–14.

- Geissdoerfer, M.; Morioka, S.N.; de Carvalho, M.M.; Evans, S. Business models and supply chains for the circular economy. J. Clean. Prod. 2018, 190, 712–721.

- McDonough, W.; Braungart, M. 3 Remaking the way we make things: Creating a new definition of quality with cradle-to-cradle design. In The International Handbook on Environmental Technology Management; Edward Elgar: Cheltenham, Northampton, UK: 2008; p. 33.

- Bocken, N.M.; de Pauw, I.; Bakker, C.; van der Grinten, B. Product design and business model strategies for a circular economy. J. Ind. Prod. Eng 2016, 33, 308–320.

- Silva, R.; De Brito, J.; Dhir, R. Availability and processing of recycled aggregates within the construction and demolition supply chain: A review. J. Clean. Prod. 2017, 143, 598–614.

- Shooshtarian, S., Caldera, S., Maqsood,T., Ryley, T. Using Recycled Construction and Demolition Waste Products: A Review of Stakeholders’ Perceptions, Decisions, and Motivations Recycling 2020, 5, doi:https://doi.org/10.3390/recycling5040031.

- Galan, B.; Dosal, E.; Andrés, A.; Viguri, J. Optimisation of the construction and demolition waste management facilities location in Cantabria (Spain) under economical and environmental criteria. Waste Biomass Valorization 2013, 4, 797–808.

- Rodríguez-Robles, D.; García-González, J.; Juan-Valdés, A.; Morán-del Pozo, J.M.; Guerra-Romero, M.I. Overview regarding construction and demolition waste in Spain. Environ. Technol. 2015, 36, 3060–3070.

- Shooshtarian, S.; Maqsood, T.; Wong, P.S.; Khalfan, M. Market development for a construction and demolition waste stream in Australia. J. Constr. Eng. 2020, 3, 220–231.

- Gálvez-Martos, J.-L.; Styles, D.; Schoenberger, H.; Zeschmar-Lahl, B. Construction and demolition waste best management practice in Europe. Resour. Conserv. Recycl 2018, 136, 166–178.

- Chen, Z.; Li, H.; Kong, S.C.W.; Hong, J.; Xu, Q. E-commerce system simulation for construction and demolition waste exchange. Autom. Constr. 2006, 15, 706–718.

- Coelho, A.; de Brito, J. Economic analysis of conventional versus selective demolition—A case study. Resour. Conserv. Recycl 2011, 55, 382–392.

- Wibowo, M.A.; Handayani, N.U.; Mustikasari, A. Factors for implementing green supply chain management in the construction industry. J. Ind. Eng. Manag 2018, 11, 651–679.

- Di Maria, A.; Eyckmans, J.; Van Acker, K. Downcycling versus recycling of construction and demolition waste: Combining LCA and LCC to support sustainable policy making. Waste Manag. 2018, 75, 3–21.

- Umar, U.A.; Shafiq, N.; Malakahmad, A.; Nuruddin, M.F.; Khamidi, M.F. A review on adoption of novel techniques in construction waste management and policy. J. Mater. Cycles Waste Manag. 2017, 19, 1361–1373.

- Esa, M.R.; Halog, A.; Rigamonti, L. Developing strategies for managing construction and demolition wastes in Malaysia based on the concept of circular economy. J. Mater. Cycles Waste Manag. 2017, 19, 1144–1154.

- Yuan, H.; Shen, L.; Wang, J. Major obstacles to improving the performance of waste management in China's construction industry. Facilities 2011, 29, doi:10.1108/02632771111120538.

- Fukao, T.; Bailey-Serres, J. Plant responses to hypoxia—Is survival a balancing act? Trends Plant Sci. 2004, 9, 449–456, doi:10.1016/j.tplants.2004.07.005.

- Loreti, E.; Valeri, M.C.; Novi, G.; Perata, P. Gene regulation and survival under hypoxia requires starch availability and Metabolism. Plant Physiol. 2018, 176, 1286–1298, doi:10.1104/pp.17.01002.

- Akman, M.; Bhikharie, A.V.; McLean, E.H.; Boonman, A.; Visser, E.J.W.; Schranz, M.E.; Van Tienderen, P.H. Wait or escape? Contrasting submergence tolerance strategies of Rorippa amphibia, Rorippa sylvestris and their hybrid. Ann. Bot. 2012, 109, 1263–1275, doi:10.1093/aob/mcs059.

- Wu, G.; Park, M.Y.; Conway, S.R.; Wang, J.W.; Weigel, D.; Poethig, R.S. The Sequential Action of miR156 and miR172 Regulates Developmental Timing in Arabidopsis. Cell 2009, 138, 750–759, doi:10.1016/j.cell.2009.06.031.

- Wu, G.; Poethig, R.S. Temporal regulation of shoot development in Arabidopsis thaliana by miRr156 and its target SPL3. Development 2006, 133, 3539–3547, doi:10.1242/dev.02521.

- Benov, L.; Fridovich, I. A superoxide dismutase mimic protects sodA sodB Escherichia coli against aerobic heating and stationary-phase death. Arch. Biochem. Biophys. 1995, 322, 291–294.

- Hsu, S.Y.; Wang, J.Y.; Liao, H.E. Factors which influence the willingness of injection drug users to participate in the harm reduction program. Taiwan J. Public Health 2007, 26, 292–302.

- Jagadeeswaran, G.; Saini, A.; Sunkar, R. Biotic and abiotic stress down-regulate miR398 expression in Arabidopsis. Planta 2009, 229, 1009–1014, doi:10.1007/s00425-009-0889-3.

- Li, T.; Li, H.; Zhang, Y.X.; Liu, J.Y. Identification and analysis of seven H2O2-responsive miRNAs and 32 new miRNAs in the seedlings of rice (Oryza sativa L. ssp. indica). Nucleic Acids Res. 2011, 39, 2821–2833, doi:10.1093/nar/gkq1047.

- Fahlgren, N.; Howell, M.D.; Kasschau, K.D.; Chapman, E.J.; Sullivan, C.M.; Cumbie, J.S.; Givan, S.A.; Law, T.F.; Grant, S.R.; Dangl, J.L.; et al. High-throughput sequencing of Arabidopsis microRNAs: Evidence for frequent birth and death of MIRNA genes. PLoS ONE 2007, 2, doi:10.1371/journal.pone.0000219.

- Liu, Q.; Zhang, Y.C.; Wang, C.Y.; Luo, Y.C.; Huang, Q.J.; Chen, S.Y.; Zhou, H.; Qu, L.H.; Chen, Y.Q. Expression analysis of phytohormone-regulated microRNAs in rice, implying their regulation roles in plant hormone signaling. FEBS Lett. 2009, 583, 723–728, doi:10.1016/j.febslet.2009.01.020.

- Lu, C.; Jeong, D.H.; Kulkarni, K.; Pillay, M.; Nobuta, K.; German, R.; Thatcher, S.R.; Maher, C.; Zhang, L.; Ware, D.; et al. Genome-wide analysis for discovery of rice microRNAs reveals natural antisense microRNAs (nat-miRNAs). Proc. Natl. Acad. Sci. USA 2008, 105, 4951–4956, doi:10.1073/pnas.0708743105.

- Small, I.D.; Peeters, N. The PPR motif—A TPR-related motif prevalent in plant organellar proteins. Trends Biochem. Sci. 2000, 25, 45–47, doi:10.1016/s0968-0004(99)01520-0.

- Felippes, F.F.; Weigel, D. Triggering the formation of tasiRNAs in Arabidopsis thaliana: The role of microRNA miR173. EMBO Rep. 2009, 10, 264–270, doi:10.1038/embor.2008.247.

- Allen, E.; Xie, Z.; Gustafson, A.M.; Carrington, J.C. microRNA-directed phasing during trans-acting siRNA biogenesis in plants. Cell 2005, 121, 207–221, doi:10.1016/j.cell.2005.04.004.

- Mallory, A.; Vaucheret, H. Form, function, and regulation of ARGONAUTE proteins. Plant Cell 2010, 22, 3879–3889, doi:10.1105/tpc.110.080671.

- Li, W.; Cui, X.; Meng, Z.; Huang, X.; Xie, Q.; Wu, H.; Jin, H.; Zhang, D.; Liang, W. Transcriptional regulation of arabidopsis MIR168a and ARGONAUTE1 homeostasis in abscisic acid and abiotic stress responses. Plant Physiol. 2012, 158, 1279–1292, doi:10.1104/pp.111.188789.

- Singh, R.K.; Gase, K.; Baldwin, I.T.; Pandey, S.P. Molecular evolution and diversification of the Argonaute family of proteins in plants. BMC Plant Biol. 2015, 15, 23, doi:10.1186/s12870-014-0364-6.

- Liu, Q.; Yao, X.; Pi, L.; Wang, H.; Cui, X.; Huang, H. The ARGONAUTE10 gene modulates shoot apical meristem maintenance and establishment of leaf polarity by repressing miR165/166 in Arabidopsis. Plant J. 2009, 58, 27–40, doi:10.1111/j.1365-313X.2008.03757.x.

- Harvey, J.J.W.; Lewsey, M.G.; Patel, K.; Westwood, J.; Heimstädt, S.; Carr, J.P.; Baulcombe, D.C. An antiviral defense role of AGO2 in plants. PLoS ONE 2011, 6, e14639, doi:10.1371/journal.pone.0014639.

- Hu, P.; Zhao, H.; Zhu, P.; Xiao, Y.; Miao, W.; Wang, Y.; Jin, H. Dual regulation of Arabidopsis AGO2 by arginine methylation. Nat. Commun. 2019, 10, 1–10, doi:10.1038/s41467-019-08787-w.

- Montgomery, T.A.; Howell, M.D.; Cuperus, J.T.; Li, D.; Hansen, J.E.; Alexander, A.L.; Chapman, E.J.; Fahlgren, N.; Allen, E.; Carrington, J.C. Specificity of ARGONAUTE7-miR390 Interaction and Dual Functionality in TAS3 Trans-Acting siRNA Formation. Cell 2008, 133, 128–141, doi:10.1016/j.cell.2008.02.033.

- Fahlgren, N.; Montgomery, T.A.; Howell, M.D.; Allen, E.; Dvorak, S.K.; Alexander, A.L.; Carrington, J.C. Regulation of AUXIN RESPONSE FACTOR3 by TAS3 ta-siRNA Affects Developmental Timing and Patterning in Arabidopsis. Curr. Biol. 2006, 16, 939–944, doi:10.1016/j.cub.2006.03.065.